Incumbert Operators – Unexpectant First Moves?

"If you can't beat them, join them." Anon

With the launch of their own VoIP services, this seems to be the tactic incumbent operators have adopted. AT&T's 'CallVantage' and Verizon's 'VoiceWing' proprietary offerings provide incumbents with exposure to VoIP. BT similarly launched its 'Total Broadband' product in early 2006, which provides free off-peak calls through its 'Broadband Talk' VoIP service.

Incumbent operators are aiming to offset declines in traditional voice revenues, retain customers and significantly reduce costs. Furthermore, by switching to VoIP, they are able to offer the value-added services that an IP platform makes possible, as well as charge for them.

Alternative telecom operators have also looked to seize the opportunity, launching their own internet telephony services. THUS, for example, offers international and domestic Voice over Broadband (VoBB) calls through its Demon brand name, while Cable and Wireless was among the first companies to offer off-the-shelf IP telephony to UK businesses.

Internet Protocol Television (IPTV) is the service that telecom operators are most excited about, as it will allow them to charge for a "triple" or "quad-play" package of services.2 BT unveiled its 'BT Vision' IPTV platform in December 2006, with the move adding digital TV and on-demand pay-per-view content to the company's core broadband, internet and fixed/mobile voice offerings. The company reported to have signed up 150,000 subscribers by February 2008.

Indeed, 2007 saw a wave ofM&A activity as telcos and other market participants looked for traction in the sector. US IPTV software developer Tandberg Television was snapped up by Ericsson inMarch for a total consideration of £642 million, with President and CEOCarl-Henric Svanberg describing IPTV as "the biggest networked multimedia opportunity [for cable and telecom operators] going forward."3 Closer to home, Alcatel Lucent reinforced its IPTV capabilities with the acquisition of London based Tamblin Ltd in September 2007, while the 2006 merger of Tiscali UK and VideoNetworks Ltd, gave the broadband provider access to the "Home Choice" IPTV and Video On Demand (VOD) platform and content.4

Consolidation is expected to continue a pace, as telcos look to continue to round out their IPTV offerings. In 2008, the focusmay well be onmiddleware, VOD and encoding companies. AIM-listed Orca Interactive, for example, issued a statement confirming that it was the subject of a takeover bid in January 2007. London-based contentmanagerOn DemandGroup and filmspecialist Film Flex could conceivably be spun off from larger parent groups.

Both incumbent telcos and new entrants now offer managed and proprietaryQuality of Service (QoS) VoIP services. By developing their own IP infrastructure, whereQoS is high, participants have begun the transition towardsNext GenerationNetworks (NGNs).

NGN's aimis to provide triple and quad-play services that are integrated at the network and not just at the billing level. Roll-out strategies have differed fromone company to the next,with some players retaining 100%control.Others have outsourced all or part of thework, creating opportunities for companies providingNGNmigration solutions such as Yorkshire-based Teleware plc, aswell as third-party vendors. Thismodel is likely to define the future landscape, asNGNs minimiseQoS issues and facilitate a move away from pay-per-use contracts to flatfee schemes. Deployment will, however, require significant investments, which not all players will be immediately ready or able to make.

Figure 9: Next Generation Network

Forward looking fixed line operators have understood that it is not a question of 'if' but 'when' VoIP will supplant PlainOld Telephone services (POTs). This is why many operators are developing NGNIP networks that will allow them to gain greater efficiency.

Broadband Access Providers – Who Will Survive The Battlefield?

In the UK, the broadbandmarket has become increasingly crowded and competitive. The sector, dominated by BT, VirginMedia (formerlyNTL), AOL, Tiscali andOrange (formerlyWanadoo), has seen the entrance of numerous and diverse players offering VoIP services.

Over 300 ISPs, from virtual ISP resellers to Tier 1 backbone carriers, resell BT wholesale's core DSL in the UK.With their 'best effort' networks, these players face major challenges as systems evolve towards IP-centricNGN architectures, offering superior QoS and the capacity to support multiple voice, data and video services.

Resellers, especially small players, face the prospect of a particularly 'bitter end'. They are likely either to be pushed out of the industry or taken over by larger ISPs which use Local Loop Unbundling (LLU). Companies such as Tiscali orOrange are taking advantage of regulatory changes which compel the incumbent telecom operators (BT and Kingston in the UK) to make their local networks available to competitors.

Acquisition is particularly likely for companies with a valuable or complementary subscriber base. Brightview Group plc, for example, which operates under the ISP brand name "Madasafish", was acquired by BT plc in July 2007 for approximately £15 million.5 Potential targets in 2008 may include some of the many independent residential and enterprise ISPs such as Edinburgh based Lumison andNDO (Namesco), an ISP and hosting company.Other resellers which may be attractive to acquisitive broadband access providers include Prodigy Networks, Fast.co.uk (part of the Dark Group), Firefly Internet and Breathe Networks.

Even large players are suffering from the intense competition. After months of speculation, CarphoneWarehouse, which entered the UK broadband market with its much hyped "free" broadband offering "TalkTalk", announced the purchase of AOL UK,6 which enjoyed one of the largest shares in the UK broadband market.

Numerous big-name firms are lining up to offer VoIP as part of their broadband packages.Orange, with its Livebox product, is understood to have gained approximately 3.6 million VoIP customers across Europe since the launch of its offering inNovember 2005, making it the market leader ahead of Neuf Cegetel and Free. In the UK, BT Broadband announced that it had passed the symbolic bar of 1 million VoIP subscribers in January 2007. VoIP therefore represent approximately 5%of the company's residential voice call business, as the number of customer lines stood at 19 million inMarch 2007. Other players entering the arena include satellite broadcaster BSkyB, which started to offer broadband connections following the acquisition of the ISP Easynet7, and Tesco which launched its own VoIP services in early 2006.

Cable operators – once challengers, today's challenged?

Embracing VoIP enables cable operators such as VirginMedia, as well as potentially regional players likeWhite Cable (Isle ofWhite) and SmallWorld (Scotland), to offer telephony in addition to their TV, entertainment and broadband services. Since they do not depend on voice revenues, they leverage cheap VoIP services as a competitive advantage, allowing them to increase Annual Revenue per User (ARPU). Voice has become a product 'sold for free', which is subsidised by other elements of the triple-play offer and used to retain customers.

Cable operators are not, however, immune to the fierce battle taking place in the market and have begun to take positions.NTL despite having its own cable network and a strong position merged with Telewest in 2006. The combined company, which has since been acquired and rebranded by Virgin Media, was the first to offer quad-play in the UK, launching a package which bundles together television and highspeed internet, as well as fixed and mobile voice services. The giant communications group is in the midst of a joint programme with Ericsson to upgrade its circuit-switched technology. The scheme will allow VirginMedia to develop its VoIP capabilities and underlines its intention to challenge BSkyB and BT.

In addition to improving infrastructure, cable operators and others players looking to roll out quadplay product offerings are increasingly looking to third-parties to assist with the seamless delivery of digital services across different mediums. Cambridgebased ANT Software is one such company. The integrator's Galio Suite software platform, for example, allows users to route and receive IP calls through their TV, as well as to pause and restart transmission at the end of their conversation. It also supports internetbased social networking applications

Telcos are likely to continue to face a major challenge from cable operators, particularly in urbanised areas where the rate of penetration is high. In the UK, VirginMedia has a large reach which encompasses approximately 50%of households and 85%of businesses.Offnet weaknesses can, in any case, be surmounted by leasing other operators' networks to reach new geographical areas and potential subscribers.

Mobile operators – facing a threat or an opportunity?

Mobile operators face an even greater challenge than fixed line or cable operators. Currently, growth is slowing and competition on price is continuing to drive down margins.

As for the future, it is not clear from where new revenues will stem.Much of the turnover expected from wireless data is yet to materialise. Globally, most mobile operators envisaged VoIP via 3G networks as a means of compensating for stagnating or even declining voice revenues. Despite introducing various multimedia services in addition to basic SMS messaging, the up-take so far has been slow.

Yet, far from providing an opportunity for the wireless industry, 3G networks have to some extent posed a further challenge, since they make VoIP calls over mobile networks a real possibility. This threat has prompted some mobile operators to take extreme measures. In April 2007, bothOrange and Vodafone were reported to have removed the VoIP functionality from certain branded IP-enabledNokia handsets for sale in the UK.

Conversely, mobile operator 3 has decided to seize the bull by the horns. Announcing a tie-up in late 2007, the company launched a range of Skypebranded phones that will allow users unlimited, free VoIP calls to other subscribers.3 hopes that the service, using its 3G network, will help both acquire and retain customers, while the opportunity of expanding into the mobile phone market represents a source of un-tapped revenue for Skype.

The market has witnessed some other surprising developments in recent years.Orange, in partnership with Cable andWireless, announced a fixed-line offering to UK businesses; Vodafone provides DSL services and entered into an agreement with BT to launch BT Fusion (a product solution which combines mobile and fixed line IP telephony) andO2, having merged with integrated service provider Telefónica in January 2006, has also proposed its own fixed line broadband offering. All of these 'escape strategies' are aimed at exploring new revenue streams, which complement mobile operators' core services in the short term.

Wireless IP telephony has already arrived in Europe. T-Mobile offers a mobile broadband service in the Czech Republic andOrange has trailed a similar service in Slovakia. In February 2008,Orange announced a joint pilot project with T-Mobile to provide mobile IPTV in London. The trial will use TDtv technology provided byNextWave Wireless.

Similarly, some wireless operators see significant market opportunities in delivering wireless VoIP over converged NGNs. As a result, they are moving towards internet-based networks to reduce the cost of carrying calls and facilitate new, value-added services. This trend will accelerate if, as predicted, WiFi coverage takes off in the medium term.

At the moment, it remains to be seen exactly how VoIP will impact mobile operators in the long term.Wireless companies, with greater control over their networks, will retain the ability to followOrange and Vodafone's lead and keep VoIP out of the 3G network. It is more likely however that mobile operators will imitate 3 and others such as T-Mobile in responding to demand and embracing IP-enabled calling as a way of growing and retaining their subscriber base.

P2P VoIP providers – a revolution in reality?

Skype, a company whose software enables users to make free calls to other users, has been the world's leading promoter of free VoIP. The hype surrounding its acquisition by e-Bay in 2006 and the emergence of many other players adopting the same business model (such asMSN, Yahoo and Google) highlights the significance of the P2P VoIP model and the enormous threat and additional competition that it poses to traditional telcos.

Despite their success, P2P VoIP is currently used largely as a 'second, alternative' line, mainly because of continuing concerns which are highlighted in Figure 10. These factors undermine P2P providers' prospects, as they bring into question the players' ability to provide a top class service

Figure 10: P2P VoIP challenges

P2P VoIP challenges

- Quality of Service (QoS)

- Security

- Accountability

- 'Free rider' bandwidth

- Issues with Cetrna Processing Units

- Limits set by ISP and mobile carriers

Furthermore, ISPs and mobile carriers are able to limit P2P players' access to networks by blocking servers, Internet Protocol addresses or websites. NTL (now VirginMedia), for example, regularly disabled P2P traffic when the number of connections rose above a certain comfortable limit.

To overcome these drawbacks and escape network dependence, P2P players would need to roll out their own infrastructure through WiFi or WiMAX networks. These technologies have not yet been fully proven themselves and deployment would be an expensive and time-consuming process.

Until recently, the other significant limitation of the P2P model was mobility.However, the introduction of Analogue Telephone Adaptors (ATAs) and specially enabled telephone handsets has made it possible to overcome this drawback.

Vonage's agreement withWiFi outfit The Cloud, for example, enables customers to use its service whenever they drift into one of the company's 7,000 hotspots. Similarly, SMC Networks, The Cloud and Skype have recently entered into a partnership to deliver the first mobile roaming Skype service onWiFi handsets. SMC registered handsets automatically switch to Skype when the user enters a The Cloud wireless access zone.

Currently, developments in the P2P space have been characterised by partnerships.However, as customers increasingly look for fully 'nomadic' solutions, vertical integration among mobile operators, P2P players and WiFi/Wimax providers is a real possibility.

Within this competitive environment, the future is uncertain. Companies like Skype, which was once characterised by its 'isolation' strategy, have been compelled to broaden their thinking in order to revive faltering growth. In following the more collaborative approach of Yahoo and MSN, Skype's partnership with 3 may demonstrate the way in which 'free' P2P players can chisel a profitable niche in the crowded and competitive VoIP landscape.

VoIP over Broadband providers – a true success story?

The VoIP over Broadband (VoBB) pioneer is Vonage. After its initial success in the US, the company has launched its services in the UK.Here, a different regulatory framework and market dynamics means that Vonage's market entrance has been met with less success than might have been expected. In the US, the company worked closely with cable operators to attack the incumbent telcos. In the UK, Vonage has been unable to leverage a similar advantage. British cable operators have been present in the telephony market for more than a decade and have not played the same role in driving the deployment of VoIP.

Vonage faces an on-going challenge to reduce customer acquisition costs, maintain churn down and increase ARPU. Long-term survival depends on the company's ability to retain subscribers, since the company currently needs five years to wholly amortise acquisition costs. In addition, the company has faced a series of law suits, notably for patent infringement from the likes of AT&T, Verizon and Sprint Nextel. These difficulties have not however prevented many other small players from adopting the same business model and entering the UK market. BandTelecom, Bluetalk, VoIP.co.uk or voiptalk are just a few examples.

VoIP on-demand providers

VoIP on-demand providers have introduced a completely new way of selling and distributing software and software services. The on-demand model is extremely appealing to businesses, in particular SMEs and start-ups, because it can drastically lower costs.On-demand providers, such as US based CRM solution supplier Salesforce.com, which is often cited as an on-demand standard bearer, typically develop and host new and innovative services, rolling them out by offering customers access on a useby- use basis through an internet portal.

In the VoIP space, Apptix is a prominent example. The company provides on-demand messaging and collaboration solutions at a variety of banded web addresses. In the UK, Telappliant offers a similar range of services – including hosted VoIP – under the name of 'VoipTalk'.Without expensive network assets, access to geographically unlimited users and a track record of providing innovative services, VoIP on-demand (VoIPOD) providers are in a good position to capture VoIP market share over time.

Equipment providers

In general, the telecom hand and headset market is highly concentrated, with a marked trend towards commoditisation. Major players are repositioning themselves by using demographic marketing, device life manipulation and cost cutting strategies in order to gain a competitive advantage and grow their market share.Nokia, for example, has recognised the move to commoditisation and is building a manufacturing and assembly plant in Chennai, India.

In the future, VoIP is set to be a major driver.Nokia has launched a range of handsets that switch between GSM andWiFi networks and let users shift between their mobile operator and VoIP provider as they talk. In the short term, the use of wireless technology remains problematic, due to security issues, signal failures and continued lowWiFi density.

Nevertheless, equipment manufacturers have made important strides towards developing a completely nomadic phone. RIMrecently acquired Ascendant Systems, adding sophisticated VoIP capabilities to its Blackberry devices. The move suggests that companies such as UK-basedOnRelay might also be the target of handset manufacturers in 2008.

As networks move towards triple and quad-play offerings, equipment providers are starting to compete in these areas as well.Network providers are increasingly exploring converged services that can be offered across devices regardless of access technology. The most common applications which are being targeted as a new source of revenue are multimedia and interactive services, such as video and mobile video gaming.

Innovative IPMultimedia Subsystem (IMS) architecture enables next generation, converged communications services. Despite the fact that this architecture was initially intended for wireless networks such as The Cloud, fixed operators have been the first to announce to implement IMS as they look to generate sustainable revenues from new and current customers and benefit from true service convergence, brand loyalty and new services revenues. TeliaSonera, for example, a leading Nordic telecommunications provider announced an agreement withNokia Siemens to deploy IMS across its networks inMay 2007.

Softphones, which allow the user to make VoIP calls through a desk or laptop computer without the need for a handset, have become popular in commercial networks. These are normally sold as part of large corporate IP telephony solutions from companies such as Cisco Systems, Avaya, Siemens andNortelNetworks. Consumer electronics manufacturers are also working on devices that have sufficient memory and processing capability to handle softphone calls.Hewlett- Packard's iPaq handheld, for example, can accommodate softphones and Ireland-based CiceroNetworks makes a softphone that handles calls over both cellular andWiFi networks.

Key Challenges And Threats

The widespread deployment of VoIP poses significant challenges in terms of vulnerability, regulation, convergence, mobility and the cannibalisation of revenues.

Security – a continuing major concern

IP networks have several interface points with the data network, a fact that raises multiple and significant security concerns. Eavesdropping, viruses and attempted fraud (including 'phishing' and toll or service theft), as well as local and network Denial of Service (DoS) attacks are major dangers with which VoIP providers, particularly in the enterprise sector, have to deal.

In order to guarantee security, VoIP systems have traditionally been 'isolated' from other voice and data traffic. The use of Virtual PrivateNetworks (VPNs) and Virtual Local AreaNetworks (VLANs), together with sophisticated anti-malware and firewall software from companies such asNet Clarity, insulates VoIP data packets from internal and external threats.

End-users are also being encouraged to use multiple layers of encryption. USbased Pretty Good Privacy, the company which is widely regarded as having pioneered email encryption technology, has launched a solution for VoIP. Currently, this is available only as a software product but is likely to be integrated directly into VoIP systems in the near future.

Cisco System's 2007 acquisition of IP surveillance software provider Broad Ware indicates there is life in the 'isolation' model yet.However, the convergence of voice and data services suggests that it cannot continue indefinitely. In the UK, the VoIP industry is watching with interest the 2008 launch of UMLabs, a start-up which promises integrated VoIP security.

Quality of Service – partial improvement, but problems remain

The use of public networks means that it is difficult to guaranteeQuality of Service (QoS). Conversely, a better service is feasible with private networks, normally managed by a carrier or an ISP. The problems of latency and jittery calls have, to a certain extent, been alleviated. Ateme, for example, a French encoding company, has worked with IPTV providers to successfully expand buffering capacity. Echoes and packet loss drawbacks can also be overcome by improving traffic engineering and prioritisation in the carrier network. This solution however will only apply to P2P VoIP providers if they sign agreements with ISPs, to avoid the blocking of servers IP addresses or websites.

Reliability – network outages still occur

The inability to make phone calls during a power outage is a major drawback for household VoIP services. Even with local power available, the broadband carrier itself may experience network outages. Broadband networks which are less than ten years old are still subject to intermittent interruptions, a scenario which presents opportunities for equipment manufacturers.

Currently, forward-looking VoIP gateway providers, such as Talk Switch, are integrating an 'intelligent' PSTN bypass facility in their product offering. This automatically activates in the event of a power outage, allowing VoIP users to maintain their service. It also provides the vendor with an opportunity to differentiate itself in a fragmented global market.

Scalability – the mass adoption deployment challenge

The mass adoption of VoIP raises considerable scalability challenges. Content, quality of service (QoS), redundancy, security, interoperability and manageability are key to the successful wide-spread deployment of VoIP.Network Infrastructure Vendors, such as Cisco Systems, Enterasys Secure, Extreme and FoundryNetworks, have a major opportunity here to strengthen their position in the market by offering a comprehensive solution at the deployment level.

Emergency calls – non-geographical numbers

The nature of IP means that it is difficult to geographically locate users. As a result, calls to the emergency services using VoIP cannot be easily directed to a nearby call centre, while on some systems, they are impossible to place. Some progress has been made in surmounting these problems, largely in response to regulatory concerns. IP PBX systems, such as those offered byMitel for instance, have full E911 capabilities built into the system.

Regulation – net neutrality issues enter the limelight

The debate on net neutrality, which has primarily been centred in the US, came to the public's attention with the reclassification of DSL services across public networks as 'information' rather than 'telecommunication services' in August 2005. According to the principle, carrier networks should be neutral to the packet which is being transported from source to destination and should not be able to differentiate - and, therefore, prioritise or 'deprioritise' traffic - based on its content or the service or content provider from which it stems.

In the US, several abortive attempts have been made to legislate against the provision of 'tiered' services. Strict provisions outlawingQoS differentiation were removed, for example, from the Communications Opportunity, Promotion and Enhancement Act following decisions by theHouse of Representatives and Senate Committee in June 2006. Nevertheless, discussions continue about incorporating certain elements in the Internet Freedom Preservation Act which was introduced in January 2007.

The European approach, in contrast, has been to rely on competition legislation to manage service provision. In general, the ability of carriers to differentiate between service providers – and therefore charge different prices – is seen as the natural consequence of a free market. The EC and the UK Government continues to monitor the situation. It is generally considered, however, that the introduction of legislation may discourage entry into a market with high sunk and fixed costs and, as a result, increase industry concentration. This will be an issue for VoIP because effectivelyQoS and net neutrality are in conflict. As bandwidth increases this will be less of an issue.

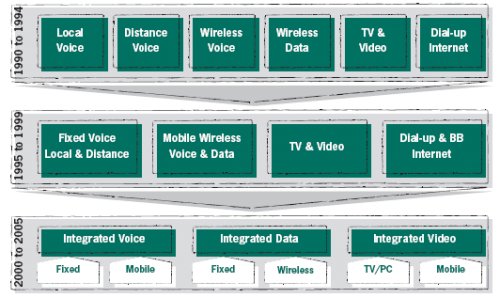

Figure 11: Evolution of converged services (1990-2005)

Source: Frost & Sullivan

Cannibalisation – PSTN revenues at risk

VoIP cannibalisation of Public Switched TelephoneNetwork (PSTN) revenues is inevitable. In order to overcome this obstacle, carriers need to develop innovative and rich value-added services, such as distance learning, video conferencing or unified messaging.

Convergence – the accelerator for VoIP

The model for selling telephony and related services has been in constant flux. In the second half of the 1990s, incumbent operators took the first tentative steps towards convergence by bundling together local and longdistance voice calls (see Figure 11). It was not, however, until the early part of this millennium that integration began to move to the network and application level.Nevertheless, bundles were still sold primarily as discrete services, with the benefit to the consumer of combined billing, lower prices and a single point of customer contact.

However, triple and even quad-play is no longer the future. VoIP is playing a major strategic role in the emergence of a new converged world. Indeed, it is the possibility of making IP calls, and sending IP data, over wireless, fixed and mobile networks which is driving the move towards complete mobility. Convenience, low-cost and the collaborative potential of combining voice, data and other services across numerous devices means that seamless fixed-mobile convergence – at a network, application and service level – is becoming a reality.

Figure 12: IP-enabled quad-play and fixed-mobile convergence (2006-2010)

Source: Frost & Sullivan

A new, burgeoning, highly competitive and innovative industry emerging

The exploitation of this disruption offers opportunities for new entrants and new markets. It is changing the status quo of an industry by increasing competition services and stimulating innovation, as the only way to provide higher value to the players involved.

Footnotes

1 Jittery calls occur as a result of voice packets not being delivered in sequential order

2 Source: BT; Press Release "Third Quarter and Nine Month Results to December 31, 2007"; released Feb 07, 2008; viewed Feb 04, 2008

3 Source: Telefonaktiebolaget LM Ericsson; Press Release "Ericsson Announces Cash Offer To Acquire Tandberg Television"; released Feb 26, 2007; viewed Feb 04, 2008

4 Source: Alcatel-Lucent; Press Release "Alcatel-Lucent Acquires Tamblin For Interactive TV Applications And Advertising"; released Sep 21, 2007; viewed Feb 04, 2008 and Tiscali UK; Press Release "Tiscali and Video Networks: Integration In The UK Market"; released Aug 12, 2006, viewed Feb 04, 2008

5 Source: BT plc; Press Release "BT Agrees To Acquire Brightview Group Ltd"; released Jul 06, 2007; viewed Feb 04, 2008

6 On October 10th 2006, Carphone Warehouse announced the acquisition of AOL UK for £370 million in cash. The acquisition transformed the combined company into the third largest UK market participant with approximately 2.3million subscribers in June 2007 (Source: Point-Topic).

7 Easynet was Virtual Private Network operator which had its own equipment in 250 local BT exchanges, providing direct access to 4.4 million homes and 850,000 businesses in the UK.

To return to the first part of this article click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.