- in United Kingdom

As alternative lenders scale, most will move from corporate facilities and overdrafts on bank standard forms to consider a "specialty finance" facility.

These facilities offer non-bank lenders their first taste of asset-backed lending and are a valuable tool in the early stages of a specialty lending business.

However, as specialty lending business grow even further, the logical next step is often to "jump" to a securitised warehouse structure (while noting that, for some originators, increasing existing borrowing (by utilising accordion features, bringing in additional senior lenders or new mezzanine lenders) may be more appropriate).

These securitised warehouse facilities are more scalable products offering favourable pricing and providing access to a new market of lenders looking to gain exposure to the originator's products.

This article sets out ten key points of difference between specialty finance and securitised warehouse structures. We hope that it is helpful to those looking to make the jump.

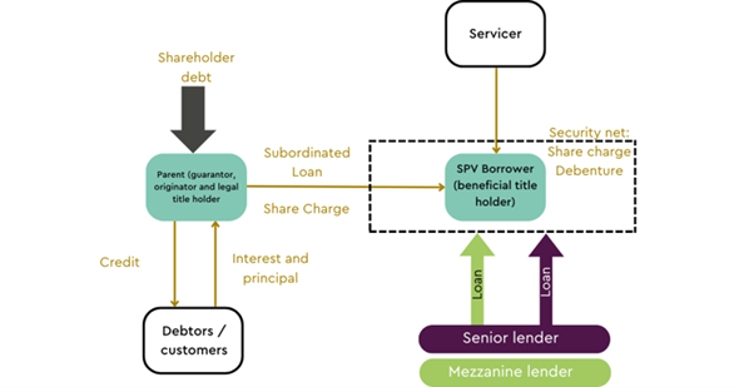

Figure 1: Specialty finance (top) vs securitised warehouse structures (bottom)

Securitised warehouse structures

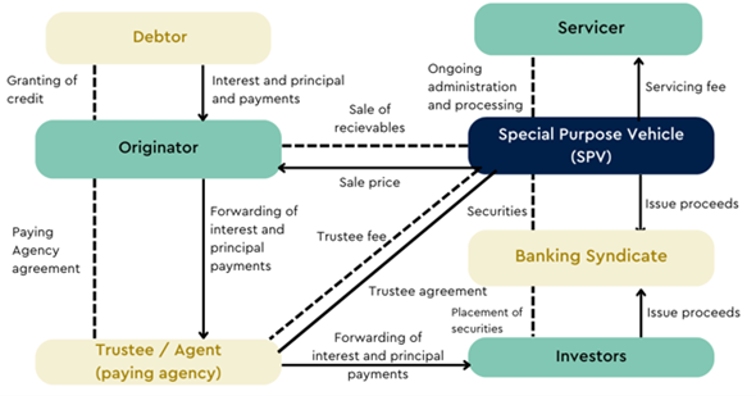

Structure of a typical securitised warehouse

- As in some (but not all) specialty finance transactions, assets (typically being the beneficial title to loans, with the ability of the transferee to require the transfer of legal title to it) are transferred to a special purpose vehicle ("SPV") that in turn issues notes and/or borrows loan finance from lenders/investors to purchase those assets from the originator.

- The SPV is a standalone entity outside of the originator group. This is a key part of securitisations and ensures that the borrower is 'insolvency remote', meaning that investor returns are wholly dependent on the performance of the receivables.

- The loans/notes issued by the SPV are in different 'tranches', often from senior to junior. These tranches govern the order of payment of receipts from the underlying assets. Each tranche may pay a fixed or floating rate of interest. Often the junior notes are retained by the originator or a member of its group (see further below).

- A trustee and other service providers are engaged to manage the cashflow from the assets and payments to investors, and to hold the portfolio on trust as security for the lenders/noteholders.

Key differences between specialty finance facilities and warehouse securitisations

| Topic | Speciality Finance | Warehouse Securitisations |

|---|---|---|

| Risk allocation | Most specialty finance transactions will include a guarantee from (for example) the borrower's ultimate parent company and/or the originator/servicer (if different). In part this is to ensure that the transaction is not a securitisation for regulatory purposes, and in part this may be a credit point for lenders (to ensure that they have recourse to the originator's wider group). | Parent company guarantees are not required in a securitisation: lender recourse is typically only to the borrower (and in practice only to its receivables and accounts). |

| As a commercial matter, the lender will require that the borrower group provide equity or subordinated debt to the borrower to bridge the gap between (i) the lender's funding (which may extend to only 70-80% of the value of the secured assets) and (ii) the full face/market value of the assets. |

Subordinated funding will be required commercially (as in specialty finance transactions). However, subordinated funding is also important as a means to meet the regulatory requirement that the borrower or its group fund a 'risk retention amount'. This is often in the form of a subordinated note or loan (although other options are available). As a regulatory matter, it can be as low as 5% of the total investment in the SPV (although, for new entrants, the amount required by the senior lenders/noteholders is likely to be driven higher by commercial consideration |

|

|

Lenders will carry out detailed due diligence on the borrower, the structure and the underlying receivables. As part of this process, management questionnaires and reports from third party services providers (such as pool audits) may be required. |

As left, save that the EU and UK Securitisation Regulations place an obligation on investors to carry out this due diligence. In practice, regulatory and commercial diligence overlap, although there is also (for example) a requirement that the risk retention mechanism be diligenced, and the investor will have the benefit of a transaction summary required to be produced by the borrower and its counsel. |

|

| Structuring |

The borrower may or may not be a newly incorporated special purpose vehicle, but is typically a member of the originator group (i.e. a subsidiary or sister company of the originating and servicing entity). Some steps are taken to insulate lenders from the risk of insolvency in the originator group (e.g. insolvency in the wider group will be an event of default, the borrower's parent will grant a share charge over the borrower's shares and there will be arrangements for servicing to continue in the case of default or insolvency of the original servicer – see below). However, the structure will not be fully "insolvency remote", i.e. there is some acceptance that insolvency in the wider originator group may affect the specialty lending structure. |

The Borrower is typically an "orphan" special purpose vehicle, with its shares held on trust by a corporate services provider. In addition to orphaning the borrower, lenders are more focused on a "true sale" of the underlying assets from the originator group to the SPV borrower (to ensure that the assets cannot be clawed back into the originator group on its insolvency). Generally this reflects a sharper focus in securitisation structures on making the borrower fully "insolvency remote" from the originator group. |

| Reporting |

Asset-level reporting and other information undertakings are negotiated between the borrower and the lenders. Typically, Loan Market Association-standard requirements for delivery of financial statements and compliance certificates are supplemented with a requirement to provide periodic data tapes and other reporting on the underlying assets and covenant compliance (typically on a monthly rather than quarterly basis). |

As left, save that the EU and UK Securitisation Regulations set out minimum requirements asset-level and structure-wide reporting, which must be provided on prescribed templates. Gearing up to comply with the requirement to report on these templates is often a significant workstream for first-time originators. |

| Documentation |

Shape of documentation Traditional specialty finance loa/ns will include a facility agreement that governs the mechanics of the loan itself. Additional agreements (often in the form of mezzanine or junior facility agreements) will also form part of the documentation where mezzanine or junior lenders form part of the structure. |

Documents may be more "joined up", with a master framework agreement or master definitions and construction schedule typically sitting across both different tranches of debt and the transaction documentation more widely. Deals are more likely to be in note format and facility documentation may include note issuance and subscription documents not often found in specialty finance transactions. This allows flexibility for listing and tranching. |

|

Servicing A servicing and back-up servicing agreement will be entered into with the originator and back-up servicer (to be exercised on an event of default). |

Typically, the warehouse structure follows this approach, but ancillary servicing-style roles such as verification agents (providing periodic reporting and verification on the underlying receivables) are more often seen. | |

|

Security Various security documents will typically be required, including all-assets security over the borrower and a share charge over the borrower. |

Security Various security documents will typically be required, including all-assets security over the borrower and a share charge over the borrower. |

|

|

Accounts Payments into and out of the Borrower's accounts are likely to be operated directly by the Borrower or members of the wider originator group. In the ordinary course, there may be no "priority of payments" or waterfall (this being replaced by confirmation that the borrower has sufficient funds to service the debt which would have been due in any such waterfall), with periodic sweeps into an account from which the borrower may freely withdraw amounts. |

Cash is likely to be pooled in a borrower account for application monthly or quarterly in accordance with a priority of payments, with administrative service providers and lenders at the top of the waterfall and origination of new receivables and remittances to the originator group towards the bottom. An external cash manager and/or paying agent may administer this waterfall. |

|

| Regulation | Typically, regulation will be limited to that affecting the underlying assets (for example, consumer credit regulations where the assets are loans to individuals) and general regulations relating to financial products under the Financial Services and Markets Act. |

Securitised warehouses will fall within the scope of:

Foreign investors may be subject to other regulations in their own jurisdiction (particularly in respect of pensions regulations (ERISA)) in the US. These requirements shape some of the features described above (e.g. risk retention and reporting). However, the scope of these regulatory requirement is very wide, meaning that regulatory structuring and advice will be required from the outset. |

This article was first published in the July 2025 issue of Butterworths Journal of International Banking and Financial Law.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]