- within Litigation, Mediation & Arbitration and Compliance topic(s)

- in United Kingdom

With trillions of dollars required to meet net-zero goals, states, industry leaders and investors are placing strategic bets on the emerging technologies touted as game-changers in the battle against climate change. From questions over the viability of hydrogen and carbon capture, to the formidable logistics of multiplying global renewable energy output, to the technical challenges of next-generation battery storage and nuclear power, much is riding on the major players choosing wisely. In a new series from Herbert Smith Freehills, our experts explore the key solutions touted as clean-power champions, assessing the commercial realities and technical dynamics at hand as the global energy industry races to remake itself for the post-carbon age.

"There's a use case and it'll happen," says Melbourne-based Herbert Smith Freehills (HSF) partner Alison Dodd assessing hydrogen's role in the energy transition. "But it hasn't become clear how widespread that role is."

It is not an easy question to answer. Despite being the universe's most abundant element, pure hydrogen on earth is difficult to source, making its journey towards the ubiquitous fuel some have prophesied bumpy at best. False dawns – as far back as the 1970s following the oil crisis and the 1990s when climate change initially shot up political agendas – have left some jaded. But complex geopolitics impacting energy security and worsening carbon emissions have transformed the debate. And with the industry receiving robust policy support from governments, and the pipeline of announced projects rapidly growing, the feeling among many observers is this time could be different.

Analysis last year from The Economist magazine noted that over 1,000 hydrogen projects are currently underway globally, while the private equity industry alone committed nearly $8 billion in 2022. The floatation in July of specialist hydrogen manufacturer Thyssenkrupp Nucera, valuing the firm around €2.5 billion in one of Europe's largest recent IPOs, was another sign of confidence.

Other significant support comes from oil majors like BP and Shell, that have the technical skills and balance sheets needed to develop hydrogen into a viable market, not to mention asset management giant BlackRock, which has made a series of investments in the sector. "Investors are cautious but open-minded and some projects are going ahead with momentum," says HSF Co-Head of Energy Nick Baker. "There has always been technological experimentation in the energy sector."

There are certainly no shortage of potential uses for the light, colourless gas, which produces no carbon dioxide when burnt, but practical challenges must be addressed around transportation, investment, regulation and supply chains. We remain years – and a string of technical breakthroughs – from hydrogen becoming a commercially viable replacement for fossil fuels; the argument has now shifted from creating a hydrogen-based economy to understanding how large a role it can carve out in the global push to decarbonise.

In the first instalment of our Chasing Zero series exploring the clean-power contenders vying to help the world win the race to net zero, we assess hydrogen's role and ask what the hopeful pragmatist's view should be.

Heavy metal or mainstream?

There is already widespread demand for hydrogen, which is used in production of chemical products and as part of a mix of gases in steel production. Ammonia production, in particular, creates huge demand; The Oxford Energy Institute estimates 35 million tonnes of hydrogen was consumed in 2020 to produce 170 million tonnes of ammonia, largely for fertilisers. The vast majority of this is classed as grey hydrogen, which is produced from fossil fuels and still generates substantial carbon emissions (see Hydrogen – Key terms below).

According to the International Energy Agency (IEA), an intergovernmental organisation, global hydrogen output hit 94 million tonnes in 2021. Low-emission hydrogen accounted for just 1 million tonnes of this.

Hydrogen – Key terms

Hydrogen

Hydrogen is a chemical element with the symbol H and atomic number 1. The most abundant and simplest element in the universe, hydrogen in its common gas form is colourless and odourless. Though non-toxic, it is highly combustible. Pure hydrogen is rare on earth and is instead found in molecular forms such as water and organic compounds.

Grey hydrogen

Hydrogen created from natural gas, or methane, using steam methane reformation but without capturing the greenhouse gases made in the process. Grey hydrogen comprises the vast majority of global output today and is responsible for significant carbon emissions.

Blue hydrogen

Hydrogen produced mainly from natural gas, using a process called steam reforming, which brings together natural gas and heated water in the form of steam. The carbon dioxide emitted through the process is mitigated through use of carbon capture and storage. Blue hydrogen is sometimes called low-carbon hydrogen.

Green hydrogen

The grail in hydrogen's long-term allure for the energy transition. This is hydrogen made using electricity from surplus renewable energy sources, such as solar or wind power, to electrolyse water. Electrolysers use an electrochemical reaction to split water into its components of hydrogen and oxygen, emitting zero carbon dioxide in the process. Green hydrogen makes up a tiny percentage of overall global hydrogen production but is growing. Dramatic increases in renewable power output and equally striking falls in the cost of electrolysis components are two considerable challenges to tackle.

Electrolysis

The process of using electricity to split water into hydrogen and oxygen, enabling the production of pure hydrogen. This reaction takes place in a unit called an electrolyser.

While such figures make downbeat reading, there is a positive takeaway: if the current hydrogen output was generated sustainably, it would itself amount to a meaningful decarbonisation effort and provide a platform for hydrogen in the wider energy transition. The IEA itself forecasts green hydrogen – produced by splitting hydrogen from water with renewable electricity – could ultimately provide up to 10% of global energy use by 2050.

If cleaning up existing hydrogen use would be a major step forward, the debate is how far hydrogen can be used to decarbonise other activities. The emerging consensus is that the clearest use is in hard-to-decarbonise areas of the economy, such as heavy industry, where it enjoys a competitive advantage over other forms of renewable energy due to its energy density and ability to use existing infrastructure. Steelmaking is a key example. The industry is responsible for 7-9% of global emissions and, as manufacturers move towards electric arc furnaces, there appears few sustainable alternatives to hydrogen.

Martin Lambert, head of hydrogen research at The Oxford Energy Institute, sets out likely scenarios: "Hydrogen will play an important role, but not in all the areas people have talked about. Its role will be as an industrial-scale product. Task number one is to decarbonise current hydrogen in refineries, ammonia plants and chemical plants, and then move on to decarbonise steelmaking."

In October 2023, Energy giant ENGIE and South-Korean steelmaker POSCO announced they would work together on creating a green steel facility in the Pilbara region of Western Australia. The project will use a model considered by many to be the most viable: renewable energy (inland wind and solar) used locally to power an electrolyser to generate hydrogen which is then piped to a hot briquetted iron facility. The much-touted H2 Green Steel project, which has secured more than €6 billion in funding to build the world's first large-scale green steel plant in Northern Sweden, is another flagship project (see Fuel futurists – Pioneering hydrogen projects below). Using hydrogen in steel production also enables the fuel to be generated close to deployment, mitigating transportation challenges.

Hydrogen – Perspectives in law and project development

"Without question, currently hydrogen's greatest potential is in green steel," says Angus Leslie Melville, editorial director of infrastructure and projects journal IJGlobal. "It's a perfect example of how you can have windfarms creating green energy to power the electrolysers creating hydrogen which replaces traditional fuel sources. These projects are no brainers."

There are also persuasive arguments for hydrogen in large-scale transportation, particularly shipping, which according to the EU is responsible for about 3% of global emissions, and aviation (around 2% of total emissions). Use in heavy road transport is also potentially viable.

Some projects envisage wider use, such as BP's joint venture with Aberdeen City Council – The Aberdeen Hydrogen Hub. The idea is to construct a green hydrogen production, storage and distribution facility in Scotland powered by renewable energy. This would see green hydrogen deployed at a refuelling facility for buses and trucks before being scaled to produce fuel for wider road, freight, rail and marine use. Ultimately, the hub envisages hydrogen having a much longer reach by providing heat in buildings and being exported.

"For all the energy majors it's part of the strategy," says HSF's Co-Head of Energy Lewis McDonald. "Exxon, Chevron, Shell, TotalEnergies, BP and all the others. The analogue is liquefied natural gas (LNG), especially in the international component, so they're the natural companies to move into this space."

UK

The Aberdeen Hydrogen Hub

This joint venture between oil giant BP and Aberdeen City Council aims to create a scalable green hydrogen production, storage and distribution facility in Aberdeen powered by renewable energy. The target is for the facility to produce over 800 kilograms of green hydrogen per day from 2024 – enough to fuel 25 buses and a similar number of other fleet vehicles. The ultimate hope, however, is to create enough hydrogen to heat buildings and export.

HyGreen Teeside

Another major play from BP, HyGreen Teeside hopes to become one of the largest hydrogen production facilities in the UK by using solar and wind to generate hydrogen made through electrolysis. The project has ambitious targets: 80MW of green hydrogen capacity by 2025 growing to 500MW by 2030.

Pioneer1

Green hydrogen services provider Protium has successfully deployed one of the first operational hydrogen production facilities in the UK, Pioneer1. Sited on the University of South Wales Hydrogen Centre in Baglan, the hub has been a source of hydrogen for local bus trials and numerous businesses. The company is also eyeing another hub: Pioneer 2, which hopes to provide further green hydrogen to Welsh businesses and transport.

Europe

H2 Green Steel

A greenfield project located in northern Sweden, a region rich in hydropower, H2 Green Steel is hoping to create the world's first large-scale green steel plant, having recently secured €4.2 billion in debt financing. A relatively advanced project due to start producing "green steel" before the end of 2025, total funding to date amounts to €6.5 billion. The project has captured industry attention, as it includes a giga-scale hydrogen plant fully integrated into the steel production facility.

CIP Hydrogen Island

Danish investment firm Copenhagen Infrastructure Partners (CIP) is leading plans to create an "artificial island" dedicated to large-scale production of green hydrogen from offshore wind in the North Sea. CIP envisages the island being an integral supplier of European hydrogen as the continent looks to secure its future green energy supplies.

Wilhelmshaven Hydrogen Hub

BP is planning a move in Germany by exploring the construction of a hydrogen hub in Wilhelmshaven. The hub would include an ammonia cracking facility, which could potentially supply 130,000 tonnes of low-carbon hydrogen from green ammonia, annually from 2028. Additionally, BP plans to use current oil and gas pipelines for transporting the hydrogen, enabling delivery to customers in the Ruhr region and other centres of demand.

Middle East

NEOM

The new city development in the Kingdom of Saudi Arabia is perhaps the world's most ambitious renewable energy project. The city aims to harness an abundance of wind and solar resource potential, which in turn can produce huge amounts of sustainable hydrogen. In May, an $8.4 billion financing closed on the NEOM Green Hydrogen Project, which hopes to build the world's largest green hydrogen facility.

Asia Pacific

Hunter Valley Hydrogen Hub

An Australia-based joint venture between Origin Energy and mining and infrastructure group Orica, the Hunter Valley Hydrogen Hub aims to deliver a commercial-scale hydrogen supply chain in the Newcastle industrial and port precinct. In particular, the hub is targeting decarbonisation of Orica's nearby ammonia manufacturing plant by replacing existing natural gas feedstock with hydrogen produced through electrolysis.

Asian Renewable Energy Hub (AREH):

Located on a 6,500-square kilometre site in the Pilbara region of Western Australia, the multi-billion-dollar AREH has lofty aims. Firstly, the hub hopes to utilise up to 26GW of solar and wind power and produce around 1.6 million tonnes of hydrogen per year. This hydrogen can then be exported into wider Asia to help propel the region's energy transition. The project is majority owned by BP, but InterContinental Energy, CWP Global and Macquarie's Green Investment Group are all equity holders.

Huge asks

Perhaps the greatest obstacle hydrogen faces is that current renewable energy capacity is nowhere near large enough to create the amount of green hydrogen required for 2050 climate goals. Lambert comments: "Building enough renewable power is mind-blowing. The European Commission came up with 10 million tonnes of hydrogen being produced by 2030. That needs at least 150GW of electrolyser capacity and renewable power to happen. We need a lot more renewable power to carry on decarbonising the grid and to have another 150GW on top, it's a huge ask."

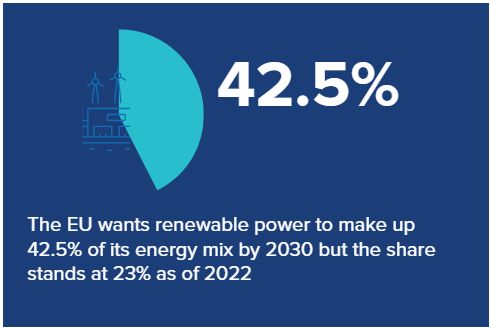

While energy security concerns have concentrated minds on the need to ramp up renewable energy production, there is a long way to go. The EU wants renewable power to make up 42.5% of its energy mix by 2030 but the share stands at 23% as of 2022. And despite the US, UK and Australia having certain advantages in generating renewable energy, there are still significant shortfalls.

Then there are electrolysers themselves, which are underproduced due to costs and difficulties in sourcing components, though the growth of solar and wind power suggests such costs will rapidly fall with rising production. Where that production happens will also be of interest amid fears that China is rapidly cornering the market.

Hydrogen business consultant David Scrimgeour notes: "While the West takes a while to get its act together, China is rolling out more projects. They're already big in electrolyser production and will get bigger. They are the one to watch."

But the other key challenge is the difficulty of transporting hydrogen, which in its normal gas form is harder to contain and move than methane gas, meaning projects either require major infrastructure upgrades or to be built on the doorstep of end-users. Advances in transportation – potentially via upgraded pipelines or shipping or more economic forms of compression, chemical conversion or liquification – would be a big step forward in building a global market to trade hydrogen as with fossil fuels.

Notes Dodd: "The transport challenges are real; the consumer safety challenges are real; also, the rollout challenges when you think of all the regulatory changes needed. In Australia, our regulations are different across different states, so you need legislative changes to inject hydrogen into gas pipelines and gas networks. Those changes are being made but they're slow and piecemeal."

States step in

With challenges ahead, industry players are looking to meaningful state support to attract capital and manage project risk until markets and supply chains can develop.

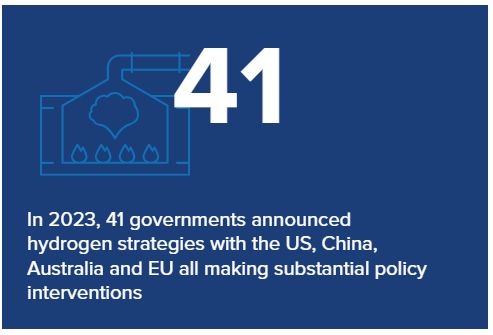

There has already been considerable progress with the IEA last year citing formal hydrogen strategies by 41 governments with the US, China, Australia and EU all making substantial policy interventions. Arguably the most striking example is in the US, where the Inflation Reduction Act (IRA) offers a generous $3/kg in subsidy for green hydrogen projects. The European Commission, meanwhile, is creating a "hydrogen bank" with €800 million from the EU's innovation fund for low-carbon technologies to subsidise hydrogen fuel. Similarly, the UK Government announced in December 11 hydrogen projects which would receive state backing as part of a £2 billion commitment. Elsewhere, Australia has committed up to A$2 billion to support its hydrogen industry through its Hydrogen Headstart Program.

HSF corporate partner Steven Dalton comments: "You need government to stimulate supply, and that will get us some demand. You then need governments to provide volume protection, or offtake protection, and underwrite drops in revenue if purchasers don't buy hydrogen because they're not ready or don't have the money. That's the number one thing." Such regimes and incentives are now emerging globally. In the UK, the government has produced its Low Carbon Hydrogen Agreement, which provides various means of support for hydrogen projects. Essentially, the agreement focuses on stabilising revenue through mitigating commodity price risk, volume risk and political risk to enable a project to attract financing.

Simon Currie, chief project officer at specialist energy developer Energy Estate, puts in context how quickly governments have swung behind hydrogen: "It's the speed at which countries have moved which is the most significant. Canada is responding to the IRA. Japan's contract for difference programme is being launched this year. Germany is already having auction rounds. This is unparalleled in the history of the energy industry."

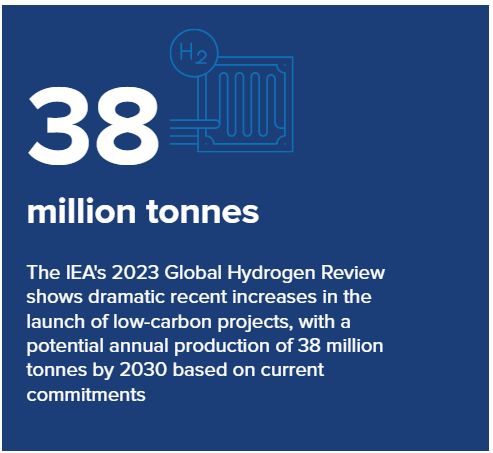

Government support is feeding through into private sector commitments. The IEA's 2023 Global Hydrogen Review shows dramatic recent increases in the launch of low-carbon projects, with a potential annual production of 38 million tonnes by 2030 based on current commitments. Of this output, only 4% have taken a final investment decision, reflecting the industry's infancy, though this has doubled since last year in absolute terms. More than two-thirds of announced projects are for green hydrogen, with the remaining capacity targeting grey equivalents. Further market support is emerging with current global falls in inflation, promising falling financing and equipment costs, a substantial boost for the economics of hydrogen projects, which are capital intensive across the value chain.

As meaningful incentives start to emerge, focus shifts also to the prospect of credible penalties to support an emerging market. "A carbon price applicable to industry where it isn't taken away by free allowances would be a huge signal the time has come," argues McDonald. "But a global carbon price is a way off, it'll be too hard for developing countries to absorb that." In the meantime, the key development to watch is the EU's Carbon Border Adjustment Mechanism, which will fully launch in 2026. This is designed to stop foreign importers of carbon-intensive commodities such as hydrogen, steel, cement, iron, aluminium, electricity and fertilisers undercutting local manufacturers forced to pay higher levies for their emissions and looks the best immediate prospect of ushering in credible carbon pricing.

Dalton says: "We need some clarity on regulation on importing into Europe and the UK from a carbon emission treating perspective. But the most meaningful thing we can have comes down to government support in early stages to stimulate supply while demand matures."

A surgical solution

While it is easy to imagine green energy sources working together to tackle climate change, these sectors are often competing to demonstrate their utility at scale and lustre to investors. The areas hydrogen appears the most competitive come back to a handful of fields: ammonia production, steelmaking, shipping and (arguably) aviation – all hard-to-abate activities.

Heating remains more contentious: in October the UK's National Infrastructure Commission said the government should rule out hydrogen for heating buildings, instead focusing on heat pumps. The European Commission is mulling blending hydrogen with conventional gas in existing networks as a workaround which could also stimulate demand. But breakthroughs in battery power have tilted the balance of heavier road transport towards electric vehicle solutions. The debate continues but wider transport applications are often viewed as riskier investments. The shorthand is hydrogen is strongly positioned as an industrial not consumer product.

The medium-term likelihood of increasing capacity and falling costs of renewable power and cheaper hydrogen production, mean the greatest immediate uncertainty over the scope of the industry lies in the success or failure of substantial advances in transporting hydrogen.

"If you can get a significant reduction in the cost of delivery, that's a bigger game-changer than tax," notes Baker. Governments, likewise, need to turn enthusiastic policy support and targets into workable regulation and subsidy schemes that can stimulate demand and de-risk investment.

"I am a great believer in the role green hydrogen will play in the energy transition," says Currie. "The mistake is to assume it will happen overnight. Cast your mind to LNG, it took years, and sometimes decades, to develop the projects and ship new sources of gas to customers."

Such thinking reflects a newfound pragmatism – hydrogen is not the elixir to decarbonise the world, its appeal is a targeted, tactical part of the energy transition, a specialist role that becomes vast if applied globally. "Hydrogen is not a silver bullet. It's not the complete answer," says Leslie Melville. "But hydrogen will undoubtedly be a central part of the mix as we move towards net zero."

"People aren't put off by the challenges," concludes Baker. "Unlike renewables, hydrogen will be led and delivered by a smaller set of larger and more traditional clients. Those are organisations full of experienced engineers and they will solve the problems."

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.