- within Insurance, Real Estate and Construction and Consumer Protection topic(s)

The DECC is inviting comment on the draft OGA Strategy to maximise the economic recovery of petroleum in the UK. The Strategy builds on the industry-led review of the sector, giving effect to the recommendations of the Wood Review. It enshrines as a "Central Obligation" that relevant persons should take all steps necessary to secure that the maximum value of economically recoverable petroleum is recovered from UK waters, while also seeking to maintain investor confidence and ensure compliance with existing HSE legislation. The Strategy could result in a very different approach being required by all stakeholders to meet their obligations in support of the Strategy and wide ranging powers will be given to the OGA to police this. Given the nature of the changes, stakeholders are being asked to share their views on the draft, and particularly whether it provides sufficient clarity and guidance on what will ultimately be a fundamental change of approach.

Background

On 18 November 2015, the Department of Energy and Climate Change (the "DECC") published its consultation paper setting out and inviting views on the draft strategy of the UK Oil and Gas Authority (the "OGA") for the maximisation of economic recovery of petroleum from the UK Continental Shelf (the "UKCS") (the "Strategy"). The consultation will run until 8 January 2016 and a final draft of the Strategy is expected to be presented to Parliament in early 2016.

The intention is that the related legislation will come into force by April 2016, whereupon the Strategy will be binding on the Secretary of State, the OGA and certain persons operating in the UKCS, including holders of offshore petroleum licences, operators appointed under those licences, operators of upstream petroleum infrastructure and persons planning and carrying out the commissioning of upstream petroleum infrastructure. It is possible that, under provisions under consultation in the Energy Bill currently before Parliament1 (the "Energy Bill"), it may also be extended to cover persons operating offshore installations.

Outline of the Strategy

The draft Strategy has been produced as a result of Section 1A of the Petroleum Act 1998 (as amended by the Infrastructure Act 2015), which requires the Secretary of State to produce a strategy for achieving the principal objective of maximising the economic recovery of petroleum from UK waters.

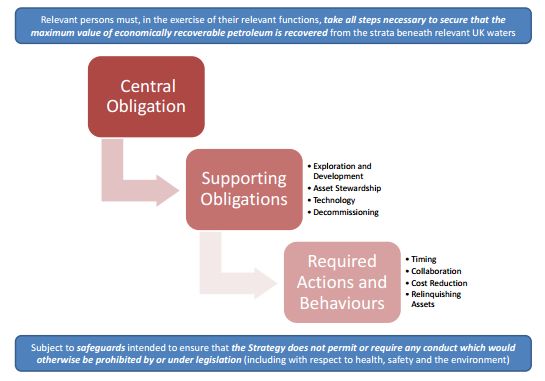

The Strategy wishes to make investor confidence a priority, acknowledging the need to provide a stable and predictable system of regulation that encourages investment as well as a collaborative approach. It includes a number of noteworthy features:

- A Central Obligation underpins the Strategy, that relevant persons should take all steps necessary to secure that the maximum value of economically recoverable petroleum is recovered from UK waters.

- Supporting Obligations provide further detail as to what is

expected of relevant persons in support of the Central Obligation.

These Supporting Obligations focus on the following areas:

- Exploration - obliging relevant persons to undertake exploration activity, especially if they have committed to work programmes;

- Development - requiring the planning, commissioning and construction of infrastructure in a way that optimises recovery, including giving due consideration to whether infrastructure could be of benefit to others;

- Asset Stewardship - ensuring that infrastructure is maintained appropriately to achieve optimum levels of performance;

- Technology - ensuring relevant persons deploy new and emerging technologies to maximise recovery; and

- Decommissioning - requiring owners of infrastructure to explore all options for the continued use of infrastructure before commencing decommissioning.

- The OGA is to be granted broad powers to publish plans setting out how the various obligations under the Strategy may be met. These plans may be targeted at individual entities or groups of relevant persons, and should any relevant person wish to deviate from an OGA plan, it will need to consult first with the OGA.

- The Strategy elaborates as to how relevant persons may demonstrate compliance with the Central and Supporting Obligations, by setting out a series of required actions and behaviours, including compliance in a timely fashion, collaboration and co-operation with others, cost reductions and, ultimately, the relinquishment of assets.

- Under the Energy Bill, new powers would be granted to the OGA to allow it to implement the Strategy, including the right to obtain data and samples from operators, attend meetings, issue non-binding declarations and (at the more draconian end) impose sanctions such as enforcement notices, fines, revocations of licences and removal of operatorships. If relevant persons decide not to ensure the recovery of the maximum value of economically recoverable petroleum from their licences or infrastructure, the Strategy may entitle OGA to require a party to divest licences or assets for fair market value2.

- The Strategy outlines certain safeguards for its implementation. None of the obligations will permit or require conduct which would be prohibited under legislation (including HSE matters), and no obligation imposed under the Strategy will require a person to make an investment or fund an activity where they will not make a satisfactory expected commercial return.

- The definitions of "economically recoverable" and "satisfactory expected commercial return" therefore become key to setting the boundaries for what can be expected by participants in the region. The economically recoverable standard is an objective test judged by what is recoverable by any person, bearing in mind their particular circumstances. A "satisfactory expected commercial return" is to be assessed by what is reasonable in the circumstances and in light of the complexity of the relevant project (more complex projects may therefore justify the requirement of a higher rate of return by participants).

Initial Observations

At a high level, the decision to launch a consultation should be welcomed. This is important for creating a sensible and workable regulatory framework for implementing the recommendations of the Wood Review, which can then address industry needs and concerns in an appropriate way.

The Strategy has a number of positive aspects that should be welcomed by the industry:

- The continued movement of powers from the Secretary of State to the OGA, the new, better resourced, arm's length body which is funded by industry, is noteworthy. In light of the need to maintain and support investor confidence and achieve the Central Objective, this shift of power away from the political arena to an independent body with deeper industry expertise will allow for a more sophisticated approach to regulation.

- It provides for an approach that might be described as "guidance before intervention". It acknowledges that there may need to be flexibility in regulation of the sector, and opens the door for non-compliance with OGA plans following consultation. Most notably, the Strategy preserves the sanctity of bilateral contracts and stresses that obligations cannot be imposed where the immediate direct benefit would be outweighed by the resulting damage to investor confidence. It is to be welcomed that the consultation paper acknowledges that it will be for private parties to determine how they best reflect the Strategy in their contractual arrangements.

- The obligation for prior consultation with the OGA before derogation from a plan should ensure that the regulator is fully informed and able to apply its powers in the most appropriate way. It is to be hoped that, over time, the OGA will build up a body of additional guidance and interpretation that is publicly available to better guide participants in the industry.

- The Strategy is very clear in the way it affirms fundamental safeguards relating to the application of the obligations. This draws a very clear line for investors and industry participants alike as to where the limits of its obligations will lie, and should provide comfort to investors that the push to maximise economic recovery will neither cut across existing legislative requirements nor encourage the OGA to engage in deal-making in order to achieve the Central Obligation.

- The articulation of the Strategy provides important insight into the thinking of the DECC and, therefore, some of the relevant considerations for the Secretary of State for Energy and Climate Change (currently) and the OGA (in the future) when exercising powers under the relevant legislation. This will, in turn, better enable participants to predict whether proposed transactions will be permissible and to explain the rationale for proposed transactions.

However, while the ideals behind the Strategy and the Central Obligation in particular should be seen as positive for the industry, and therefore beneficial to the sector, there are a number of concerns which will require further thought and discussion:

- How will the Strategy be applied in differing economic environments? It remains to be seen how the OGA will interpret the need to "maximise the value of economically recoverable petroleum" in a low oil price environment. A low oil price discourages development; participants may be reluctant to be pressured into a particular project or production rate, or to collaborate with competitors to provide routes to market that only continue to depress prices by increasing supply. Further guidance is required from the OGA as to what they perceive to be the maximisation of value at different stages in the economic cycle.

- The Strategy in its current form puts greater pressure on the way operators manage their internal data and information flows, and, where relevant, the content of their announcements to the market. Operators may need to justify their calculations of economic recovery in order to rebut any allegations to the contrary from the OGA. We have concerns that the definition of what is economically recoverable is subject to an objective test. Is it really right that private investors should have to worry about whether a public regulator will agree with its own interpretations of where the tipping point of value lies? We would query whether it is workable in practice to expect a regulator to dictate what is "economic" and what is not, and whether it is realistic to expect the OGA to have the manpower or the expertise to test a relevant person's own calculations and conclusions. As a result, we would question how easily the OGA would be able to enforce this Strategy.

- Concerns over a perceived increase in the risk of regulatory intervention may undermine one of the core aims of the Strategy – that of investor confidence. The prominence of the OGA's power to require relinquishments under certain circumstances could deter investors from an already challenging North Sea market. For the Strategy to succeed, further clarification of the scope of the OGA's powers, and its willingness to use them, will be crucial. Careful consideration needs also to be given to the impact that the Strategy and its implementation may have on the international competitiveness of the UKCS – for example, investors might be deterred by the powers to be granted to the OGA when considering competing investments in the UKCS and other comparable petroleum producing nations (for example, Norway).

- Is the brevity of the Strategy the right approach? The objectives of the Strategy are admirable, but are often conceptual and can conflict with one another. For instance, how will the OGA oblige a person to complete a work programme as set out in a licence, if no person will be required to fund an activity where they will not make a satisfactory commercial return? As noted above, how does the threat of forced relinquishment tally with the need to prioritise investor confidence? There remain questions as to how the Strategy will work in practice. In order to be effective, the consultation will need to clarify the Strategy's internal contradictions and specify which objectives take precedence, and how, in cases of conflict. In striving for economy of text, there is a risk that the OGA creates uncertainty in the market, at least until there is a body of evidence to demonstrate how it will act when implementing the Strategy.

Your Views

We think that, overall, the Strategy is a step forward in the implementation of the Wood Review, but that further guidance and detail is needed, particularly from the OGA, as to how the Strategy will be interpreted and implemented if it is to create the stable and predictable system of regulation that is desired. We would be delighted to hear from you as to whether you share our views – please get in touch with your Shearman & Sterling contacts if you wish to be part of the discussion.

Footnotes

1 [HL] 2015-16

2 While this might seem quite invasive, the consultation paper notes that there have been examples of required divestment in the UKCS in the past. Recently, Letter One was required to make disposals of North Sea assets to Ineos, albeit for different circumstances, and although not a divestment, a 2010 DECC Decision Notice was issued on the Rhum Field in relation to the interests of one JV partner on the grounds that it was "necessary to apply a temporary scheme to IOC's hydrocarbons interests...to prevent permanent destruction of the value of the relevant licence." Production of gas from the Rhum Field had ceased in 2010 due to the application of the sanctions against Iran as IOC was a subsidiary of the National Iranian Oil Company.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.