Are insurance buying strategies linked to risk appetite or are boards being led by fear where data isn't present?

Welcome to the next blog post in our 'Bridging The Gap series'. This time we are investigating the suggestion that insurance buying decisions are being driven by fear due to a lack of data driven advice.

In the mind of a director

We can all appreciate that controlling risk within a firm is a constant battle for risk managers and their boards. They are faced with regular reminders of the risks they are exposed to, under pressure from shareholders to make financial returns and have the potential of personal scrutiny looming over them from the regulator. Given the consistency of this pressure it was interesting to see a marked increase in the perception of risk felt by directors in WTW's Global Directors' and Officers' Survey Report 2024.

WTW's Global D&O Survey is published annually and aims to identify and analyse the top risks perceived by directors and officers worldwide, tracking shifts in risk priorities and uncovering emerging threats.

47%

Comparative increase in perception of risk as being very or extremely important for D&Os of FIs according to the Global Directors' and Officers' Survey Report 2024 vs 2023.

Over the five years that WTW has published this study, directors of financial institutions have consistently shown greater concern than their non-FI peers for the risks discussed. Despite this already high level of risk awareness, in the most recent study there was a 47% jump in directors of financial institutions indicating that risks were very or extremely important to their organisation compared to the 2023 study.

Whilst risk awareness shouldn't automatically be considered risk aversion, especially when greater risk can lead to greater rewards, the trend may help explain why when it comes to insurance many boards consider themselves to be risk adverse.

Is a lack of data leaving boards acting on fear over facts?

Our data shows firms have notably lower risk appetite for risks which are likely to be caused by failure of a board's own management team. Does this suggest personal accountability is top of directors' minds? Interestingly, insurance policies which are triggered by management failure are on average bought to cover a loss four times as severe as those triggered by technology or control failures.

A D&O claim is 69% more likely to be triggered by a management failure than a PI claim.

Let us consider two liability insurances, Directors' & Officers' insurance (D&O) and Professional Indemnity insurance (PI), which are both most commonly triggered by a management failure. A D&O claim is 69% more likely to be triggered by a management failure than a PI claim. There is a stark correlation with insurance limits, which are bought to a 67% higher level of probability. This correlation continues when you consider other liability insurances such as Crime and Cyber.

Is this a deliberate strategy linked to their firm's risk appetite or are boards being led by fear where data isn't present?

Does this leave other areas underexposed?

Whilst we have identified strong correlation, the inconsistency of clients buying habits within, and between, firms suggests that boards are lacking information to support the development of a consistent programme strategy. This supports our previous observation that over reliance on benchmarking is leaving firms with gaps in coverage. Without the data to show how likely different events are, board members should be expected respond to emotional triggers.

Inconsistency of insurance buying strategies

WTW has analysed more than 14k liability claims made by financial institutions since 2008. These losses are incorporated into our dedicated risk quantification models which evaluate your current and potential insurance structures to gauge the adequacy of different options and provide data driven recommendations.

But where does this leave the other risks? Should we be concerned that they are being left underinsured? And what should boards do about it when budgets are tight?

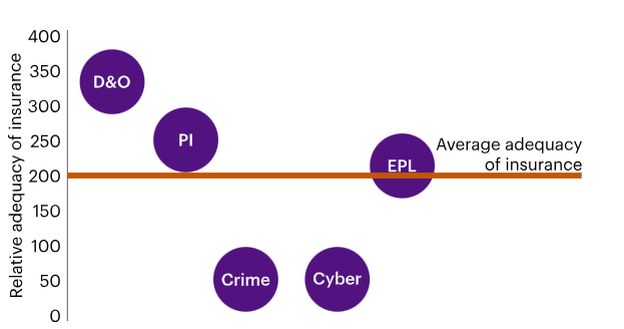

A case study

Having data on which to base decisions allows you to compare the value of spending a dollar to cover one exposure over another. Take for example, Bank A. Bank A buys PI, Crime, Cyber and D&O insurance based on peer benchmarking. When we delve deeper and consider the likelihood that these policy limits are sufficient, using our proprietary risk quantification models, we see that whilst a breach of their PI limit is extremely unlikely their Cyber limit could be breached by a 1 in 10-year event. This information gives the board the power to save premium by reducing the PI limit and invest in additional Cyber cover. Their firm is better protected, and no more money has been spent.

...using our proprietary risk quantification models, we see that whilst a breach of their PI limit is extremely unlikely their Cyber limit could be breached by a 1 in 10 year event.

Empowering board members

Insurance isn't just an expense line on your balance sheet, it's a critical financial tool underpinning your business. Ensuring your board receives the data it needs to make sound decisions is critical. Contact WTW to understand how we can empower your board and develop an insurance strategy fit for your firm.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.