For those of us based in the UK, summer 2023 has taken a turn for the worse weather-wise. Sunny June has been replaced by a wet and grey July.

Events of this week bring back into focus the ever – present and increasingly prevalent threat to property insurers posed by 'flash flooding'. In London this week a driver had to be rescued from their car due to flash flooding. The BBC and other news outlets reported that an area of one square mile was flooded to a depth of around one metre, with six fire engines and forty fire fighters being called out to assist members of the public.

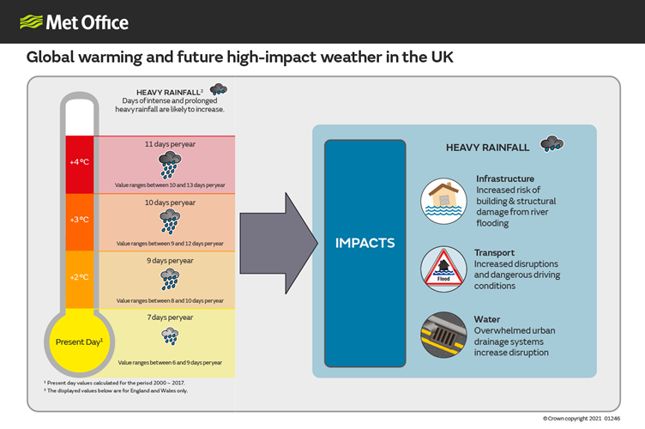

According to the Met Office, the latest set of climate projections (UKCP18) show that climate change will lead to more intense rainfall in the summer period, with the frequency of events of extremely heavy rainfall akin to flash flooding set to increase by around 25%. This will be particularly the case in urban areas, where a lack of appropriate drainage can overwhelm the infrastructure.

Since the inception of 'Flood Re', the issue of domestic property owners being left uninsured in respect of flooding events or an extreme (and often seasonal) deluge of property claims relating to flooding at domestic properties has markedly abated.

However, Flood Re does not, of course, cover commercial premises, nor certain other categories of premises, including properties forming part of a landlord's rental portfolio, blocks of three or more residential flats or multi – use properties under commercial or private ownership. In any event, Flood Re will come to an end in 2039 and there will once again be a free market for flood risk insurance.

Insurers will sometimes seek to expressly exclude flood cover, often because the property is located in an area known to be prone to flooding. However, it is important to understand what a 'flood' really is and whether a court would agree that a set of circumstances truly constitutes a flood, as opposed to a storm or some other event which might still be covered under the policy.

Ideally, the policy would be clearly drafted to include a precise definition of a 'flood' or 'flooding'. This is likely to be the first place a court would look in order to ascertain the underwriter's intention in respect of the intended operation of the cover.

In the absence of a definition, the court would look at a number of other sources for guidance.

The Oxford English Dictionary definition of 'flood' is as follows:

"An overflowing of a large amount of water beyond its normal confines, especially over what is normally dry land" (the noun);

"To cover or submerge (a place or area) with water in a flood" (verb)

In the Court of Appeal decision of Rohan Investments v Cunningham and Other Members of Syndicate 877 at Lloyd's (t/a Criterion Insurance Services) the court set out some guidance in relation to what constitutes a flood. The court in this case held that one should give the word 'flood' its natural and ordinary meaning and whether a flood has occurred should be considered in the context of the size of the property relative to the amount of water. For insurance purposes, the focus ought to be on whether water entered the property and caused damage.

In the judgment of the High Court in the case of The Board of Trustees of the Tate Gallery v Duffy Construction Jackson J held that the following factors are relevant in order to ascertain whether the arrival of water on property constitutes a flood:

(a) whether the source of the water was natural

(b) whether the source of the water was internal or external

(c) the quantity of water

(d) the manner of its arrival

(e) the area and character of the property upon which the water was deposited and

(f) whether the water was a normal event.

Usefully, there is a statutory definition of 'flood'. The Flood Risk Regulations define 'flood' in quite a straightforward manner as "any case where land not normally covered by water becomes covered by water".

However, as can be seen from the above, there is no uniform definition of 'flood' in England and Wales.

Property insurers are therefore well advised to be alive to this and to ensure that policy wordings contain clear definitions and that any exclusion for flood cover is absolutely watertight (no pun intended), so that there can be no reasonable argument that the claim is covered elsewhere under the policy.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.