- within Finance and Banking topic(s)

- within Compliance, Strategy and Insolvency/Bankruptcy/Re-Structuring topic(s)

Portability has featured in European leveraged debt markets for some time. Over 70% of sponsored high yield deals have included leveraged based portability in each year since 20231. Whilst less frequently seen in loans, European syndicated TLB saw an increase in portability features in 2025 with such features appearing in 20% of loan documents compared to 5% in 20242. The U.S. loan market is seeing a similar trend, although the incidence of portability appears to be lower overall than it is in Europe.

We also know (though market reporting is limited) that portability has featured in some private debt deals.

WHAT ARE THE DRIVERS FOR PORTABILITY'S INCREASED POPULARITY IN EUROPEAN LOANS?

Ongoing mismatched price expectations, the muted M&A market, and the interest rate environment have all made it harder for sponsors to realize investments by way of third party sales. As a result, assets are being held for longer. Whether there is a specific transaction on the horizon or not, sponsors are looking to minimize cost and execution risk for any potential buyer on an exit. An option to keep the existing financing in place can be helpful, particularly for buyers wary of market conditions or for whom new money financing is not available on the desired terms. On the debt side, new issuance leveraged loans for buyouts have been in short supply for some time, with the majority of activity coming from incremental facilities, amend-and-extend transactions, repricings and refinancings. The pronounced supply/demand imbalance for new paper has driven the inclusion of more sponsor friendly terms.

WHY HAS IT BEEN MORE COMMON IN HIGH YIELD BONDS?

Recent conditions are common across markets and products, yet portability is a more established feature in the high yield market in both Europe and the U.S..

Loan lenders have always placed importance on the identity of the sponsor as the ultimate owner of the business, whereas high yield bond investors are generally more accustomed to trading in and out of positions. Historically sponsors may have felt more confident to rely on the easier consent process available in the loans market if necessary compared to the high yield bond market, and so did not feel the need to include a specific permission up front unless they had a particular planned exit in mind.

WHAT CONDITIONS ARE APPLIED TO THE EXERCISE OF PORTABILITY?

In European loans, portability is a carve out to the standard change of control mandatory prepayment which otherwise typically triggers an individual lender put right. In U.S. loans, portability is commonly a carve out to the standard change of control event of default.

In high yield bond documentation, portability appears as a carve out to the bondholders' change of control put option.

In all markets and products, the effect is that the debt 'ports' to the new owner leaving the capital structure and documents intact

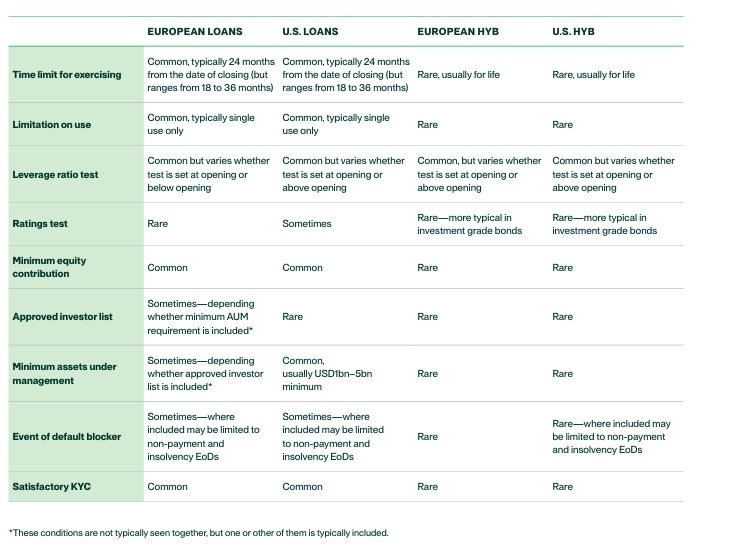

In all cases where portability is agreed in a leveraged deal, it is subject to some level of conditionality. While deal-specific variations exist, the most common conditions are generally drawn from the list below with leveraged loans including more conditions than high yield bonds:

- Leverage ratio test -Time limit -Single use limitation

- New investor controls

- Minimum equity requirement

- No event of default

- KYC on the new investor

HOW DO CONDITIONS DIFFER ACROSS LEVERAGED MARKETS AND PRODUCTS?

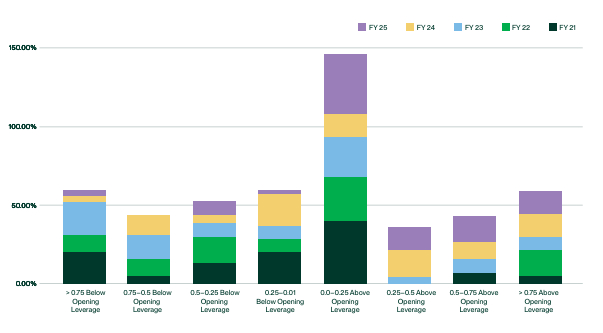

High yield bonds in both Europe and the U.S. tend to feature a sole condition— a leverage ratio test (or rarely a ratings test, although this is more common in the investment grade context). In both markets, portability is typically available as long as the high yield bonds are outstanding. According to 9fin, the ratio test in 2025 was increasingly set at or above opening leverage, meaning that day one availability of the feature was much more common.3

PORTABILITY HOVERS JUST ABOVE OPENING LEVERAGE

Leverage-based portability relative to opening leverage in sponsored deals (%)

Source: 9fin—FY 25 European High Yield Bonds Covenant Trends Report

In contrast, European and U.S. broadly syndicated loans impose more conditions:

- A ratio test is common in both markets, though isn't universal. Formulations vary, requiring leverage either at or immediately following the change of control, to be either no worse than opening level, or at or below minimum assets under management requirement. Whilst this approach is also seen in Europe, in some cases here the control will instead be an agreed list of potential new investors. FY 23 0.5–0.75 Above Opening Leverage FY 22 > 0.75 Above Opening Leverage FY 21 the RCF is typically excluded as it is a relationship-based 'take and hold' product, and RCF providers are often more sensitive to the idea of portable debt. In the U.S. the RCF is not typically treated differently. a specified level.

- There is almost always a time limit for use—ranging from 18 to 36 months in both Europe and the U.S. 24 months has emerged as the most common position in both markets.

- There is usually a limitation to single use.

- Often the provision requires the maintenance of a minimum equity cushion by the new investor post-exercise of the portability.

- In many cases there will be some sort of control over the identity of the incoming investor. Most commonly in U.S. loans this is in the form of a

- There may be a requirement that no event of default is continuing at the time of the change of control. A materiality qualifier sometimes applies in both markets to limit the blocker to non-payment or insolvency event of defaults.

- Satisfactory KYC is typical. Some European transactions have sought to loosen this by providing that KYC is deemed satisfied if a lender fails to respond or make a KYC request within an agreed timeframe.

- In European loans, portability may be limited to particular tranches of debt, most commonly senior secured term loans. In these cases, Although private debt market terms are not reported to the same extent, conditions typically mirror those seen in the broadly syndicated loans markets. One notable variation is that sponsors are more likely to be asked to agree a specific list of potential transferees upfront rather than set agreed criteria, and there may be a longer list of deal specific conditions applied. The table in the appendix provides a comparison of the conditions typically seen across markets and products.

OTHER FORMS OF PORTABILITY

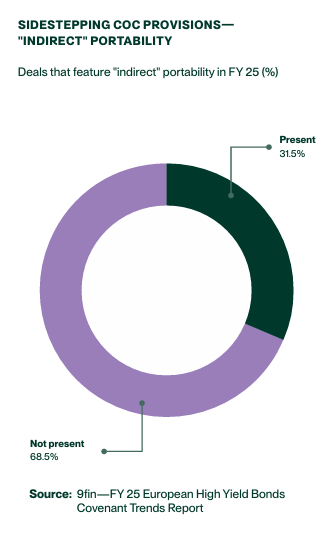

An even greater focus point for investors is the inclusion of 'indirect' portability. Some financing documents adopt expansive definitions of 'Sponsor' (or its equivalent) and related terms within the context of 'Permitted Holders' which are carved out of the change of control provisions. These definitions have a broader approach to which entities are permitted to hold equity in the borrower. In some cases, this can include investors in the original Sponsor's funds or the Sponsor's successors or assignees. The point to note is that investments by, or transfers to, these entities may not trigger a change of control, and they are not subject to any further conditions. There is no settled market position on how this type of portability is provided for. Recent market data from 9fin suggests that it was present in just under a third of 2025 European leveraged loan deals4.

WHAT NEXT?

We expect sponsors to continue to advocate for portability to preserve future exit flexibility. The high yield bond market has remained broadly consistent on this point over recent years and we don't expect that to change. However, in the loan market, the emphasis is likely to continue to be on balance: conditions robust enough to protect credit integrity for investors, yet practical enough for sponsors to rely on portability to exit if/when required

Footnotes

1 FY 25 European High Yield Bonds Covenant Trends Report (9fin) February 4, 2026

2 Octus 2025 European Leveraged Loans Wrap January 27, 2026

3 FY 25 European High Yield Bonds Covenant Trends Report (9fin) February 4, 2026

4 Pass the debt: comparative portability analysis across leveraged finance products and markets | March 2026

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.