Legislation: Pension Schemes Bill 2019-2020 will make no further progress. This Bill will be reintroduced by the new Parliament.

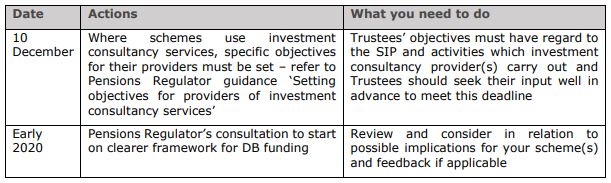

Pensions Regulator: regulatory guidance on tendering and setting objectives for investment service providers. Four guides have been issued for trustees on their duties to set objectives and tender for fiduciary management services and how investment consultancy services interact with schemes' governance models. Therefore by setting objectives for providers of investment consultancy services under the Investment Consultancy and Fiduciary Management Market Investigation Order 2019. Trustees will need to carry out competitive tendering for any agreement with fiduciary managers where 20% or more of the scheme assets are being delegated. See link

DWP: proposal to simplify annual benefit statements. The DWP's consultation (which closed on 20 December) considers ideas for standardising the structure, design and content of annual statements for members of DC workplace pension schemes. Three options for change have been proposed. The DWP also seeks views on two specific changes to the Disclosure Regulations. See consultation

Pensions Regulator: final master trusts' facts and figures. Only 37 of the 90 master trusts in operation in October 2018 have been granted authorisation (representing 16 million memberships and more than £36 billion in assets) and the Regulator believes that due to the authorisation process, many of the master trusts have improved e.g. by establishing more robust systems and processes and undertaking a greater level of financial due diligence than previously. See analysis

Revaluation Order 2019 published. The Order which comes into force on 1 January 2020, confirms the amount by which deferred pensions in pension schemes using the final salary revaluation method should be revalued for those reaching retirement during 2020.

NHS: exceptional action proposed to settle annual allowance tax issues. NHS England and NHS Improvement are introducing an interim measure for 2019/20 to ensure staff within the NHS Pension Scheme who are in active clinical roles are not left out of pocket due to annual allowance tax charges.

HMRC pension schemes newsletter: annual allowance charges' reminder. Administrators are asked to remind members who have exceeded their annual allowance and who do not have sufficient unused allowance to carry forward to cover the excess, that they must declare this even if their scheme pays the annual allowance charge under a "scheme pays" arrangement.

Pensions Regulator: improvement notice sent to LGPS fund following internal controls failings. The Regulator confirmed a range of improvements to the London Borough of Barnet Superannuation Fund (part of the Local Government Pension Scheme) following intervention in the scheme's administration. Key failings included over-reliance on third party service providers and the need for reconciliation of scheme's data. See statement

LGPS: opposite sex-civil partnerships amending regulations. Following legislation which provides for opposite-sex civil partnerships and in line with government policy that public sector pension schemes pay the same survivor benefits for opposite-sex civil partnerships as they would for opposite-sex marriages, the amending LGPS regulations make the required changes to achieve this, noting that the approach also complies with the equalisation principles in Barber.

Business Energy and Industrial Strategy Committee: recommendations to prevent future corporate collapses following inquiry into Thomas Cook. The Committee's recommendations included that changes should be made to executive pension contributions to create a fairer system and that executive bonus scheme arrangements must use measures that are pre-defined and not ambiguous and all future performance bonus arrangements should be required to include enforceable clawback provisions for a suitable period and covering all the elements of the bonus.

Pension Ombudsman: trustee acted properly in switching to CPI-based indexation. The member's complaint about the switch from RPI to CPI as the method for calculating increases to pensions in payment was dismissed, because unlike the Barnardo's case, the wording of the scheme's rules allowed for an alternative index to be used and also the trustee had taken all necessary and appropriate advice. See determination

Pensions Ombudsman: co-habiting partner not entitled to survivor's LGPS pension. Here, the member had left active service before the date required under the scheme's provisions to qualify for this benefit. The Ombudsman found that the death grant form provided sufficient information about the death grant and specifically, that it was only payable if the member died within five years of his pension coming into payment, which he did not. Therefore, the partner was not entitled to a death grant. In conclusion, the partner had suffered a loss of expectation, not financial loss.

Pensions Ombudsman: trustee's duties and disclosure. A complaint has been dismissed which related to an alleged breach of law where a deferred member contended that the scheme trustee's refusal to provide requested information relating to climate change risks were indeed maladministration. Here, the trustees confirmed that climate change had been identified as a major risk and provided that the scheme's recent actuarial valuation and statement of investment principles. The complaint was dismissed as the information request went far beyond what the trustee was required to provide at the time under the Occupational and Personal Pension Schemes (Disclosure of Information) Regulations 2013.

Pensions Ombudsman: scheme administration where a delayed transfer payment caused SSAS member additional rental costs in a property transaction. A complaint has been partly upheld in favour of the complainant who alleged that missing and incorrect information the scheme's provider had given to third parties had caused the failure of one property purchase delays and subsequently rental costs being incurred. The member wanted to transfer two personal pension schemes to his SSAS to use the funds to purchase a property for his business. By the time the provider replied, the purchase failed. Additionally, the scheme's bank account details included two sort codes and because the sort code provided to the administrator by the provider was incorrect, this caused serious distress and inconvenience in having to find a substantial amount of missing money, such so, he had incurred additional expenditure in another month's rent. The Ombudsman directed the provider pay £1,000 to the member in recognition to the serious distress and inconvenience he had suffered as well as the rental costs and interest.

Pension Ombudsman: it was incorrect to ask member to pay for medical reports in relation to ill-health early retirement application. The deferred LGPS's member's complaint that his application was delayed as a result of being asked to pay for reports was upheld. The Council were directed to consider backdating the members benefits by 5 years and to pay £1,000 compensation.

Pensions Ombudsman: incorrect benefit quotations. The deferred member's complaint that his scheme entitlement was lower than he had been promised was dismissed on the basis that a trustee is not bound to follow incorrect information and a member is only entitled to receive benefits based on correct information reflecting the rules. The member had received incorrect information in 1992 and 1994 but statements in 2004, 2001 and 2015 were correctly calculated and the member only complained in 2015 and should have been queried earlier.

High Court: pension increase rule rectified following discovery of drafting error. Rectification was granted on the basis that the situation arose due to a drafting error and it was noted that the scheme had always been administered on the pre-error basis.

High Court: settlement of British Airways pension increase litigation approved. The settlement agreed in April 2019, related to the trustee's decision to exercise its unilateral power of amendment to introduce a new trustee power to provide discretionary pension increases, and provided that the trustee would be entitled to award increases using the surplus in the scheme, including catch-up payments since 2013 and full RPI increases from 2021. In return, BA would be largely excused from further contributions. The Court held, applying the rationality test, that the settlement was one which a reasonable trustee could take.

Upcoming key dates:

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]