- within Environment topic(s)

- in Asia

Geopolitical pressures, technological disruption and shifting energy markets are reshaping what it means to transition to a more sustainable economy. This edition examines how three sectors, energy, defence and digital, are navigating the transition and reviews the regulatory and financial framework that will determine whether the transition succeeds.

The consistent message across recent editions of our ESG Circular is that disruptive times call for durable measures. Short-term reactive strategies rarely maximise opportunities and never more so than on sustainability, where striking the balance between immediate and longer-term priorities is fundamental. We hope this edition helps you find that balance.

This quarter in the round

The topics covered in this issue cover two key themes:

Theme 1: Sectors in transition

(chapters 1 - 4)

Theme 2: Frameworks for change

(chapters 5 - 7)

1. Energy security: independence, sustainability and the energy price crisis

The recent spike in wholesale electricity prices, triggered by conflict in the Middle East, thrust energy security to the top of the political agenda as the Government sought to mitigate the fallout from higher household energy bills. In late April 2026, the Government announced a significant package of measures designed to decouple electricity prices from volatile international gas prices which have been "driving the cost-of-living crisis even though much of the country's electricity supply comes from cheaper renewables and nuclear".

Energy independence

Under the current system, Britain can continue to build low-cost, homegrown renewable generation, yet still see its electricity prices dictated by global conflicts and supply disruptions due to the current pricing mechanism for the wholesale electricity market. The Government's measures seek to address that risk.

A boost for renewables?

From a sustainability perspective, volatile energy markets accelerate some transition dynamics (higher electricity prices boost the economics of renewables and efficiency investment), while complicating others (supply chain disruption and restricted access to finance for new projects), plus, more complex supply chains bring greater sustainability due diligence challenges.

Sustainable finance implications

The proposed measures were centred on the new Wholesale Contracts for Difference (WCfD) scheme and an increase in the Electricity Generator Levy (EGL) from 45% to 55%, an approach which has attracted mixed reviews. While the WCfD is framed as a voluntary, consumer-friendly measure, the simultaneous EGL increase creates a clear fiscal incentive for legacy generators to enter fixed-price contracts. And coming hard on the heels of the controversial RPI-to-CPI indexation change, the cumulative impact on legacy renewable assets is significant, with implications for valuations, financing structures and investor confidence.

Energy Independence Bill

A new Energy Independence Bill was announced in the King's Speech in May. Little has been said by Government on what it will include, but we anticipate: (i) powers to help accelerate renewable projects through planning processes; (ii) wider energy regulatory simplification, to allow e.g. hydrogen grids and smart technology to be deployed more easily; (iii) a properly legislated position, rather than ministerial announcements, on new oil and gas licences in the North Sea; and (iv) consumer-focused reforms aimed at reducing bills, particularly for the most vulnerable.

It remains to be seen whether it will introduce broader, more radical measures, such as de-coupling renewable energy pricing from gas. If the Bill provides much-needed clarity on the regulatory direction of travel, this will help crystallise opportunities to invest in the transition.

The interplay between energy pricing reforms and transition finance frameworks is explored further in sections 5 and 6 below.

Deep Dive

Breaking the link: Government moves to decouple gas and electricity prices

The Energy Independence Bill: Promise, Politics and the Price of Security

2. Responsible investment in defence

The question of how defence sits within an ESG investment framework has moved to the mainstream over the past 18 months. The EU's Defence Readiness Omnibus, published last year, represented a pivotal shift in Europe's approach - seeking to streamline regulatory barriers to defence investment while providing clarity on how the EU's sustainable finance frameworks interact with the sector.

The Commission's position is clear: there is no sustainability without security. In the UK, the FCA's view is that nothing in its rules, including those relating to sustainability labels under the SDR, prevents investment in or financing for defence companies.

Classification challenges

For asset managers, in practice, navigating the apparent conflict in regulatory obligations remains complex. The SFDR's requirements for "sustainable investments", especially the "do no significant harm" test and the need to address human rights due diligence in the context of investments, require careful analysis when applied to defence-related holdings. The Commission's suggestion that compliance with export licensing rules is sufficient to satisfy the human rights due diligence requirements has been questioned, not least by the UN Working Group on Business and Human Rights, which has argued that companies should conduct independent human rights due diligence "in all cases, regardless of export licence decisions by States".

Fund managers considering defence investments for Article 9 or Article 8+ funds will need robust, well-documented processes and should treat the Commission's guidance as a helpful starting point rather than a complete answer.

Separately, the amendment to the Climate Benchmarks Regulation, narrowing the exclusion for investments in "controversial weapons" to "prohibited weapons" provides additional clarity for funds with relevant ESG-related terms in their names.

These classification challenges apply equally to investments in other sectors, including opportunities arising from the energy transition, digital infrastructure and industrial transformation, discussed in sections 1, 3 and 4.

3. ESG in the Digital Economy: what AI means for environmental and social transition

The societal implications of AI for employment, for access to information, and as regards the concentration of economic power are a key ESG issue. From an environmental perspective, data centres are notoriously power- and water-intensive, and generate significant heat and noise, but as we explored in our previous Circular, the picture is more nuanced than it first appears.

On the regulatory front, once largely unregulated beyond their constituent parts (e.g. the building, the servers), data centres are now recognised as critical national infrastructure on both sides of the Channel, bringing with them a rapidly expanding web of regulatory obligations. The UK's Cyber Security and Resilience Bill now brings data centres with a rated IT load of 1MW or more within scope of the cybersecurity regime. The EU's Environmental Omnibus has proposed streamlining of Environmental Impact Assessment procedures for data centre projects.

While EU transparency and reporting rules and the expected efficiency ratings scheme might at first appear to seek to stifle investment in data centres, they could also provide an opportunity for differentiation in the face of discerning procurement teams with an eye to climate targets.

The advent of AI and the digitisation of economies also bring huge opportunities for businesses looking to make the transition, and investors looking for returns from it, but a step-change in the exploitation of data will be key. For the transition, flexible markets will need to make continuous micro-second micro-adjustments in connecting systems of intermittent renewable generation, variable storage capacity, and moveable energy demand. On the circular economy, digital product passports (discussed further below) and expectations around the recovery of materials will require more sophisticated and data-driven sustainability disclosures and decision making, at significant scale. Both will rely on AI and digitisation to achieve sustainable ends.

Deep Dive

Too Big to Ignore: Regulating the Data Centre Boom

Travers Smith's Alternative Insights: Governing the huge potential of AI

Balancing innovation and sustainability: The UK’s AI Growth Lab proposal - edie

4. Environmental product regulation: the EU's circular economy agenda

Digital Product Passports

Digital Product Passports under the Ecodesign for Sustainable Products Regulation (ESPR) are moving from concept to reality. This will drive new levels of transparency over information such as the origin of materials, environmental impact and disposal requirements. Businesses will also be required to disclose the presence in products of substances of very high concern.

PFAS regulation

Businesses in the consumer goods, fashion and industrial sectors are advised to review their exposure to PFAS regulation. The EU is working towards a landmark universal restriction on the whole group of PFAS substances, with France having already introduced a prohibition on intentionally added PFAS in some products from January 2026. In the UK, the Government's "PFAS Plan" published in February 2026 provides the first strategic framework for reducing PFAS harms, though critics claim it does not go far enough (and indeed, essentially amounts to a 'plan to have a plan').

Carbon pricing

The EU's Carbon Border Adjustment Mechanism entered its definitive phase in January 2026. The Omnibus I changes significantly narrowed the scope of importers subject to the regime, exempting approximately 91% of importers while continuing to capture over 99% of relevant emissions. The UK-EU "reset" has opened the door to ETS linkage, which could ultimately lead to mutual CBAM exemption, although political sensitivities and the Swiss precedent suggest meaningful progress will be slow to materialise.

Deep Dive

Moving Parts: A Guide to the EU's Evolving Product Regulatory Landscape

Travers Smith's Sustainability Insights: EU product regulation

PFAS under the spotlight: regulatory and litigation trends for forever chemicals

5. Transition planning: what should you be doing now?

The UK Government's commitment to mandating climate transition plans for UK-regulated financial institutions and FTSE 100 companies remains on the table, but the final regime is still taking shape.

For listed companies, the FCA's latest proposal on UK Sustainability Reporting Standards includes a "comply or explain" requirement to disclose whether they have a climate transition plan and if not, why not. This falls short of the Government's manifesto commitment on mandating the adoption of transition plans, but the FCA has left the door open for further requirements as Government policy develops.

For investors, the picture is also evolving. Many UK pension schemes have already adopted voluntary net zero targets and are actively using tools such as the Science- Based Targets initiative and the Transition Pathway Initiative to monitor their portfolios. This focus on transition risks is supported by the Government's statutory guidance on how trustees of large occupational pension schemes should consider climate change risks.

The FCA is currently consulting on replacing its current climate change reporting requirements with fewer, more targeted and more outcomes-based rules for FCA-regulated asset managers and investors. The aim is to ensure that retail and institutional investors get the right information based on their specific needs, while giving firms more flexibility in how they communicate with them. This could lead to companies facing more bespoke requests for information on transition risks, tailored to the specific priorities of their investors.

As more companies face mandatory reporting under the FCA's new sustainability reporting framework (expected from January 2027 for listed companies), the quality and credibility of transition plan disclosures will also face scrutiny from investors who may themselves be subject to these requirements.

Deep Dive

Ready, set, report: the FCA fires the starting gun on UK sustainability reporting

Travers Smith's Sustainability Insights: Reporting requirements still shifting

Travers Smith's Sustainability Insights: The UK's cautious roll out

UK formally adopts ISSB sustainability standards

6. Transition finance: bridging the funding gap

Based on FCA findings from the Transition Finance Pilot

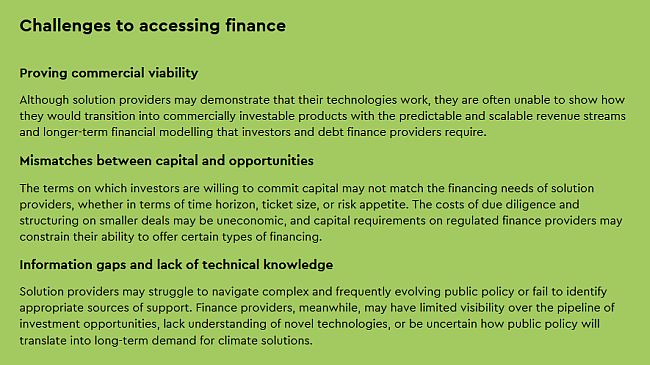

How easy is it to match UK climate solution providers with appropriate financing? That was the question the UK Financial Conduct Authority posed in its Transition Finance Pilot exercise in July 2025. The results, published in May 2026, make for sober reading: it appears it is far from straightforward.

The FCA notes that investments amounting to an estimated £26 billion would be required each year to reach the UK's 2050 net zero target, and that climate solution providers are growing on average three times faster than the wider economy. Despite the UK's status as a leading financial services hub with deep pools of capital, and the seemingly attractive growth prospects of target businesses, the FCA notes that serious challenges remain to accessing appropriate finance.

How should these barriers be addressed? The FCA has ruled out further changes to its own rules. Instead, its key recommendations are to encourage greater data sharing in the market, to encourage climate solution providers to engage more proactively with government initiatives and public finance opportunities, and for all market participants to leverage participation in wider networks.

There are also wider policy initiatives at play. Seventeen of the largest UK defined contribution pension providers signed the Mansion House Accord in May 2025, committing to deploy more patient capital into UK private markets which could support climate solutions investments alongside other sectors. Reforms to the British Business Bank and National Wealth Fund may provide more public finance for development-stage climate technologies that are typically shunned by private investors. And the Government's commitment to developing clearer sectoral transition plans aims to provide greater stability and long-term demand signals.

7. SFDR 2.0: call to action

Now is the time to engage in the legislative process for SFDR 2.0, through industry associations, direct responses to consultations, and dialogue with national regulators. The framework that emerges will shape sustainable investment disclosure for the next decade. For private market firms, the proposals as they stand remain inadequate. The framework continues to be designed around liquid assets that can be traded and rebalanced on short timescales, not the long-dated, illiquid investments that characterise private equity, infrastructure and private credit.

The European Commission's long-awaited proposal for a revised Sustainable Finance Disclosure Regulation landed in November 2025, and the direction of travel is becoming clearer, even if much of the detail remains unresolved.

The proposal would replace the existing (unlabelled) Article 8 and Article 9 classification system with three formal product categories: "Transition", "Sustainable" and "ESG Basics". Uncategorised products would face strict limits on what they can say about sustainability in investor communications, a provision that could effectively bake greenhushing into law for private market managers.

Member states are divided on whether active engagement with portfolio companies should qualify for the Transition category. This is a question of fundamental importance for private equity and infrastructure managers. Most Member States oppose grandfathering provisions, which would force costly repapering exercises for funds raised under SFDR 1.0. And the "ESG Basics" label has drawn criticism as politically awkward and commercially problematic.

There are some positive signals. Sweden has repeatedly warned that the investment approaches in the proposal suit listed equities but need adjustment for unlisted assets, and there are calls to extend transition periods and to allow voluntary ESG disclosures by non-categorised products. The window for influence is narrowing: the rules are expected to take effect no earlier than late 2027, but the legislative process is now well underway.

Deep Dive

Travers Smith's Sustainability Insights: Reporting requirements still shifting

Travers Smith's Sustainability Insights: Six fixes for SFDR 2.0

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]