Can you reframe your approach to sustainability disclosure and leverage the EU CSRD as a means for longer-term commercial advantage?

The Corporate Sustainability Reporting Directive (CSRD) aims to enhance the consistency, comparability, relevance and reliability of your sustainability reporting. However, you don't need to see CSRD as a purely regulatory imperative. Your organization could use CSRD requirements as a strategic tool to unlock long-term business success through sustainability.

If you're required to meet CSRD (see here for details on which organizations are impacted), adopting a more strategic approach could deliver significant competitive edge. While both reporting-led and strategy-led approaches to CSRD require collaboration across business functions, choosing a strategic approach need not involve any greater time commitment or financial costs compared to a reporting-led stance.

This insight, based on a webinar that also included facilities services business OCS's experiences of responding to CSRD, examines:

- Understanding the impact of CSRD

- Key principles of double materiality under CSRD

- Strategic and competitive advantage from CSRD

- Next steps on responding to CSRD

Understanding the impact of CSRD

The Corporate Sustainability Reporting Directive extends to large undertakings and listed companies, including third-country (non-EU) undertakings with significant EU revenues. If your organization has an annual turnover of more €150 million in the EU, or meets two out of three requirements – €40 million in net operating profit, €20 million in assets, 250 or more employees – you could be required to comply with CSRD.

Understanding and implementing double materiality is crucial to not only comply with the CSRD but also to enhance your strategic decision-making and stakeholder communication.

It mandates a comprehensive framework that requires you to report on a wide array of sustainability matters, which cover environmental, social and governance (ESG) factors. It introduces 12 European Sustainability Reporting Standards (ESRS) that apply to all sectors and lists disclosure requirements on potentially hundreds of data points. The table below illustrates the disclosures across the 12 ESRS, breaking it down into required and optional requirements.

The 12 European Sustainability Reporting Standards (ESRS).

| Cross-cutting standards | Topical standards – expanding on disclosure requirements mandated by ESRS 2 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Basic guiding principles | Mandatory disclosure requirements | Subject to materiality assessment | ||||||||||

| Environment | Social | Governance | ||||||||||

| ESRS 1 - General requirements | ESRS 2 - General disclosures | ESRS E1 - Climate change | ESRS E2 - Pollution | ESRS E3 - Water and marine resources | ESRS E4 -Biodiversity and ecosystems | ESRS E5 - Resource use and circular economy | ESRS S1 - Own workforce | ESRS S2 - Workers in the value chain | ESRS S3 - Affected communities | ESRS S4 - Consumers and end users | ESRS G1 - Business conduct | |

| Disclosure requirements (DR) | N/A | 16 | 12 | 7 | 6 | 8 | 7 | 19 | 7 | 7 | 7 | 8 |

| Data points (DP) | N/A | 99 | 64 | 38 | 18 | 61 | 35 | 106 | 57 | 55 | 55 | 25 |

| Sub-data points (SDP) | N/A | 89 | 111 | 5 | 32 | 67 | 38 | 90 | 45 | 44 | 41 | 41 |

| Required by other EU legislation | N/A | 8 | 69 | 2 | 6 | 6 | 2 | 17 | 10 | 7 | 7 | 4 |

| Required | N/A | 179 | 174 | 40 | 36 | 73 | 58 | 153 | 76 | 78 | 73 | 52 |

| Optional | N/A | 25 | 13 | 10 | 20 | 63 | 22 | 62 | 33 | 28 | 30 | 22 |

This table outlines the 12 European Sustainability Reporting Standards (ESRS) and the disclosure requirements for each.

The directive introduces a transformative approach to sustainability reporting, at the heart of which lies the concept of double materiality, which we explore in detail below. The double materiality concept helps you consider both your company's impact on the environment and society and the impact of sustainability issues on your company. This dual perspective takes a holistic view of a business' sustainability matters and specifically helps understand which of the disclosure requirements (outlined in the table above) should be reported on.

Understanding and implementing double materiality is crucial for you to not only comply with the CSRD but also to enhance your strategic decision-making and stakeholder communication.

Key principles of double materiality under CSRD

CSRD outlines several key principles that govern the application of double materiality in sustainability reporting. The following principles aim to ensure the reports you generate are not only comprehensive but also meaningful to the stakeholders reliant on them for decision-making:

- Materiality assessment CSRD mandates you

assess and report on both angles of ESG materiality, recognizing

your sustainability performance isn't only about how external

factors affect the business, but also about how the business itself

affects the world. Impact materiality, or 'inside-out'

materiality, shifts the focus to how your operations and practices

impact the environment, your stakeholders, such as your employees,

providers, clients and society. Impact materiality includes your

business's direct and indirect actions, looking beyond your

business operations to your value chain, key to including upstream

and downstream activities. These can contribute to impacts such as

environmental degradation, social inequality and economic

disruption. Financial materiality, often referred to as

'outside-in' materiality, involves identifying and

assessing how external environmental, social and economic factors

can affect your business. This perspective is more closely aligned

to traditional risk management, where the focus is on the risks and

opportunities posed by external factors to your financial health

and operational stability. CSRD mandates you assess and report

these impacts comprehensively, recognizing your sustainability

performance isn't only about how external factors affect the

business, but also about how the business itself affects the world.

This dual approach makes sure you consider the full spectrum of

your interactions with the environment and society, acknowledging

that these interactions can have significant consequences.

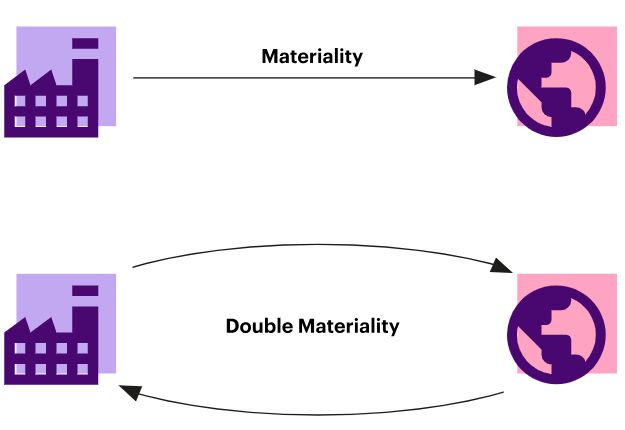

Materiality is illustrated as the impact the world has on your business. Double materiality is illustrated as the impact the world has on your business and the impact your business has on the world. The concepts of materiality and double materiality This graphic illustrates the concepts of materiality and double materiality. Materiality is illustrated as the impact the world has on your business. Double materiality is illustrated as both the impact the world has on your business and the impact your business has on the world. - Comprehensive disclosure: You aren't required to report on all possible disclosure requirements, but focus on those you identified as material through your double materiality assessment. This is specific to the 10 key Environment, Social and Governance Topical ESRSs identified in the CSRD. The exception is where the business notes ESRS E1-Climate Change as non-material it will have to separately explain why it has been deemed as non-material. This targeted approach is designed to ensure your reporting is relevant and focused on areas of significant impact, risk or opportunity (IROs).

- Accountability for all material impacts: You must account for all material IROs, regardless of whether you've taken or planned actions to address these impacts. This principle aims to ensure transparency and holds you accountable for your sustainability performance. It also encourages you to take proactive steps to mitigate potential negative impacts or enhance positive ones.

- Stakeholder inclusivity: CSRD mandates that the way you disclose information takes into account the diversity of stakeholders, so serves the needs of a broad audience, including investors, customers, employees and the wider community.

- Dynamic and ongoing process: The process of identifying material topics and reporting on them isn't static. You're expected to regularly review and update your materiality assessments and disclosures in response to evolving external conditions and internal strategies. This dynamic approach ensures sustainability reports remain relevant and reflect current conditions and challenges.

Strategic and competitive advantage from CSRD

By requiring detailed disclosures on a wide range of sustainability issues, CSRD pushes you to integrate these considerations into your strategic business model and core planning.

Engagement with internal business functions, initially during the double materiality assessment process and then during the disclosure processes, allows key strategic stakeholders to consider the risks, opportunities as a result of ESG factors.

CSRD disclosure requirements compel you to recognize and manage both the risks and opportunities associated with your sustainability practices. This means the strategic implications of the CSRD are profound, encouraging you to adopt a long-term view on sustainability and understanding the interconnectedness of this to your business strategy.

CSRD can also provide a series of robust indicators supporting your ESG stewardship. As the directive mandates comprehensive and granular disclosures that increase transparency, it could enhance trust among stakeholders, including investors, employees, customers and regulators. You can look to leverage this transparency to differentiate yourself in the marketplace, attract socially responsible investments, improve employee engagement and retention and enhance your corporate reputation.

A further key potential competitive advantage through CSRD compliance is improved financial performance.

A further key potential competitive advantage through CSRD compliance is improved financial performance. Transparently reporting and actively managing sustainability issues can lead to better risk management and open up new business opportunities, particularly in sectors where sustainability is a critical aspect of business operations. The phased implementation of CSRD meanwhile, allows you to prepare and adapt your processes gradually, which may help mitigate the impact of transition while still capitalizing on early compliance benefits.

Transparently reporting and actively managing sustainability issues can lead to better risk management and open up new business opportunities.

Next steps on responding to CSRD

While the CSRD presents numerous opportunities, it also poses challenges, in particular around data management and reporting, which you'll need to overcome.

CSRD requires you to report on a wide array of indicators and targets across environmental, social and governance factors in your different countries of operation, meaning you may need to develop more sophisticated systems for data collection, verification and management. This shift may entail significant initial costs and ongoing operational challenges.

The starting point of the analysis to help streamline the process is however the double materiality assessment which specifically helps identify the sustainability matters and subsequently the data points the business must report or could report under. Data associated with these requirements then must be collected, verified and managed regularly by stakeholders across the business.

The comprehensive nature of CSRD disclosures will also mean harmonizing your existing reporting processes to accommodate the new standards. This can involve extensive internal training, developing new tools and potentially restructuring teams.

Despite these challenges, there are wide-ranging strategic benefits of robust sustainability reporting. Advantages include an enhanced understanding of the business, bringing together different ESG initiatives in a streamlined manner and improved transparency that could enable improved market positioning, improved stakeholder relations and increased access to capital. These benefits indicate incentives for you to overcome these hurdles and embrace the strategic possibilities the CSRD represents.

There are wide-ranging strategic benefits of robust sustainability reporting. These benefits indicate incentives to overcome these hurdles and embrace the strategic possibilities CSRD represents.

For a smarter way to capitalize on the opportunities driven by climate, social and governance sustainability regulations, get in touch with our industry specialists.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.