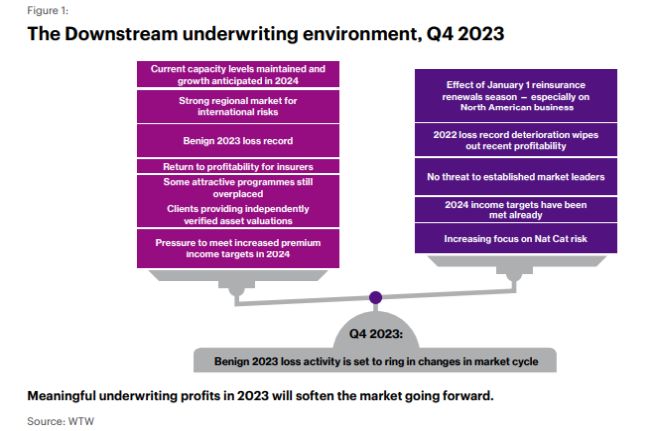

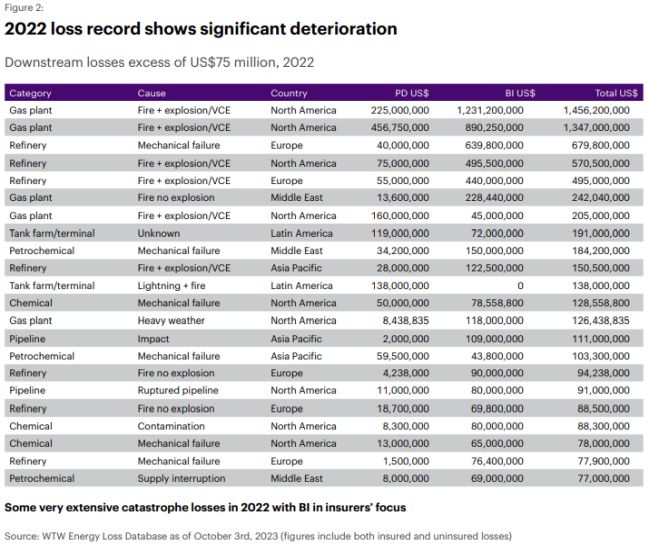

Significant deterioration of 2022 loss figures but there is light on the horizon

As reported in our April Energy Market Review, in 2021 and 2022, we saw major losses in the market, mainly in oil and gas but also in the chemical and midstream space. This ultimately affected both the downstream market and those upstream insurers who write midstream risks. Over the course of this year, 2022 loss reserves have deteriorated significantly and our database now records in excess of US$8 billion in losses for 2022. This deterioration is primarily due to the reduced or delayed access to sites for loss adjustors, either due to a knock-on effect of COVID-19 or because local authorities shut down sites immediately following a loss. As a result, loss adjustors cannot access sites to fully quantify losses until after the location is released by local authorities, which is causing meaningful delays in loss quantification and consequently less accuracy in insurer's initial reserves. This has been a key factor in the increase in reserves, particularly for the North American losses shown overleaf.

But why were losses so much more prevalent in 2021 and 2022? COVID-19 and the resulting low oil price environment have certainly led to fewer fully trained and experienced personnel on site. When this is combined with the excellent refining margins in 2021 and 2022, which have led clients to push out turnarounds and run assets at full capacity, it is clear why a greater incidence of loss events has emerged in these years.

Over the course of this year, 2022 loss reserves have deteriorated significantly and our database now records in excess of US$8 billion in losses for 2022.

In 2023 some green shoots are appearing. So far there have only been two major losses in the downstream market as well as some smaller attritional losses. The total loss record for 2023 stands at just over US$1.8 billion so far and we expect reserves for the largest of these losses to reduce, further improving insurers' position. If loss trends continue to be this benign for the remainder of 2023, we expect a very profitable year for downstream underwriters, which we believe will create a softer pricing environment going forward.

Increased capacity expected for 2024

Capacity levels have been generally stable throughout 2023, with some slight increases from less mature insurers who are now more comfortable to deploy slightly larger line sizes. Looking forward to 2024, we already know of some new entrants coming into the market and we expect a number of existing insurers to push for incremental capacity increases during their reinsurance treaty renewals, on the back of strong and profitable underwriting results for 2023. MGAs are also becoming more popular, further helping to increase capacity, and that should create more competition going forward, which is of course good news for buyers.

Regional capacity still plays a key role and in the Middle East in particular, there continues to be plentiful capacity and strong appetite for local business. This local market is buoyant, fuelled by significant levels of construction in both the downstream and upstream sectors.

Elsewhere in the world, we are seeing some local capacity being brought back into London in a move to "deregionalise" and we will continue to monitor whether this recentralising of underwriting authority is a trend that will gather momentum with other (re)insurers across the Downstream Energy market.

The market is still fragmented in their ESG positions, with some of the European insurers taking the strongest stances and we will continue to monitor how insurers' evolving ESG positions could affect future underwriting capacity.

To view the full article click here

Originally Published by Energy Market Review

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.