- with readers working within the Law Firm industries

- within Strategy, Privacy and International Law topic(s)

Co-authored by Professor Yarik Kryvoi

With assets under management worth over USD 10 trillion1 and about 7.8% of all listed equities worldwide2 under their control, Sovereign Wealth Funds ('SWFs') are among the world's most powerful economic actors. The 20 largest SWFs own 89% of these assets3. Despite their significance, the topic of SWFs and dispute resolution has not until now received the comprehensive consideration and analysis that its importance merits.

This joint report, co-authored* by Withers' public international law team and the British Institute of International Comparative Law, focuses on the transnational dimension of SWFs. It reviews different approaches to defining SWFs, their origins and cross-border operations.

This report fills this gap by examining the structure and dispute resolution matters related to Sovereign Wealth Funds, as well as related questions of sovereign immunity, enforcement, sanctions and future trends

The report explores transnational dispute resolution involving SWFs before both national courts and international courts and tribunals (including investment treaty and commercial arbitrations) and discusses strategic legal issues such as the fora in which disputes involving SWFs are settled, the subject matter of disputes involving SWFs and a host of related jurisdictional and merits issues.

The Report further considers regulatory and other issues related to the position of SWFs in a changing world, with sections dealing with questions related to the screening of SWF investments, sanctions affecting the operations of SWFs and the impact of business and human rights on SWF's operations. It also brings together institutional definitions of SWFs, lists the largest SWFs and examines their corporate structures. Finally, it provides detailed summaries of cases involving SWFs from key jurisdictions.

To read the report in full, please click here.

*The authors would like to thank the following lawyers from Withers for their invaluable assistance in preparing the Report: Dr Aniruddha Rajput, Ms Jovana Crnevic, Ms Clàudia Baró Huelmo, Ms Christina Liew, Mr Giacomo Gasparotti, Ms Martha Male and Ms Yousra Salem. The authors would also like to thank everyone who kindly reviewed drafts of the Report and provided feedback including in particular: Mr Diego Lopez, Dr Claudia Annacker and Dr Dini Sejko. A special thanks goes to Mr Diego Lopez and Global SWF also for supplying up-to-date and unpublished data and graphs on SWFs and their investment activities that are incorporated into this Report.

Insight from the report

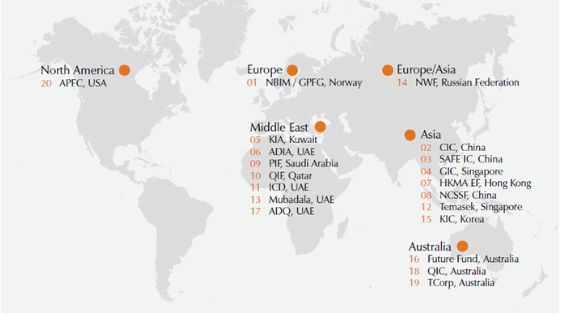

SWFs are located worldwide. The 20 largest SWFs (as at 22 August 2021) are spread across the Middle East, Asia, Europe, North America and Australia.

Although SWFs' investment geography is varied, it is notable that between 2015 and 2021 SWFs have invested predominantly in emerging markets4. In 2020, SWFs investments in emerging markets amounted to 66% of SWFs' investment by region5. By 2021, the trend decreased, but emerging markets still represent almost 49% of SWFs target regions to invest in6.

The importance of SWFs in the global economy has grown in the years following the financial crisis of 2008, and 'with many governments assuming . the role of guardians of substantial amounts of their countries' financial assets, effective wealth management has become an important public sector responsibility'7. The value of SWFs amplifies their impact on the world economy.

Since 2000, over 100 new SWFs have emerged. Data collected and analysed by Global SWF also shows that assets management under SWFs grew by 212% between 2008 and 2021.

The last 30 years have seen a significant growth in the number of new SWFs.

SWFs are powerful economic actors in the world economy.

SWFs engage in major cross-border acquisitions and corporate transactions in economic sectors such as real estate, infrastructure, TMT and healthcare. Disputes involving SWFs may include proceedings before national courts, commercial arbitrations, investment treaty arbitrations, and, to some extent, State-to-State disputes before international courts and tribunals.

State-to-State dispute resolution is a potentially underestimated avenue for a SWF to bring a claim against the host State of its investment.

Responsible business conduct and human rights responsibilities are particularly important for institutional investors such as SWFs.

SWFs by their nature act as long-term investors '...with the aim of leaving a legacy and safeguarding national wealth for future generations', and may therefore be expected to direct their investment policy towards more responsible firms which adopt policies aimed at sustainability8.

In recent years, the responsible business conduct and human rights responsibilities of business enterprises have become increasingly important.

Footnotes

1. Cf Global SWF, 'Top 100' https://globalswf.com/top-100 accessed 3 September 2021. The aggregate amount of assets under management of the SWFs listed in Global SWF's 'Top 100' rankings add up to around USD 10.02 trillion.

2. Unpublished data supplied by Global SWF for this Report.

3. This data can be extrapolated from Global SWF, 'Top 100' https://globalswf.com/top-100 accessed 3 September 2021. According to Global SWF's statistics, the 20 largest SWFs hold USD 9,053 worth of assets under management, which corresponds to around 89% of the total assets under management from SWFs.

4. Cf graph below 'SWFs Investments by Region'. The graph and underlying data have been supplied by Global SWF for this Report.

5. Ibid.

6. Ibid.

7. 'Sovereign Wealth Funds: Their Role and Significance – A Speech By John Lipsky, First Deputy Managing Director, International Monetary Fund' (3 September 2008) https://www.imf.org/en/News/Articles/2015/09/28/04/53/sp090308 accessed 3 September 2021. Cf also Christopher Beus, 'Sovereign wealth funds in the ICSID - a new approach to standing' (2014) 1 lndonesia Journal of lnternational and Comparative Law 543, 543.

8. Hao Liang and Luc Renneboofg, 'The Global Sustainability Footprint of Sovereign Wealth Funds' (December 2019) ECGI Working Paper Series in Finance, 8.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.