Small and medium businesses do not usually spend much time thinking about the quality of their reporting. After all, they have other priorities to tackle that could drastically alter the fate of their business. Besides, small and medium businesses are usually managed "by hand": the founders and top managers can make decisions independently and can easily monitor the implementation of their instructions.

Reporting in and of itself is viewed as less useful and of secondary value, as both employees and managers tend to associate the word "report" with accounting documents. However, as the company grows, so do the complexity of business processes and the quantity of decisions that need to be made. Trying to manage everything by hand creates a bottleneck. If the decision is made to sell part of the business to outside shareholders or to secure external investments (this does not necessarily imply significant revenue or enterprise value, considering that the average annual turnover of Russian companies acquired in 2015-2016 was USD 7-8 mln*, which is within the range for medium or even small businesses), then the priority of quality reporting increases significantly.

Managers and shareholders alike need quality reporting to track growth trends, to allow them to promptly react to problems, and to ensure a consistent understanding of the company's current situation and main strategic development goals. In our practice, we have worked with a private company during a gradual change of ownership. The new shareholder group was unsatisfied with the existing reporting format and required radical improvements. Meanwhile, the current owners felt that this was a secondary matter and wanted to focus on other issues that seemed more important to them. As part of the project, our consultants needed to develop metrics and algorithms that would make it possible to objectively evaluate the quality of the company's existing reporting and develop recommendations for necessary improvements.

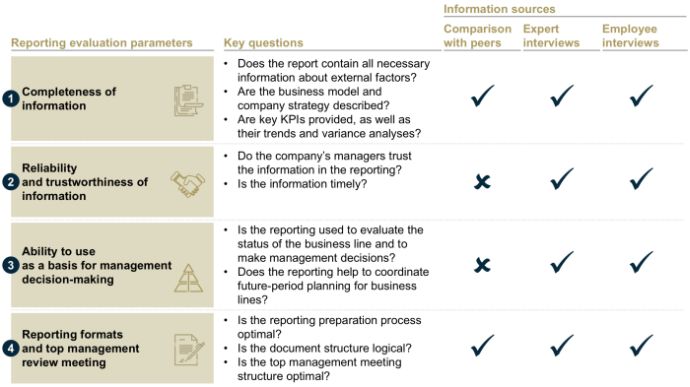

We first focused on formulating the parameters for evaluating the reporting and identified sources where the necessary information could be obtained. Figure 1 shows the parameters and information sources used.

Now, we will take a closer look at our approaches and the tasks we set when working with each information source.

Figure 1.

Evaluation parameters and information sources

- Comparing regular reporting

documents.

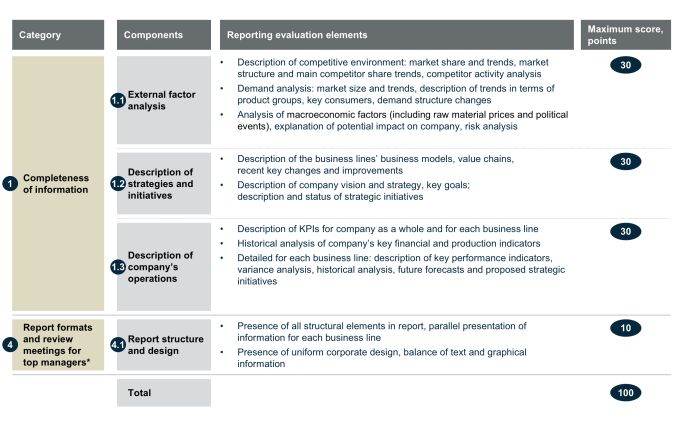

We collected and compared examples of the structures of both public and internal reports for a wide range of companies. In this analysis, our consultants were primarily interested in the completeness and quality of the information reflected compared with the client company's similar reports. Figure 2 shows our evaluation scale for regular reporting. - Expert

interviews.

Our consultants arranged to interview several top managers from a wide range of companies. During the interviews, we asked questions about the report preparation processes and how the reports were used (for example, by the board of directors, in management and employee motivation systems, and for distributing dividends among shareholders).

Figure 2.

Evaluation scale for regular reporting of companies in the food

industry

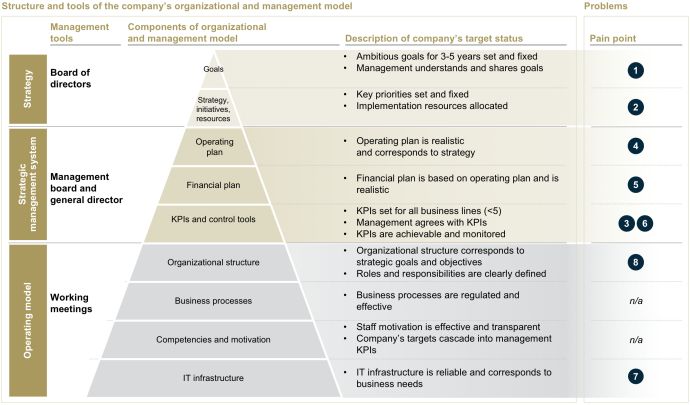

Figure 3.

Elements of the company's organizational and management

model

- Interviews with employees and

managers of the client company's business units.

During this process, our consultants conducted several dozen structured interviews inside the client company aimed at identifying "pain points" in its management models. Figure 3 shows general elements of the company's organizational and management model and their target state, which we discussed during the interviews.

We aggregated the results of all three parts of our work into a

single document:

1) quality evaluation for the client company's existing

reporting;

2) description of the risks associated with the client

company's existing organizational and management model;

3) recommended action plan to improve the organization's

management and decision-making process.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.