- within Energy and Natural Resources topic(s)

- in South America

- in South America

- within Compliance, Technology and Real Estate and Construction topic(s)

On Budget Day, the Dutch government published several legislative proposals and amendments related to energy and environment. These proposals are to be discussed and adopted by the Dutch parliament in the coming period but are still subject to changes and amendments. Below, we elaborate on the most relevant proposals.

General Policy

Lower budget for BESS and hydrogen

The budget within the Climate Fund for the development of battery energy storage systems and green hydrogen is lowered by EUR 1.2 billion.

Additional financing for national grid operator

An additional EUR 19.4 billion in financing is available for TenneT, the national transmission grid operator.

Future funding for nuclear

In addition to the two new nuclear power plants planned, the Government intends two additional new nuclear plants. EUR 250 million has been made available from the Climate Fund to both perform preparatory work for four new nuclear power plants as well as increase the life span of the current plant in Borselle. During 2025 it is envisaged to (i) tender the technology used, (ii) decide upon suitable locations and (iii) incorporate the project organization.

Energy Tax

Abolishment of the netting rule (salderingsregeling)

As of 1 January 2027, the netting rule in the Dutch energy tax will be abolished. This means that for both supplier invoicing as well as energy tax purposes, households may no longer net any self-generated renewable electricity with electricity supplied from the grid on an annual basis. Self-generated renewable electricity that is immediately consumed remains free of energy tax. The legislative proposal also stipulates that self-generating households and other non-market parties, should be paid a 'fair compensation' for the renewable electricity supplied by them to the grid.

Previously a gradual phase-out of the netting rule until 2030 was proposed, but the current Government coalition agreed upon a full and immediate abolishment as of 2027.

Changes to energy tax rates

As of 1 January 2025, the energy tax rates on the supply of natural gas up to 170,000 m3 will be gradually lowered, starting with EUR 2.8 cents / m3 in 2025 to ultimately 4.8 cents / m3 in 2030. Furthermore, the planned decrease of energy tax for electricity in the coming years is reversed.

Lower energy tax rate for hydrogen and precision of exemption

Currently, hydrogen used in a similar manner as natural gas

(e.g. as fuel) is taxed with energy tax at the same rate as natural

gas. As of 1 January 2026 a separate rate will be used for hydrogen

which will be equal to the energy tax rate in the last bracket for

electricity. This is currently at EUR 0.00188/kWh, but this will be

increased in the future. A Nm3 of hydrogen is assumed to

equal 9.77 kWh for this purpose.

An exemption applies for electricity used for the production of

hydrogen. This exemption is further specified to apply to the

demineralization and electrolysis of water, as well as the

purification and compression of the hydrogen produced.

Greenhouse horticulture sector

New tariff path for the greenhouse horticulture sector

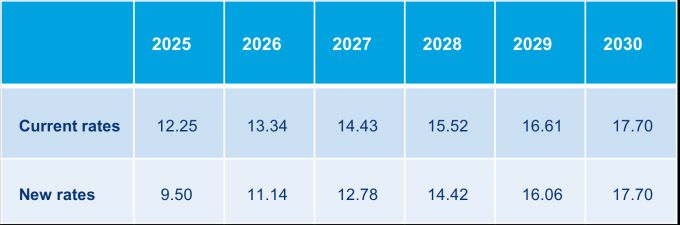

As of 1 January 2025, a carbon tax will be introduced for CO2 emissions by the greenhouse horticulture sector, similar to the current system for the industry. This coincides with the introduction of certain EU ETS obligations for the built environment. This proposal was already adopted last year, but it is proposed to make several amendments. The government proposes to adjust the tariff path to start at EUR 9.50 per ton of CO2 in 2025 (instead of EUR 12.25 per ton of CO2), which then increases to already adopted rate of EUR 17.70 per ton of CO2 in 2030.

The proposed carbon tax rates for this sector are as follows (in EUR / ton CO2):

Greenhouse gas installations of a greenhouse horticulture company or energy company for greenhouse horticulture are exempt from the minimum CO2 price for electricity generation. These greenhouse gas installations are part of the greenhouse horticulture sector and will be taxed through the CO2 levy for greenhouse horticulture.

The CO2 levy for greenhouse horticulture does not apply to greenhouse horticulture companies whose greenhouses have a cumulative area of less than 2,500 m² throughout the entire period, or in cases where the cultivation of crops in a greenhouse is solely for home-based businesses, educational purposes, research institutions, or allotment gardens. It is also important to note that if a greenhouse gas installation or an energy company for greenhouse horticulture does not fall under the CO2 levy for greenhouse horticulture, it will fall under the CO2 levy for industry or the minimum CO2 levy for electricity generation.

Energy companies for greenhouse horticulture

The requirement to be designated as an energy company for

greenhouse horticulture is specified. In the current Fiscal Climate

Measures Act for Greenhouse Horticulture, it is stipulated that

energy companies for greenhouse horticulture are also subject to

the CO2 levy for greenhouse horticulture. To be

designated as an energy company for greenhouse horticulture, the

requirement is that at least 75% of the heat generated with natural

gas is directly or indirectly transported to one or more greenhouse

horticulture companies. If this condition is met, it concerns a

company that has a strong connection with greenhouse horticulture

and therefore falls under the CO2 levy for greenhouse

horticulture.

Change to output exemption cogeneration

The output exemption for the own use of electricity produced by cogeneration installations will be limited to installations with a maximum electrical capacity of 20 MW as of 1 January 2025. This was already proposed last year, but initially the 20 MW limit referred to thermal capacity. This has been changed to electrical capacity.

Coal tax

Abolishment of certain coal tax exemptions

As of 1 January 2027, the coal tax exemptions for (i) the dual use of coal and (ii) the non-energy use of coal will be abolished. The current coal tax rate is EUR 18.10 per metric ton. The exemption for the use of coal for electricity generation remains.

This was already proposed during Budget Day last year, although as of 1 January 2028. Due to other elements of the legislative proposal it was not adopted at the time. The Government now proposes to still abolish the exemption, as it appears there is sufficient support in Parliament.

VAT

Introduction of VAT revision period for real estate related investment services

The Dutch government proposes to introduce new administrative obligations for all owners and users of real estate which procure real estate related investment services. Such services are characterized by their durable nature. This involves services to real estate, such as the renovation, extension, repair or replacement and maintenance of such property. Demolition work associated with renovation is also included. The government published a draft proposal to introduce a (five-year) VAT revision period for such services with an invoice amount of € 30,000 or higher. Although the draft proposal aims to address VAT-saving practices related to "short stay structures" with renovated residential property and property that is redeveloped from non-residential to residential property, the proposed revision period will affect all entrepreneurs owning or using real estate. A transition period is proposed, with the measure set to take effect on 1 January 2026.

This measure is announced in the 2025 Budget Plan, however, the details were already included in the draft end of year policy decree 2024 that was published for consultation on 5 September 2024. The definitive end of year policy decree 2024 is expected to be published at the end of December 2024. Earlier this year, a draft legislative proposal introducing the revision of VAT on investment services was published for consultation (we refer to our blog via this link).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.