In the first part of this article, we proposed a liquidity and payment support mechanism for the Nigeria Electricity Supply Industry (NESI), which should achieve the following objectives:

- Support NBET's payment obligations to Gencos under respective PPAs, which in turn, would enable Gencos meet their payment obligations to their Gas Suppliers under respective GSAs;

- Settle outstanding debts to Gencos and their Gas Suppliers;

- Cover anticipated revenue shortfalls which threaten the stability and sustainability of the NESI;

- Guarantee full payment to market participants (Gencos, Gas Suppliers and other market participants);

- Provide re-investible funds for Discos to fund their capital programs to reduce distribution losses and improve collection;

- Provide market confidence to investors in the NESI.

Under the proposed solution, NBET, as the Bulk Trader of electricity, will fully bear existing and future revenue shortfalls and payment risks to the NESI during the transitional electricity market (TEM) until such a time that Discos significantly improve their revenue collections and become more efficient in their operations.

The liquidity and payment support mechanism can be structured as a medium-term notes issuance program by NBET (NBET MTN Program), with an embedded partial risk guarantee from the CBN.

In this concluding part of the article, we put out our ideas on the structuring of the liquidity and payment support solution.

What Are MTNs?

Medium-term notes (MTNs) are debt instruments usually issued under a program that allows the issuer to offer bonds to investors from time to time without producing extensive legal documentation at the time of each issuance of notes, thus offering the issuer and investors more flexibility to the issuer and investor both in terms of structure and documentation.

While the bonds issued under a MTN Programme are typically called "notes", they are the same in substance and form as stand-alone bond issues, save that they are done under a set of master documents with standard terms and conditions, and thus allow the issuance of bonds quickly and easily. Due to its flexible nature, MTNs are an effective tool of asset-liability management for both the issuer and the investor. MTNs are most commonly issued as senior, unsecured debt of investment grade credit rated entities, and may have fixed or floating interest rates. They may be issued with flexible interest payments and have calls, puts and other options built into them. The flexibility of an MTN programme means that the pricing supplement or final terms of a particular series of notes will have the features that the Issuer wants based on prevailing market conditions at time of issue.

In a transitional electricity market, this flexibility will allow NBET to tailor the terms of the notes to the specific market realities while taking advantage of temporary market opportunities.

Although labeled as "medium-term", the tenor of a medium-term note (MTN) may be as long as 30 years, and the proposed NBET MTN program tenor can be established to cover the duration of the license period of NBET.

Description of The Proposed NBET Liquidity & Payment Solution

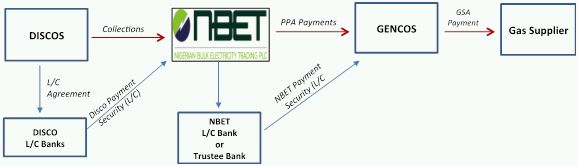

There is in place a payment security structure to support the NESI, which is shown in the diagram below.

Fig 1: The Existing NESI Payment Security Structure

In the event of revenue shortfalls by a Disco, NBET has the right to call on the Disco's payment security (which is in the form of a Standby Letter of Credit (SBLC) covering three months' of the Disco's payment obligations to NBET), to enable NBET meet its full payment obligations to Gencos. NBET has a back-to-back payment security with Gencos serving the same purpose (i.e. to cover any shortfall in payment by NBET to Gencos). However, under the current liquidity challenges, the reality is that, should NBET call on the Disco L/Cs, Discos will be unable to replenish the L/Cs once depleted, which may cause negative financial ripples along the entire Nigerian financial sector.

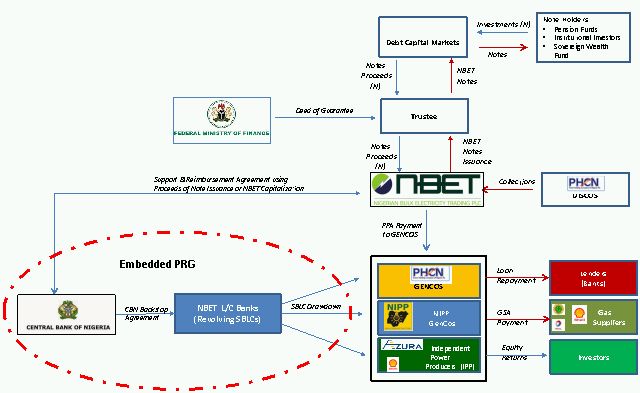

To enhance liquidity and assure a renewable payment cycle along the power sector value chain, we propose liquidity and payment support mechanism, which is depicted below:

Fig 2: The Proposed NBET Payment Support Program

The proposed mechanics of the NBET liquidity and payment support program is an improvement on the existing payment support program as it includes a liquidity upgrade and is as follows:

- NBET enters into a reimbursement and credit agreement (or similar agreement) with the CBN and approved NBET L/C Banks under which approved L/C Banks will undertake to make available a payment support instrument in the form of Standby Letters of Credit (SBLC) that may be drawn down by Gencos in the event that NBET is unable to make full capacity and energy payments to Gencos under the PPAs with Gencos, or there is a shortfall by NBET in capacity and energy payments to Gencos as a result of corresponding payment shortfall to NBET by Discos.

- The CBN will enter into a partial guarantee agreement (CBN PRG) with approved L/C Banks to backstop the repayment of any amounts drawn under the NBET SBLC in the event of NBET's failure to repay such amounts as a result of any risk specified under the guarantee. The CBN partial guarantee provides a secondary replenishment source for the SBLCs, thus further improving the viability and credit worthiness of the entire power sector. The CBN PRG is a critical piece of the liquidity solution and is key to providing continuous liquidity to the system and further credit enhancing NBET.

- To ensure NBET's ability to top up the SBLCs however, NBET will periodically issue notes under the NBET MTN program, which will be subscribed to by investors. The NBET MTN program provides a stable and sustainable liquidity mechanism for NBET to replenish the SBLCs when depleted and to fund any revenue shortfalls in the NESI during the TEM.

- To ensure investor confidence in the NBET MTN Programme, the notes will be guaranteed in full by the Federal Government of Nigeria to ensure that the Bonds are investment grade and can be subscribed to by Pension Funds and Institutional Investors. Regular note issuance by NBET provides market liquidity and the notes will be tradeable in the secondary markets.

- To strengthen investor confidence in the NESI, the program limit of the NBET MTN program should be sufficient to address existing debt to Gencos and potential future revenue shortfalls from Discos over a five-year to ten-year period or over the duration of the NBET license. The program limit can be extrapolated from current market realities, but with a positive outlook based on increase in efficiency as the NESI becomes more stable.

- The NBET notes will be repaid through a direct credit agreement between NBET and the Discos, wherein the shortfall amounts by Discos are converted to term loan obligations to Discos and amortized against the Discos' cash flows for the life of the NBET Notes.

- The conversion of Disco shortfall payments into term loan obligations of Discos, as well as enforcement of stiff penalties against core investors, such as dilution of their shareholding in Discos, arising from any inability to meet agreed collection levels and/or ATC&C targets, reduces the moral hazards on the part of the Discos who might see the NBET liquidity and payment solution as an encouragement to be inefficient in their operations and profligate in their capital spending.

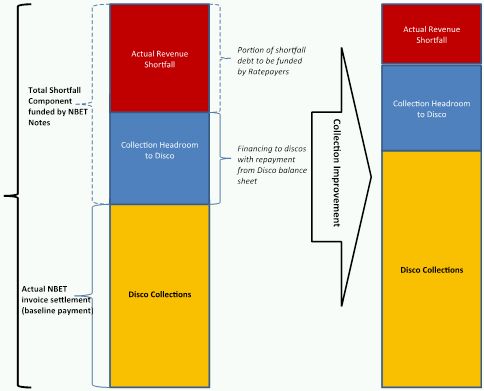

Financing the Discos – Agreeing Baseline Payment Levels to NBET

In our view, the Discos, being the direct consumer interface, are the weakest link in the entire power sector value chain. Thus any liquidity and payment solution that doesn't incorporate a solution to increase collection efficiency by Discos as well as make Discos more efficient in their operations may not succeed. The proposed NBET liquidity and payment solution will address this by setting a more realistic minimum baseline payment level to NBET by Discos. The baseline payment level is a percentage of total NBET energy invoice to Discos based on energy supplied to the Disco for that period.

Under TEM, Discos are expected to fully pay NBET for energy invoices. There are no minimum payment levels to NBET by Discos based on their present actual collection levels and settlement records. Where Discos use all their revenues to meet payment obligations to NBET, this leaves little or no room for Discos' to develop their infrastructure, reduce ATC& C losses, improve operational efficiency or even service loan obligations to Lenders. This is inimical to the growth of the power sector during the transitional phase of the market and creates a perpetual remittance shortfall cycle by Discos.

To improve operational and collection efficiency by Discos, we propose initial baseline payment levels to NBET for each Disco, which the Discos would commit to. The initial baseline payment level for a Disco should be set at a collection level below the actual revenue collections by that Disco. Setting the initial baseline payment levels below actual Disco collections creates financing for the Discos to finance their loss reduction programs. Any revenue collections achieved by Discos above the baseline payment level set is to the Discos' benefit and must be invested by Discos to improve losses and increase their collection efficiency for the following year.

The diagram below demonstrates the NBET baseline payment level concept.

The baseline payment levels are then adjusted upward periodically, to reflect improved efficiency and increased power supply from the grid. Alternatively, the baseline payment level could be increased annually in line with the annual ATC & C loss reduction targets which Discos will be required to submit to NBET under well worded information covenants in their term loan agreements with NBET.

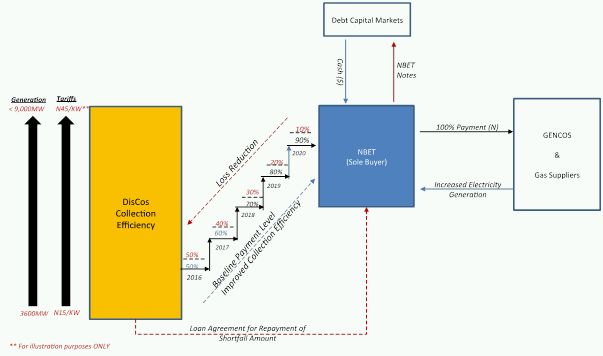

Example:

Assuming that at the start of the NBET MTN program, the baseline payment level for a Disco is set at 50% of total NBET electricity invoice, while its actual collections as a percentage of its NBET's invoice is 70%. NBET bears a 50% revenue shortfall, while the Disco retains 20% of its collections to finance its NERC approved capex program for that year. The 50% shortfall is funded by proceeds from the NBET MTN Programme. If under that Disco's loss reduction plan, it was supposed to have reduced ATC&C losses by 15% in the relevant billing year, the baseline payment level will be set at a new level of 65% of its NBET invoice for the next billing year. NBET then bears a 35% revenue shortfall in the next billing year, which is funded via the NBET MTN program. The baseline payment level is set at a new level each year till the Disco attains up to 100% payment levels.

The diagram below further illustrates the above example:

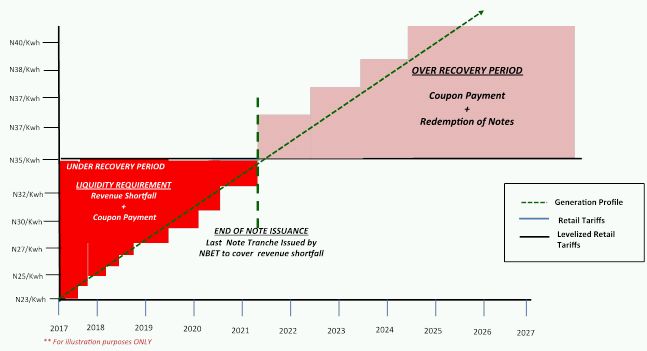

Repayment of the NBET Notes by Discos

The shortfall amount funded by the NBET notes will be structured as Loan obligations to Discos and repaid from a special portion of retail electricity tariff dedicated to the redemption of the Notes. We propose that the repayment of the Notes (principal and coupon payment) is sculpted to MYTO electricity tariffs to under-recover at earlier years (hence shortfall) and over – recover at later years. The diagram below illustrates the repayment of the NBET notes from tariff over-recovery at later years post – shortfall period.

Creating a special line item in retail electricity tariffs for the repayment of the NBET notes is not a new idea. In Ontario, Canada, the Ontario Electricity Financial Corporation charges a debt retirement charge, a line item on ratepayers' bills. The debt retirement charge is an amount above the energy charge to repay stranded debts arising from the privatization of Ontario Hydro. The repayment of the N213billion CBN Nigerian Electricity Market Stabilization Facility to the NESI is also structured as a line item in the electricity tariffs.

Benefits of Implementing the NBET Liquidity & Payment Solution

In summary, the proposed NBET Liquidity and Payment Support Mechanism delivers the following benefits:

- The NBET note issuance structure can be used to address the payment shortfall in the Power Sector to the Gencos in order for the Gencos to continue generating power and meeting their obligations to the Gas producers.

- The proposed structure will prevent payment default by Discos, which default may trigger defaults across the electricity value chain and cause financial distress in the NESI as is evident today. The collapse of the NESI will have a catastrophic effect on the banking sector, which is already exposed to the NESI by over US$4billion. The economic implications of a collapsed power sector can't be quantified.

- The payment support mechanism will bring about increased generation capacity both in the short term and long term, thus electricity supply will improve.

- It would prevent a rate shock due to rapid increase in electricity tariffs to support the revenue requirement of the sector (i.e cost reflective tariffs), without an incremental increase in electricity supply to customers. The recent 45% increase in electricity tariffs and the ensuing public uproar and negative after effects so far is a good case study.

- The lower baseline NBET remittance level for Discos is a sustainable way to provide financing to Discos to implement part of their loss reduction program.

- The proposed structure also provides liquidity for local banks to support the Power Sector.

- The structure provides firm payment assurances to gas producers, which would allow them reach Final Investment Decisions (FID) for new gas-to-power development, particularly FID for Non-Associated Gas (NAG) and building critical gas infrastructure, which would increase gas supply to the NESI. Gas-to-power investments require long lead times, thus making the investments today guarantees the availability and sustainability of gas supply to power plants in the long term.

- It would allow new generation projects from renewable energy sources (wind, solar, etc), hydroelectric projects and coal reach financial close quicker, leading to the attainment of the plan by the FG to achieve a 50:50 diversification of our energy mix by year 2020.

- It reduces or possibly eliminates the requirement for other payment support instruments like the World Bank Partial Risk Guarantees, MIGA guarantees, typically required by Lenders to project finance greenfield IPPs. It also would reduce the cost of project financing power projects.

- It provides stable and assured cash flows to the Transmission Company of Nigeria, thus making the TCN operationally viable to meet its obligations of operating the grid efficiently. This solution will enable TCN implement PPP arrangements with Investors to build new transmission lines badly needed to wheel power efficiently.

Overall, developing a sustainable liquidity solution for the power sector will have positive domino effect on the quality of lives of Nigerians as a whole: there will be greater investor confidence in the power sector, a more stable power supply, increased output and efficiency in manufacturing towards a more speedy industrialization of Nigeria, less reliance on foreign goods and products, a lessening of the pressure on Nigerian foreign reserves, increase in productivity across the entire economic spectrum, and a better life for Nigerians as a whole.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.