Or, more accurately, if you build part of it they will come to Oamaru. That is how the government hopes the private sector and local authorities will respond to its draft broadband investment initiative released last week for comment.1

The proposal is to set up a Crown Fibre Investment Company (CFIC) to invest $1.5 billion in up to 25 local fibre companies (LFCs) that will deploy and provide access to fibre optic network infrastructure to the 75% of New Zealand's population located in our 25 largest cities and towns. Oamaru is 25th on the list.

This fibre-to-the-home (FTTH) initiative is intended to achieve broadband speeds of up to 100 megabits per second (Mbps), over the next 10 years. This compares to the 10-20 Mbps that will be achieved for 80% of the population under Telecom's current fibre-to-the-node rollout which is scheduled for completion by 2011.

The Proposal

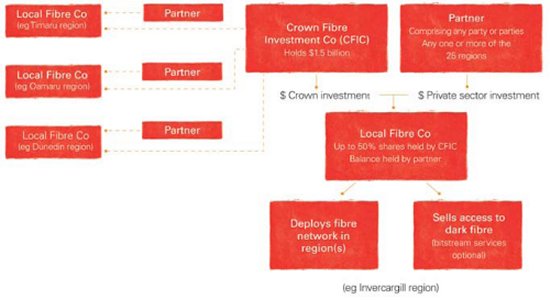

The CFIC will invest alongside private sector co investors in the LFCs. The paper says the phrase 'private sector' is used loosely to refer to any non central government partner, thereby opening the way for local government participation.

Of the $1.5 billion, $150 million is already earmarked to be spent on making schools 'broadband ready'. This leaves $1.35 billion for a broader FTTH network. The government is looking to the private sector to provide the remainder of what the paper estimates will be a total cost of $3 to $6 billion to roll out a FTTH network to 75% of the population. In return, the private sector partner will secure shares in the LFCs and the government's acknowledgement that its own shareholdings in the LFCs may be 'concessionary' and in particular subject to a lower rate of return than the shareholdings of its LFC partners, at least for the initial period (which the paper defines as 'for example up to 10 years'). Partners are expected to offer both investment and the commercial and technical ability to deploy and operate the fibre network.

The proposed structure is:

The proposal paper expressly states that there is to be no 'regulatory holiday' for the LFCs. In other words there is to be no undertaking from the government that, in return for investment, the LFCs will not be made subject to regulation under the Telecommunications Act 2001 or the Commerce Act 1986. This means that, while pricing will initially be determined commercially, there is scope under either of those Acts for the Commerce Commission to make recommendations to the relevant Minister that prices be regulated.

However, the proposal also recommends that existing telcos with retail operations be ineligible to participate as partners in LFCs unless they either:

- fully divest themselves of their retail operations, or

- do not appoint the majority of the directors to the board of the relevant LFC and the chair of the LFC board is independent and agreed to by all shareholders.

The intention of this is that any incentive for an LFC to engage in anti competitive behaviour by favouring its own retail operation would be eliminated.

What exactly this means for Telecom is not clear. On the one hand it has just undergone a hugely expensive and difficult operational separation whereby its retail, wholesale and fixed network divisions have been separated and structured in such a way as to ensure they behave as separate entities. On the other hand, those divisions are still part of the same legal entity and Telecom's retail division would not appear to meet the paper's test of being 'fully divested'. This has prompted media speculation that Telecom's network arm, Chorus, will be structurally separated from the rest of Telecom, leaving it free to control any LFCs in which it invests.

Who Gets What?

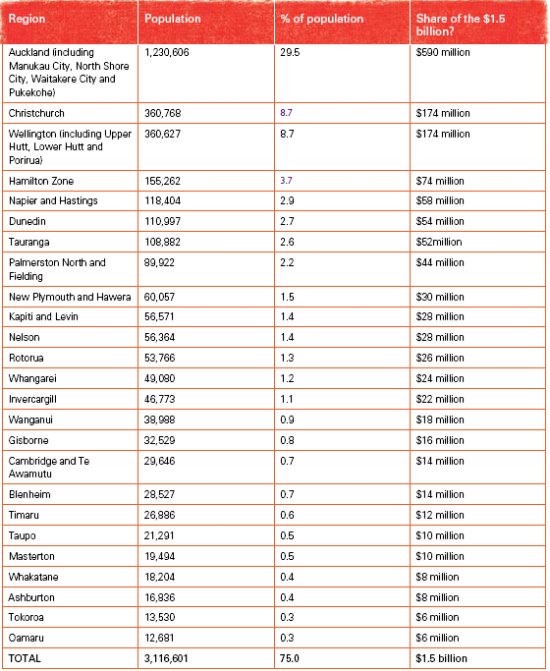

One of the key selection criteria that the CFIC is to apply when selecting proposals is achieving a roughly proportionate spread of the available government funds across regions. This means in relation to the 25 cities and towns referred to in the proposal an approximate distribution of the available funds would be as follows:

As noted above, of the $1.5 billion, $150 million is already earmarked for making schools broadband ready so that to secure the full level of funding indicated in the table, proposals will presumably have to assist the CFIC in meeting that objective.

Points Of Interest

Some points of interest are:

- The proposal leaves open the door for a single party to submit a bid covering a number of regions. At the extreme this means a single bid could cover all 25 regions and there could therefore be a single LFC to which the CFIC then provides funding.

- The proposed structure of the CFIC is as a Public Finance Act 1989 Schedule 4 entity (a current example of such an entity is the New Zealand Lottery Grants Board). The paper envisages the CFIC would have a secretariat of around 5 10 full time staff and would have operational costs in the order of $4 million per year which would come out of the $1.5 billion.

- The initial priorities under the proposal would be to make fibre available to priority users such as business, schools and health services plus green-fields developments. This is slated for the first six years of operation of the CFIC. The secondary goal is to make fibre available to 75% of the population within 10 years.

- The proposal envisages that LFCs would have company constitutions requiring them to operate in certain ways and to avoid certain activities. The proposal envisages a shareholder's agreement would be put in place between the CFIC and the LFC partner. Further, LFCs would be required to adhere to common technical and commercial standards. LFCs are to operate purely as fibre infrastructure carriers providing wholesale access to dark fibre but would have the option of providing other wholesale services such as bitstream services (bitstream services are suitable for wholesale customers with less of their own infrastructure).

- The proposal refers to the current fibre-to-the-node/ cabinetisation program being undertaken by Telecom's operationally separate network division, Chorus. This was part of the commitments made by Telecom in connection with its operational separation undertakings finalised in March 2008. The paper notes that Telecom may not have made that investment had it known of this new FTTH initiative. It refers also to the risk to Telecom that the value of its fibre-to-the-node/cabinetisation investment might be eroded as customers move to the proposed FTTH network. The paper says this risk is mitigated in that Telecom can compete to access the government's CFIC investment. It also notes that Telecom can seek a review of its operational separation undertakings.

- Areas outside the 75% coverage area in the proposal will, according to the paper, be addressed through the review of the Telecommunications Service Obligations Regime.

- Officials have been directed to report back to the relevant cabinet committee on whether a National Environmental Standard and/or legislative amendment is necessary to cover:

-

- fibre cable deployment on telephone and electricity poles

- access to local authority-owned passive infrastructure such as ducts

- microtrenching; and

- fibre optic cable 'drops' from the street-side zone into customer premises.

- The proposal does note that the local fibre companies may be new companies or could be based on existing companies where existing companies are suitable vehicles for fibre deployment.

What Will FTTH Deliver?

In terms of economic benefits from FTTH, the paper refers to independent estimates of improved productivity, global connectivity and capacity for innovation valued at between $2.4 billion and $4.4 billion a year. In answer to the critics who say that the benefits of a step change in broadband capacity are speculative, and that even the experts still can't say exactly what many homes and businesses could usefully do with up to 100 Mbps of extra bandwidth, the paper's response is in part 'if you build it they will come'. The paper notes that in the short term there could be significant productivity improvements for ICT dependent businesses but that for most residential users the applications available with FTTH as compared to the status quo are unlikely to be significantly different. However, the paper puts its faith in new applications being developed in the future and references the massive growth in applications over the last 10 to 15 years on the back of incremental increases in available bandwidth. The paper notes:

'...in 10 years' time it is likely we'll be talking about ultra fast broadband at speeds of 100 Mbps and there are very likely to be applications that will demand this bandwidth.'

Submissions on the proposal close at 5pm on 27 April 2009. The timetable after that proposes a report back to cabinet by the end of May, the appointment of the CFIC by mid June 2009 and thereafter indicative dates whereby an RFP would be released by the CFIC by mid August 2009, proposals due by mid October 2009, and the initial decisions made by the CFIC by January 2010.

Footnote

1. The proposal is available at www.med.govt.nz/upload/63958/Final-broadband-iniative-consultation-document.pdf

Phillips Fox has changed its name to DLA Phillips Fox because the firm entered into an exclusive alliance with DLA Piper, one of the largest legal services organisations in the world. We will retain our offices in every major commercial centre in Australia and New Zealand, with no operational change to your relationship with the firm. DLA Phillips Fox can now take your business one step further − by connecting you to a global network of legal experience, talent and knowledge.

This publication is intended as a first point of reference and should not be relied on as a substitute for professional advice. Specialist legal advice should always be sought in relation to any particular circumstances and no liability will be accepted for any losses incurred by those relying solely on this publication.