- within Corporate/Commercial Law, Government and Public Sector topic(s)

Background

The Crown Dependencies (Guernsey, Isle of Man and Jersey) will shortly be approving new legislation, presented to the three respective Parliaments, to introduce economic substance requirements, for companies incorporated, or resident for tax purposes, in each of these jurisdictions.

This legislation has been designed to meet the high level of commitment made by the Crown Dependencies, in November 2017, to address the EU Code of Conduct Group's concerns, that some companies tax resident in these Islands do not have sufficient 'substance' and benefit from preferential tax regimes.

- Once implemented, these changes are designed to place the Crown Dependencies on the EU white list of cooperative jurisdictions and will avoid any possibility of future sanctions.

It is worth noting that the EU have identified 47 jurisdictions, in total, all of which are having to address substance requirements urgently.

Crown Dependencies – Working Together

It is anticipated that the final substance based draft legislation will be submitted for consideration, by the appropriate Parliament within the Crown Dependency jurisdictions, in December 2018.

The Crown Dependency Governments have "worked in close collaboration together" in preparing the respective legislation and guidance notes, with the intention that these are as closely aligned as possible. Representatives from the relevant industry sectors have been involved in the preparation of the legislation for each Island, to ensure that it will work in practice, as well as it fully meeting EU requirements.

Summary: Crown Dependency – Economic Substance Requirements

In brief, Economic Substance Requirements, will be effective for accounting periods commencing on or after the 1st January 2019. Any Crown Dependency company that is considered resident in the jurisdiction for tax purposes and is undertaking relevant activities, will need to prove substance.

Specific 'relevant activities' are defined as:

- Banking;

- Insurance;

- Fund Management;

- Headquarters;

- Shipping [1];

- Pure equity holding companies [2];

- Distribution and service centre;

- Finance and leasing;

- 'High risk' intellectual property.

[1] Not including pleasure yachts

[2] This is a very narrowly defined activity and does not include most holding companies.

A company tax resident in one of the Crown Dependencies which undertakes one or more of these 'relevant activities' will have to prove the following:

- Directed and Managed

The company is directed and managed in the jurisdiction in relation to that activity:

- There must be meetings of the Board of Directors in the jurisdiction, at adequate frequency, given the level of decision making required;

- At these meetings, a majority of directors must be present in the jurisdiction;

- Strategic decisions of the company must be made at these Board Meetings and the minutes should reflect these decisions;

- All company records and minutes should be retained in the jurisdiction;

- Members of the Board should have the necessary knowledge and expertise to discharge the duties of the Board.

- Qualified Skilled Employees

The company has an adequate level of (qualified) employees in the jurisdiction, proportionate to the activities of the company.

- Adequate Expenditure

An adequate level of annual expenditure is incurred in the jurisdiction, proportionate to the activities of the company.

- Premises

The company has adequate physical offices and/or premises in the jurisdiction, from which to carry out the activities of the company.

- Core Income Generating Activities

It conducts its core income generating activity in the jurisdiction; these are defined in the legislation for each specific 'relevant activity'.

The additional information required from a company, to demonstrate that it meets the substance requirements, will form part of the company's annual tax return in the appropriate Island. Failure to file returns will generate a fine.

Enforcement

Enforcement of the economic substance requirements will consist of a formal hierarchy of sanctions for non-compliant companies, with increasing severity, up to a maximum fine of £100,000. Ultimately, for persistent non-compliance, an application would be made to strike off the company from the relevant Company Registry.

What Type of Companies Must Pay Particular Attention to Substance?

Companies that only have their registered office in or are incorporated outside (and controlled in), one of the Crown Dependencies must pay particular attention to these new rules.

How Can Dixcart Help?

Dixcart have been proactively encouraging clients to demonstrate real economic substance for several years. We have established extensive serviced office facilities (in excess of 20,000 square feet) in six locations around the world, including the Isle of Man and Guernsey.

Dixcart employ senior, professionally qualified staff, to support and direct international functions for its clients. These professionals are competent to take responsibility for different roles, as appropriate; finance director, non-executive director, industry specialist, etc.

Summary

Dixcart perceive this as an opportunity for clients to demonstrate true tax transparency and legitimacy. These measures also encourage real economic activity and job creation, in the Crown Dependency jurisdictions.

Additional Information

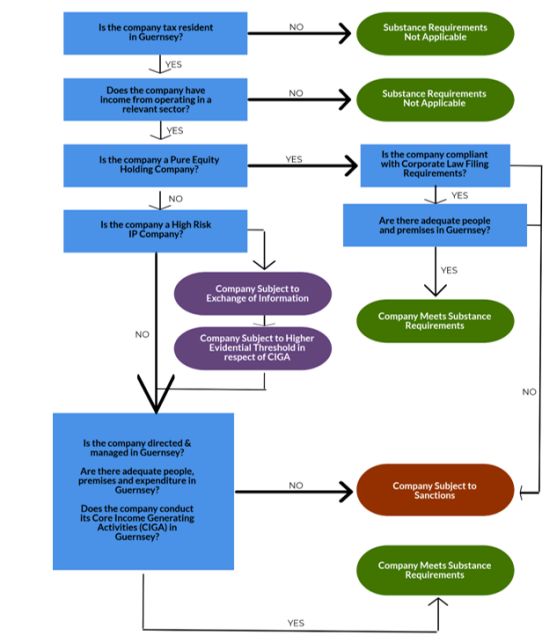

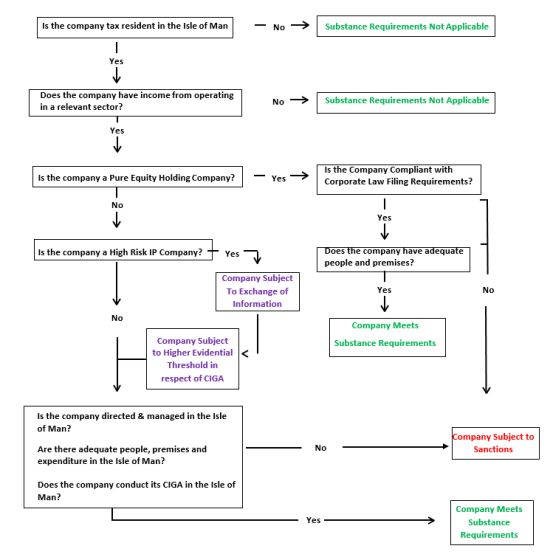

Two flow charts, one for Guernsey and one for the Isle of Man, are appended.

They detail the respective steps to consider and define when substance requirements must be met. Links to the relevant Government websites containing comprehensive details regarding the appropriate legislation for each jurisdiction are also featured.

Dixcart Trust Corporation Limited, Guernsey: Full Fiduciary Licence granted by the Guernsey Financial Services Commission. Guernsey registered company number: 6512.

Dixcart Management (IOM) Limited is licensed by the Isle of Man Financial Services Authority.

GUERNSEY SUBSTANCE REQUIREMENTS

8th November 2018

https://www.gov.gg/economicsubstance

ISLE OF MAN SUBSTANCE REQUIREMENTS

Release Date: 6 November 2018

Flowchart

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]