- within Immigration topic(s)

Headlines

|

In our latest European Securities Law Update and following the recent publication of the ESMA final report of technical advice issued on 3 April 2018 we provide a high-level synopsis of the recent Prospectus Regulation, its implementation in Ireland and its applicability as regards Irish SPVs operating in the debt capital markets ("DCM") space.

Timing and Implementation

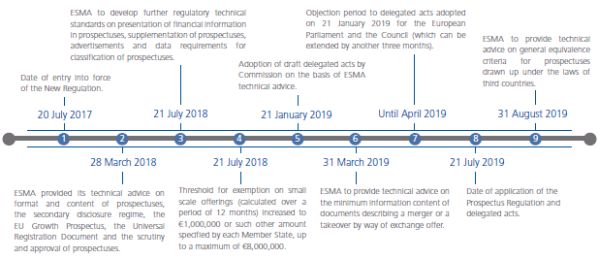

Regulation (EU) 2017/1129 (the "New Regulation") entered into force in Ireland on 20 July 2017. The New Regulation will take effect from 21 July 2019, save for a handful of specific provisions as outlined below. The New Regulation forms part of the EU's Capital Markets Union initiative which aims to ensure investor protection and market efficiency, while enhancing the internal market for capital.

The New Regulation will replace and repeal the existing Prospectus Directive regime and related measures (the "Old Regime"). The new rules are introduced by directly effective European regulation in order to eliminate regulatory arbitrage at Member State level and to ensure consistency and certainty of application.

Requirement to Publish a Prospectus

The triggers requiring publication of a prospectus remain unchanged, issuers must publish a prospectus in connection with:

- an offer of securities to the public (the "Public Offer Trigger"); or

- the admission to trading of securities on a regulated market in the EU (the "Trading Trigger").

Exemptions to Public Offer Trigger include:

|

Exemptions to Public Offer Trigger

The Old Regime provides for a number of exemptions from the 'public offer' trigger and these have been retained in the New Regulation (see adjacent summary).

The exclusion for small scale offerings has been retained but amended; under the Old Regime an issue of securities not otherwise subject to regulation where the total consideration in the EU is less than €5,000,000, calculated over a period of 12 months, fell outside of the remit of the Prospectus Directive. Under the New Regulation this threshold has been reduced to €1,000,000 with effect from 21 July 2018. Member States have discretion to increase this threshold to €8,000,000 however any offer which benefits from such discretion will not be allowed to passport under the passporting regime set out under the New Regulation and will be exempted from the requirement to publish a prospectus, rather than being excluded from the New Regulation altogether.

Exemptions to Trading Trigger

Some of the existing exemptions to the Trading Trigger have been revised. Of relevance in the DCM space is the extension of the exemption under the Old Regime whereby there is no requirement to publish a prospectus for the admission to trading of shares representing, over a period of 12 months, less than 10% of the number of shares of the same class already admitted to trading on the same regulated market.

From 20 July 2017 this 10% threshold has been increased to 20% and the exemption has been extended to the admission of securities i.e. now including bonds and debt (the "Fungible Tap Issue Exemption"). On its face this amendment should facilitate fungible tap issues of debt which come within the 20% threshold as issuers of such debt will not be required to publish a New Regulation compliant prospectus.

In practice however, debt securities issued by Irish SPVs are often listed and so such fungible securities will likely require the preparation of a listing document in any case. As such, this revision is not expected to significantly overhaul DCM market practice.

It should be noted however that the New Regulation helpfully allows for simplified disclosure relating to secondary issuances in a number of circumstances. This includes issuers whose securities have been admitted to trading on a regulated market continuously for at least the last 18 months and who issue securities fungible with existing securities which have been previously issued. Such simplified prospectus shall consist of a Summary (see below), a specific registration document and a specific securities note.

Retail Offers: Summary

The New Regulation has retained the requirement to include a Summary. While the New Regulation prescribes a uniform structure, issuers have discretion to include information in the Summary that they deem to be material and meaningful provided that such information is presented in a fair and balanced way. The Summary should not be a mere compilation of excerpts from the prospectus.

The New Regulation does not require inclusion of a Summary where the prospectus relates to the admission to trading on a regulated market of non-equity securities provided that (1) such securities are to be traded only on a regulated market, or a specific segment thereof, to which only qualified investors can have access for the purposes of trading in such securities; or (2) such securities have a denomination per unit of at least €100,000.

Subject to certain exceptions, the Summary shall be drawn up as a short document written in a concise manner and of a maximum length of seven sides of A4-sized paper when printed. The Summary shall comprise four sections: (1) an introduction; (2) key information on the issuer; (3) key information on the securities; and (4) key information on the offer of securities to the public and/or the admission to trading on a regulated market.

A brief description of the risk factors that the issuer considers most material must be included in the Summary but cannot exceed 15 risk factors in total. This restriction may prove challenging for issuers and, on its face, opens the door for increased prospectus liability, particularly in the case of complex and multi-faceted transactions. In this regard issuers can take comfort from the retention of provisions in the New Regulation which provide that no civil liability should be attached to any person solely on the basis of the Summary unless (1) it is misleading, inaccurate or inconsistent when read together with the other parts of the prospectus; or (2) it does not provide, when read together with the other parts of the prospectus, key information in order to aid investors when considering whether to invest in such securities. As per the Old Regime, the Summary shall not contain cross-references to other parts of the prospectus or incorporate information by reference.

Universal Registration Document

The New Regulation introduces an optional 'shelf' registration mechanic whereby issuers, whose securities are already admitted to trading on a regulated market or an MTF, may prepare and submit an annual universal registration document (a "URD") for approval by the Central Bank of Ireland (the "Central Bank"). The URD shall describe the issuer's organisation, business, financial position, earnings and prospects, governance and shareholding structure for approval.

After the issuer has had a URD approved for two consecutive financial years the issuer shall have the status of a 'frequent issuer' and all subsequent URDs and any amendments thereto may be filed without prior approval and reviewed on an ex-post basis.

A frequent issuer shall only be required to draw up a securities note and the Summary when securities are offered to the public or admitted to trading on a regulated market. The URD, accompanied by the securities note and the Summary shall constitute a prospectus. Frequent issuers also benefit from a fast-track approval process of 5 (as opposed to 10) working days.

While the URD mechanic has the potential to allow frequent issuers to access the market quickly using the fast-track approval process, this timeline is not guaranteed. Where an issuer draws up a prospectus consisting of separate documents, all constituent parts of the prospectus remain subject to approval, including, where applicable, the URD where it has been previously filed but not formally approved. It is possible that frequent issuers may be required to amend the URD and resubmit for approval, resulting in delays. As such it appears that the main intended benefit of the URD framework is negated and we expect debt issuers, such as Irish SPVs, to continue to avail of the option to register a base prospectus annually which effectively acts as a shelf approval for a note programme.

EU Growth Prospectus

The New Regulation has expanded on the proportionate disclosure concept in the Old Regime by the introduction of an 'EU Growth Prospectus'. The EU Growth Prospectus regime will allow for a lesser standard of disclosure in connection with an offer of securities to the public (but not admissions to trading on a regulated market) by certain issuers provided that they do not already have any securities admitted to trading on a regulated market.

Taken in a DCM context, this feature is primarily aimed at (1) SMEs; or (2) issuers where the offer of securities to the public is of a total consideration in the EU that does not exceed €20,000,000 calculated over a period of 12 months, and provided that such issuers have no securities traded on an MTF and have an average number of employees during the previous financial year of up to 499.

An EU Growth Prospectus under the proportionate disclosure regime shall be a document of a standardised format determined by delegation legislation, written in a simple language and which is easy for issuers to complete. It shall consist of a specific summary, a specific registration document and a securities note. A public consultation on minimum disclosure requirements, their order of presentation and the format and content of the specific summary has been undertaken by ESMA with final technical advice having been published on 3 April 2018 which specifies the minimum disclosure requirements for the EU Growth Prospectus, the order in which they should be presented, and the format and content of the specific summary .

As noted above, debt securities issued by Irish SPVs are often listed on 'recognised stock exchanges', including either the regulated (Main Securities Market) or unregulated (Global Exchange Market) markets of Euronext Dublin (formerly the Irish Stock Exchange). An EU Growth Prospectus cannot be used in connection with the admission to trading on a regulated market and the Global Exchange Market is only suitable for securities which, because of their nature, are normally bought and traded by a limited number of investors who are particularly knowledgeable in investment matters. As such, the circumstances in which Irish SPVs may use an EU Growth Prospectus for an Irish listing appear to be limited to offerings to sophisticated investors in connection with a Global Exchange Market listing. The suitability of an EU Growth Prospectus in connection with the listing on any other recognised stock exchange would need to be considered by local counsel on a case by case basis.

Risk Factors

The New Regulation will require risk factors included in a prospectus to be (1) limited to risks specific to the issuer and / or the securities in question; and (2) material for the purposes of making an informed investment decision.

The issuer must also assess the materiality of the risk factors based on the probability of their occurrence and the expected magnitude of their negative impact. The assessment of the materiality of the risk factors may also be disclosed by using a qualitative scale of low, medium or high.

Risk factors shall be presented in a limited number of categories depending on their nature. In each category, the most material risk factors shall be mentioned first according to the issuer's assessment.

These changes, and in particular the requirement for ranking according to materiality, are likely to cause practical difficulties for issuers as they seek to quantify the probability and magnitude of potential risks. Rating risk factors on a scale of low, medium or high risk appears to be optional and we do not expect issuers to risk increased prospectus liability by availing of this option.

The New Regulation provides that, in order to encourage appropriate and focused disclosure of risk factors, ESMA shall develop guidelines to assist competent authorities in their review of the specificity and materiality of risk factors and of the presentation of risk factors across categories depending on their nature. Further, the New Regulation allows the Commission to adopt delegated acts specifying criteria for the assessment of the specificity and materiality of risk factors. Any guidance on these points will be welcomed by issuers and market participants alike.

Our View

The overall direction of the New Regulation and attempts to simplify the disclosure process are welcome however the move to a more prescribed format of the prospectus, including requirements on the materiality of risk factors and restrictions on the length of the Summary are likely to create challenges for issuers.

In addition, it remains to be seen how widely some of the new features will be adopted in the DCM space - the new URD mechanic does not appear to offer debt issuers any meaningful advantage over the existing option to register an annual Base Prospectus and the increase of the Fungible Tap Issue exemption will not present any efficiencies where securities are also listed.

Key Dates

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]