- within Tax topic(s)

- in Ireland

- in Ireland

- within Family and Matrimonial topic(s)

Union Budget 2026 marks a subtle yet decisive inflection point in India's transfer pricing framework. Rather than introducing new compliance layers, the Budget focuses on simplifying existing mechanisms and embedding certainty into routine cross-border transactions. The fast-tracking of Unilateral APAs for IT services and the rationalization of the Safe Harbour regime through consolidation of fragmented IT service categories into a unified service with a margin aligned to commercial realities, an automated rule-based approval framework without tax officer intervention, and an enhanced eligibility threshold represent a welcome shift towards predictability and administrative efficiency.

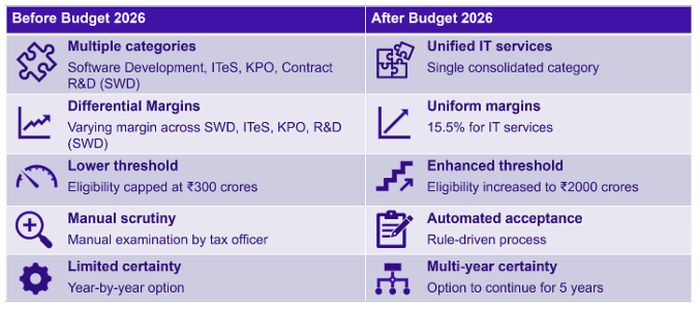

Safe Harbour Mechanism – Uniform category, one margin, automated acceptance

Safe Harbour (SH) is a transfer pricing dispute resolution mechanism where tax authorities accept the transfer price declared by a taxpayer for specific international or domestic transactions, provided they meet pre-defined criteria. It aims at reducing litigation and compliance costs, providing certainty, reduction in documentation etc. The SH typically applies to routine, non-complex cross border services such as software development services, IT-enabled services (ITeS), KPO services, Contract R&D services (software and pharmaceuticals), Manufacturing and export of core auto components, Intra group loans etc

Over time, recognizing the low adoption of SH, the margins were rationalized and scope was expanded in subsequent years with the aim of making the SH framework more attractive and accessible to small taxpayers, thereby reducing compliance and reducing disputes.

However, the adoption was still much lower than anticipated and various representations were made over the years to reduce the SH rates and increase the activities under the SH coverage.

The current Budget proposal has finally listened to the taxpayers request thereby proposing significant changes to the SH provisions.

The exiting framework included multiple categories like software development, ITeS, KPO, contract R&D relating to software development services with different rates resulting in ambiguity and the risk of the application getting rejected by the Transfer Pricing Officer (TPO) due to subjective interpretation.

With the proposed amendment, ambiguity of classification across IT/ ITeS/ KPO appears to be eliminated. Further, enhanced limit, uniform and rationalized SH margin to 15.5% for IT services, and automated rule-driven adoption instead of manual examination by tax officer, aim to encourage vast number of Companies rendering IT services to consider SH option. These amendments aim to provide greater predictability in tax position thereby encouraging Companies rendering IT service to opt for SH and significantly reduce TP audits, adjustments and litigation. This is also a great alternative to APA for routine, low risk IT services.

Recognizing the need to strengthen critical digital infrastructure and stimulate investment in data centres, the proposal seeks to extend a tax holiday up to 2047 for foreign companies that provide services to customers located outside India by procuring data centre services within India. Services supplied to Indian users, however, will be required to be routed through an Indian reseller entity and taxed in accordance with applicable domestic tax provisions.

Accordingly, recognizing the importance of data centres as critical digital infrastructure, the Budget proposes a tax holiday till 2047 for foreign companies providing cloud services to global customers using data centre infrastructure located in India.

The proposed tax holiday for foreign cloud service providers and the introduction of a 15% SH margin for Indian data centre service providers further extend the certainty-driven approach beyond traditional IT services into digital infrastructure.

Advance Pricing Agreement - Certainty, now with a clock

As per the APA Annual Report 2024–25, published in September 2025, a total of 109 UAPAs were signed across various sectors. Of these, 44 agreements pertain specifically to the Information Technology domain.

Further, the APA Annual Report 2024-25 also highlights that the time taken to conclude an APA range from 12 months to 72 months. Accordingly, the average time required to process an APA, on a cumulative basis, is approximately 45.41 months (around 4 years).

Considering that a significant portion of Unilateral APAs relate to the IT services sector and that the overall APA process can be time‑consuming, a fast‑track APA mechanism for IT services has been introduced. The objective of this initiative is to conclude Unilateral APAs for the IT sector within 2 years, with a possible extension of up to 6 months at the taxpayer's request.

This initiative is expected to significantly reduce the overall APA completion timeline from the current average of around 4 years to approximately 2 to 2.5 years. Given the TP litigation scenario in India and uncertainty on determining the arm's length price, this measure is likely to encourage more IT companies to consider entering into APA in the future. Thus, beyond ALP certainty, IT service providers now gain certainty on timelines too.

Further, with respect to Modified Return Filing- Under the existing provisions of section 168(1), only the person who has entered and concluded an APA with the CBDT is permitted to file a modified return of income. There was no provision allowing the associated enterprise, whose income and tax liability are impacted as a result of the APA, to revise its return or file a return to claim a refund of excess taxes paid or withheld.

To simplify and rationalize the provision, it is proposed that where income is revised due to an APA entered into by the Applicant, the Applicant or the related associated enterprise may file a return or a modified return, as applicable, in line with the APA. This must be done within 3 months from the end of the month in which the APA is signed, and shall apply to APAs entered into on or after 1 April 2026.

Overall, the re-engineered Safe Harbour framework and the fast-track Unilateral APA mechanism under Budget 2026 reflect a clear policy shift towards predictability, administrative efficiency, and dispute prevention in India's transfer pricing regime. By combining time-bound certainty, rationalized Safe Harbour margins, enhanced thresholds, and automated acceptance for routine IT services, the Government has significantly lowered friction for compliant taxpayers. These measures not only reduce audit intensity and litigation risk, which were expecting margins in north of 17%, but also position India as a stable and competitive jurisdiction for global IT and digital service operations, reinforcing the broader objective of ease of doing business and sustained foreign investment.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]