- within Technology, Energy and Natural Resources, Government and Public Sector topic(s)

- with readers working within the Law Firm industries

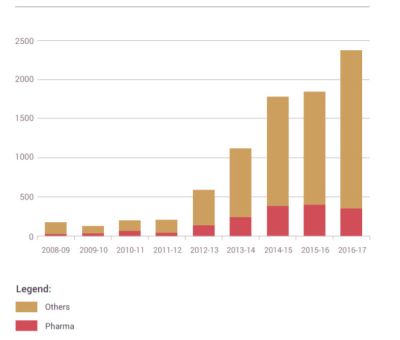

In recent years, Government of India has created a tax regime in India specially for IPR. With the rapid increase in economic development of the nation, requirement for the IPR development is a pressing need of the hour. By way of a healthy tax structure, the IPR can be escalated to the utmost level and maximum benefits can be given to the inventors for securing an innovation culture in the country. It has been seen that many startup companies do not promote or fail to promote their IP because of the future financial loss or lack of knowledge. A better taxation model may catalyze the research and development of intellectual property assets in such startups and they may think to rejuvenate the IP. Also, a good IP taxation regime and efficient royalty policies would persuade the authors and artists to come up with more original & artistic works and expand the number of technologies or know-how transfers into India.

First, let us discuss the tax benefits and the benefits to Startup/ SMEs:

SECTION 80 IAC: Post getting recognition, a startup may apply for tax exemption under section 80 IAC of the Income Tax Act. Section 80 IAC of Income Tax Act, 1961, provides for Income tax exemption to recognized startups for any 3 consecutive years out of a block of 7 years (10 years for startups from Bio-Technology Sector) from the date of its incorporation. Eligibility criteria for applying to income tax exemption (80IAC) are:

- The entity should be a recognized startup

- Only Private limited or a Limited Liability Partnership is eligible

- The startup should have been incorporated after April 01, 2016

Section 56: Angel tax1 - Post getting recognition, a startup may apply for Angel Tax Exemption. Eligibility criteria for tax exemption under Section 56 of the Income Tax Act are:

- The entity should be a DPIIT recognized startup

- Aggregate amount of paid up share capital and share premium of the startup after the proposed issue of share, if any, does not exceed INR 25 Crore.

Other Benefits for Intellectual Property for startups:

- Fast tracking of patent applications

- Expedited examination

- 90% reduction in official fee

- Waiver of professional fee

SMEs: Support for International Patent Protection in E&IT (SIP-EIT) is a scheme launched by the Department of Electronics and Information Technology to provide financial support to MSMEs and Technology start-up units for international patent filing. SIP-EIT scheme captures the growth opportunities in the area of information technology and electronics. This scheme encourages indigenous innovation and also recognizes the value and capabilities of global IP. The reimbursement limit has been set to a maximum of Rs. 15 lakhs per invention or 50% of the total charges incurred in filing and processing of a patent application, whichever is lesser2.

There are various sections introduced by government in the Income Tax Act, 1961, such as sections 32(1) (ii), 35A, 35AB, 80 GGA, 80-O, 80OQA, 80QQB, 80RRB etc.

Currently, the manufacturing of an IP includes various transactions which are taxed separately:

- Deduction: The capital used for research and development of an IP which is the pre-existing stage including the analysis cost, manufacturing cost, etc is treated as an expense which is to be deducted from the gross income for further calculation of income tax.

- Income: The income received as royalty by transfer of IP is treated and taxed under the Income Tax Act, 1961. To promote innovation in the country, royalty income is given tax incentives.

- GST: Tax on Sale/ Transfer/ Licensing/ Assignment of the intellectual property.

Once the IP is created, it can be commercialized either by integrating it into products and selling them or the right to use the IP can be transferred temporarily or permanently, and is subject to taxation under the Indian Taxation system of direct and indirect taxes.

- Royalty: Royalties are taxable income and also a business expense. If you receive royalties from someone for use of your property, you must claim these payments as business income. Royalty income is taxable in respect of any right, property or information used or services utilized by a non-resident, in India or for the purposes of making or earning any income from any source in India. If such income is payable in pursuance of an agreement made before the 1st day of April 1976, and the agreement is approved by the Central Government, is not taxable.3

- Depreciation: Section 32(1)(ii) of the Act accounts for depreciation of the intellectual property as expenditure for the purpose of calculation of income tax.

- Expenditure: Section 35A of the Income Tax Act 1961, explained the expenditure on acquisition of patents and copyrights rights.

- Depreciation over the acquired patents and copyrights shall be claimed over a period of time when the consideration is paid in lump sum. In a scenario where the consideration is paid on periodical timeline, the depreciation can be claimed as expenditure fully incurred for the purpose of business. Provided any expenditure incurred after the 28th day of February 1966, but before 1st April 1998, on the acquisition of patent rights or copyrights for the purpose of business, deductions will be allowed for each of the previous years on an amount equal to the appropriate fraction of the amount spread over 14 years.

- Deductions are not applicable to amalgamating companies in the case of amalgamations, if the amalgamating company sells or otherwise transfers the rights to the amalgamated company (being Indian company).

Section 35AB states that where the assesse has paid any lump sum consideration for acquiring any know-how for the use of his business, the expenditure for the same shall be deductible in six equal installments for six years:

- one-sixth of the amount so paid shall be deducted in computing the profits and gains of the business for that previous year, and

- the balance amount shall be deducted in equal installments for each of the five immediately succeeding previous years.

Deduction: Section 80 GGA talks about certain other deductions for scientific research which are provided under the head "deduction in respect of certain donation for scientific research or rural development" – Any sum paid for scientific research or to a university, college or institution to be used for scientific research. The research work for the development of a patent comes under the umbrella of scientific research.

Under present laws, expense deductions and additional weighted deductions are permitted to all taxpayers for R&D expenditure. Such weighted deduction is restricted to 150% of the expenditure from tax year 2017/18 to tax year 2019/20. Thereafter, deduction will be restricted to 100% of the expenditure.

Section 80O provides and that no deduction shall be allowed in respect of the assessment year beginning on the 1st day of April, 2005, and for subsequent years for income from patents.

Section 80 OQA states that a deduction of 25% shall be allowed from any income obtained by the author in exercise of his profession on account of any lump sum consideration for the assignment or grant of any of his interests in the copyright of any of his books or of royalty or copyright fees.

Exceptions to 80 OQA: No deduction in case of:

- Dictionary

- Thesaurus

- Encyclopedia,

- Any book that has been added as a textbook in the curriculum by any university for degree of graduate or post graduate course of the university, or

Any book which is written in any language specified in the 8th schedule of the constitution or in any other language as the Central Government by notification in the official gazette specifies for the promotional need of the language. Section 80QQB, highlights the deductions to be made in respect of royalty income of authors of certain books other than textbooks.

Section 88 RRB deals with the deductions on payment of royalties for patents. In some cases, the total income earned by an individual on a patent can be divided into royalty and additional income classified not under royalty. In all cases, the income received as royalty alone is eligible for tax deduction; it states that when income is received as a royalty, the whole income or Rs. 3 lakhs (whichever is lesser) shall be deducted.

When a compulsory license is being granted in respect of any patent, the terms and conditions of the license agreement shall decide the status of the income by way of royalty. For the purpose of allowing deduction under this section which shall not exceed the amount of royalty.

Deductions under Section 80 RRB can be claimed only upon satisfaction of a few basic criteria by the inventor:

- The individual claiming a deduction should be an Indian resident.

- Only patentees can claim this tax deduction.

- Individuals who do not hold the original patent are not eligible for tax benefits.

- The patent under Section RRB in question should be registered under the Patent Act of 1970, either on or after April 1, 2003.

Patent Box Regime4: Section 115BBF provides concessional rate of taxation at 10% on royalty income in respect of exploitation of patents granted under Patents Act, 1970, and is only applicable to Indian resident who is a patentee (eligible taxpayer). The total income of eligible taxpayer must include income by way of royalty in respect of patent developed and registered in India and atleast 75% of the expenditure is incurred in India by eligible taxpayer for invention No other expenditure is allowed under the tax provisions if concessional tax rate under Section 115BBF is availed.

The eligible taxpayer has an option to avail the benefit of Section 115BBF in any year but he is required to continue to avail the benefit for next 5 years because in case option is not exercised in any of such 5 consecutive years, he shall not be eligible to take the benefit under the section for the next 5 years following such year in which option is not exercised.5

With this tax structure we are very much sure that keeping an IPR as an asset will be a good deal for the companies. The government is giving huge tax benefits along with redemptions in the official fees to boost up the IP culture in the country.

Footnotes

2. SIP-EIT Scheme, https://www.indiafilings.com/learn/sip-eit-scheme/

3. Section 9(1)(vi) of The Income Tax Act, 1961

4. https://cleartax.in/s/patent-tax-treatment

5. Tax on Income from Patents – Patent Box Regime, https://cleartax.in/s/patent-tax-treatment#choose (accessed on 12th June'19)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.