- within Corporate/Commercial Law topic(s)

- in India

- with readers working within the Law Firm industries

- within Corporate/Commercial Law, Government, Public Sector, Media, Telecoms, IT and Entertainment topic(s)

Indian economy | May 2026

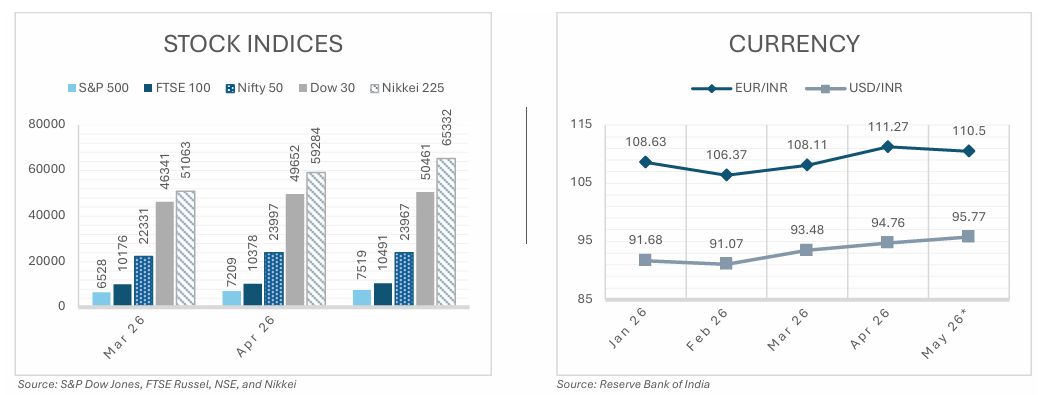

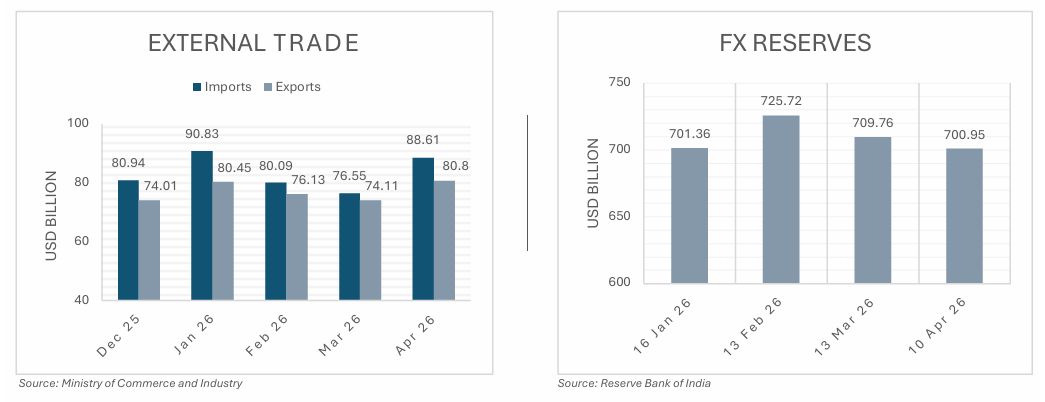

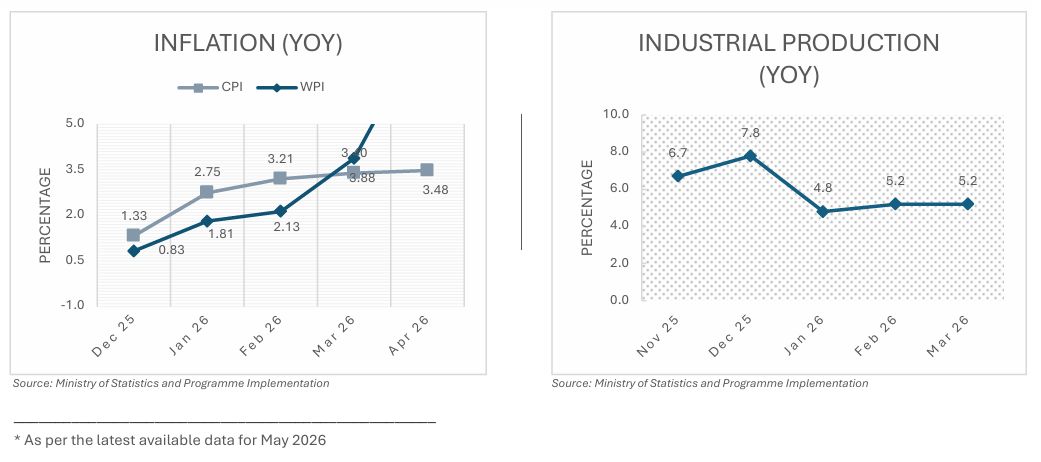

Snapshot of key indicators

SEBI streamlines settlement mechanism for FPIs

Circular on FPI net settlement of funds

Until now, Foreign Portfolio Investors (FPIs) were required to settle each transaction individually on a gross basis. This meant the full value of each purchase had to be funded upfront, irrespective of any sale proceeds that the FPI was simultaneously receiving on the same day. In practice, this locked up large amounts of capital for short periods, increased the need for forex conversions, and raised the overall cost of operating in Indian markets. Addressing this concern, the Securities and Exchange Board of India (SEBI) introduced the concept of net settlement for funds on a limited and calibrated basis, bringing Indian market practice in line with global standards already followed in the United States (via the DTCC system) and Europe (under CSDR regulations). The change shall take effect from 31 December 2026.

Key changes

- Net funds settlement permitted: FPIs may now use the proceeds from a sale to meet a purchase obligation arising within the same settlement cycle. Only the net difference needs to be arranged, significantly reducing the amount of capital that must be kept ready at any given time. For example, in the case of a purchase worth INR 10 crore and a sale worth INR 7 crores on the same day, the FPI only needs to arrange the balance INR 3 crores, effectively freeing up INR 7 crores of capital that would otherwise have been blocked under the old mechanism.

- Gross settlement applicability: The actual transfer of shares continues on a gross basis. Each securities transaction is processed individually and remains separately traceable. The reform applies only to the funds side of the settlement, not to the delivery of the underlying securities. This ensures that ownership records and delivery discipline are fully maintained.

- Taxes unchanged: Statutory levies such as Securities Transaction Tax (STT) and stamp duty are unaffected. This reform is limited to settlement mechanics only.

Outright transactions in distinct securities: The netting benefit applies only to ‘outright transactions’ defined as either a purchase or a sale in a security within a settlement cycle, but not both. Where an FPI has both purchase and sale transactions in the same security within the same settlement cycle, gross settlement continues to apply. Additionally, excess outright sale proceeds cannot be applied towards non-outright purchase obligations.

Counterparty risk: If an FPI’s sale transaction fails, the expected proceeds cannot be used to fund the purchase, potentially causing a settlement failure. If a sale transaction fails or is not confirmed by the custodian, its proceeds cannot be used for netting purposes. This ensures that only verified trades benefit from the liquidity advantages of net settlement while reducing settlement risk.

Calibrated rollout: Netting calculations across multiple transactions within a single settlement cycle introduce the possibility of computational errors. SEBI’s decision to limit the netting mechanism to eligible outright transactions, rather than all trades, is a deliberate precaution to contain this risk during the initial phase of implementation.

The net settlement framework is a practical, industry responsive reform that addresses a long-standing structural inefficiency in India’s capital markets. For FPIs, the immediate benefit is a meaningful reduction in the amount of capital that needs to be pre-funded for daily trading activity, along with lower forex conversion costs and reduced operational friction. For the broader market, greater FPI participation and improved liquidity efficiency are the expected outcomes.

At the same time, the partial nature of the reform signals that SEBI is proceeding cautiously. This is understandable given that linking the buy and sell legs of a trade introduces new risks that need to be carefully managed. The success of the framework will ultimately depend on the robustness of custodian oversight, the accuracy of netting systems, and the speed with which settlement failures are identified and managed. Depending on how smoothly implementation proceeds, a broader extension of net settlement to additional transaction types is a reasonable prospect in the medium term

To view the full article please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.