As published in 'Accountancy Cyprus', the Journal of the Institute of Certified Public Accountants of Cyprus, March 2019 edition.

Download >> IFRS 9 For Corporates: Is The Grass Greener On The Other Side?

IFRS 9, the new financial instruments reporting standard, is widely recognised as having a profound impact on banks. But what about corporates? There is a common misperception, that, IFRS 9 will have little or no impact. This is not the case!

An entity may have to face significant changes and challenges with its financial reporting, IT systems, processes and controls as a result of applying this standard. This is certain to be the case for those intra-group loans, equity and debt securities, or even financial guarantee contracts. It might even be the case for those holding short-term trade and intra group receivables. It all greatly depends.

Classification & Measurement

IFRS 9 has a more simplified approach for classifying and measuring financial assets, compared to IAS 39. However, the fact that the approach is described as simplified, doesn't necessarily mean it is simple. Entities will be now required to assess under which business models they manage their financial assets and understand the characteristics of the contractual cash flows they collect from those assets. Determining whether the terms governing loans and receivables are "in accordance with a basic lending arrangement", in order to justify measurement at either amortised cost or fair value, can be a real challenge in practice.

Although the new requirements can lead to similar measurement categories as per IAS 39, one cannot presume that this will always be the case for every single financial asset. The only time, one can safely assume the classification and measurement of a financial asset will always be the same with IAS 39, is for non-hedging derivatives, which are, and forever will be measured, at FVTPL.

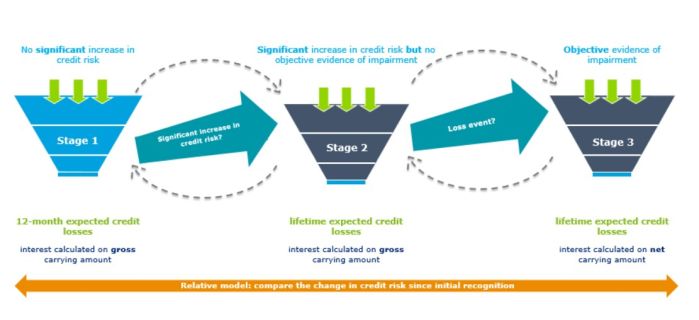

Impairment

When it comes to Impairment, IFRS 9 brings about wholesale changes, as it moves from an "incurred loss" to an "expected loss" impairment model. The standard follows a forward-looking approach, and companies will have to recognise immediately a certain amount of expected credit losses (ECL). This is because, every receivable, loan or other financial asset, carries a certain risk of default. Every such asset, inevitably, has an ECL attached to it, from the very moment of its origination until its final maturity. Consequently, the impact of IFRS 9 impairment requirements will vary between companies, across portfolios as well as be subject to more stringent data and methodology requirements.

Under the general model of impairment, entities must recognise ECL in two stages. For credit exposures for which there has not been a significant increase in credit risk since initial recognition, entities are required to provide for those credit losses that result from default events which are possible within the 12 months after the reporting date, i.e. 12-month ECL or Stage 1. For those credit exposures for which there has been a significant increase in credit risk since initial recognition, a loss allowance is required for credit losses that result from all possible default events over the expected life of the financial instrument, irrespective of the timing of default i.e. a lifetime ECL or Stage 2 or 3 (see Figure 1 below).

Apart from the general model of impairment, there are simplification options available which are applicable for trade receivables, contract assets that do not contain a significant financing component (see IFRS 15) and lease receivables (see IFRS 16). The simplified approach does not require tracking the changes in credit risk, but instead requires the recognition of lifetime ECLs at all times (see Figure 2 below). For trade receivables or contract assets, entities are required to apply the simplified approach.

Further to Deloitte's publication: Applying the expected credit loss model to trade receivables using a provision matrix, one may use it as a practical expedient to determine ECL for trade receivables. The provision matrix follows an approach based on the entity's historical default rates over the life of its trade receivables and thereafter adjusted with forward-looking information. The use of such a tool provides some relief from the need to track changes and most importantly offers the ability to entities to apply consistently their ECL methodology.

Furthermore, IFRS 9 eliminates the need for an impairment assessment for equity instruments, and establishes a new approach that is based on measuring equity instruments purely at fair values. An irrevocable election can be made at initial recognition, to measure equity instruments that are not held for trading, at FVOCI. Therefore, although the IFRS 9 model is simpler than IAS 39, it comes at a price, the inherent threat of volatility in profit or loss from moving to a fair value approach.

Modification of financial instruments

Contrary to widespread belief, modifications of financial instruments is an area that if not carefully considered, may cause unpleasant surprises to the profit and loss. When the terms of a financial instrument are modified, entities need to consider whether the modification is substantial. If the modification is considered substantial the original financial instrument is derecognised and a new financial instrument is recognised at fair value. The process for assessing whether a modification to the terms of a financial instrument is substantial is the same under both IAS 39 and IFRS 9. However, the treatment of a non-substantial modification is different.

Previously, there was some ambiguity around the accounting treatment for a non-substantial modification of a financial instrument. Deloitte's publication, Impact of transition from IAS 39 to IFRS 9 on the exchange of or modification of financial liabilities, clarifies, that, under IFRS 9 a gain or loss should be recognised at the time of a non-substantial modification, and for this reason, modifications of financial instruments are particularly important under IFRS 9.

Final thoughts

The impact of this standard goes well beyond a simple technical change in accounting policy. It requires coordinating multi-disciplinary effort from various functions within an organization, from Risk and Finance, to IT and Business.

IFRS 9 will eventually change the way entities manage risk, as its impact could be significant in terms of capital and business model management. The impairment model is likely to have a negative impact on equity and bottom line profit, but it is also likely to generate more volatility when it comes to impairment. These consequences may persuade organisations among others to review and rethink their current risk management strategies, business models, the financial instruments they use to manage financial risks and restructure, divest and reposition themselves in other market segments.

Data availability is pivotal to successful IFRS 9 application. Issues around data quality, availability, appropriate format and eventual collection are likely to be at the forefront of the implementation efforts for IFRS 9. It is therefore essential to plan the implementation ahead of new systems, processes and modelling tools, in order to prepare for the inevitable organisational and governance changes to come.

So, is the grass greener on the other side for corporates?

IFRS 9 will affect almost all entities and not just large financial institutions. Where entities have material trade receivables, contract asset and lease receivable balances, special attention is required to ensure that an appropriate process and methodology is put in place to calculate the expected credit losses.

Moving to IFRS 9 will likely have some significant upsides as it creates significant opportunities for corporates to get their accounting more aligned with how they manage risk. Risk is a key investor focus, so "telling the risk management story" better, will align any organisation's communication strategy with investors' expectations.

With careful planning, the changes introduced by IFRS 9, might prove to be a great opportunity for balance sheet optimization. Left unattended for too long, IFRS 9 may hide some nasty surprises. Either way, there's enough at stake already, and entities that haven't begun assessing the standard's implications, will have to beat the ticking clock.

All in all, corporates can accept reality for what it is, embrace this opportunity to develop, to improve, and leverage on the changes that IFRS 9 brings to their business. So, is the grass greener on the other side for corporates? Rather than simply stating that the grass is always greener on the other side, I would say that the grass is greenest where it is watered.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.