1 Introduction

1.1 The implementation of the Notional Interest Deduction ("NID") rule in Cyprus since July 2015 has created a powerful tool to local and international organisations seeking new options to finance their operations. By using NID, businesses have the opportunity to deleverage and realise a new, tax efficient return on new equity, via the deduction of a 'notional' interest expense against their taxable income.

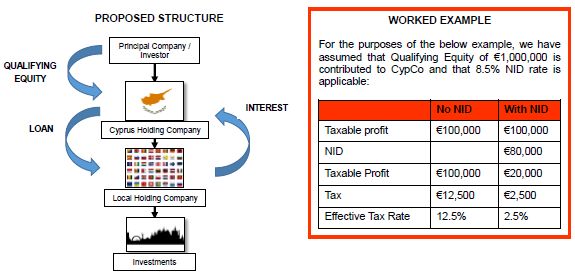

1.2 Equity financing in Cyprus can therefore constitute a very useful alternative to debt financing (thus avoiding the use of, now inefficient, offshore financing parents of the Cypriot company). The use of NID can achieve effective tax rates in Cyprus of as low as 2.5%.

2 How it works

2.1 The NID rate is equal to the higher of:

2.1.1 3% plus the yield on the 10-year government bonds (as at 31 December of the year preceding the tax year the NID is claimed) of the country where the funds are deployed (e.g. in Ukraine); and

2.1.2 3% plus the yield on 10-year government bonds of Cyprus.

2.2 The NID rule works as follows:

2.2.1 qualifying equity1 is contributed to the Cypriot company;

2.2.2 a tax deduction is allowed following the application of the NID rate to the amount of qualifying equity contributed to the Cypriot company (the deduction is made in a similar manner as if it was actual interest expense i.e. only if it is used to finance business assets);

2.2.3 NID is deducted following the determination of the taxable profit of the company, which can be up to a maximum of 80% of the taxable profits of the company. This deduction is made annually and in perpetuity.

3 Worked Example

Footnote

1. Qualifying equity is generally equity contributed (in cash or in kind): (i) as from 1 January 2015 in the form of paid up share capital of share premium; or (ii) pre-existing shareholder reserves which are converted into share capital.

Originally published February 2018

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.