The Indonesian Directorate General of Taxation issued two key tax regulations (the "Regulations") dated 5 November 2009 (Director General of Tax Regulations Nos. 61/PJ/2009 and 62/PJ/2009). The Regulations provide long awaited clarification on the withholding tax treatment of the typical structure used for Indonesian bond issuances. Our initial impressions are that the Regulations will have significant implications for Indonesian bond issuances, and will likely affect existing issuances as well as new ones.

Typical Indonesian Bond Structures

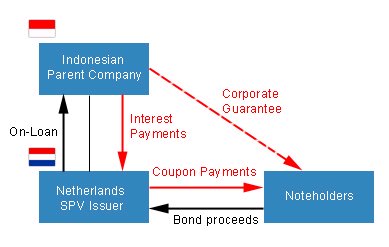

Most international bond issuances by Indonesian corporations employ an 'SPV issuer' structure designed to limit withholding tax on interest income. Indonesian corporations are required to withhold tax on interest payments to offshore parties at the rate of twenty percent (20%), unless this rate is reduced by an applicable double taxation treaty. Under the usual SPV issuer structure illustrated below, an Indonesian corporation wishing to issue bonds sets up a special purpose subsidiary in a jurisdiction with a favourable double taxation treaty with Indonesia. The subsidiary then issues the bonds and on-lends the proceeds to the Indonesian parent company. Payments under the bonds are guaranteed by the Indonesian parent.

The concept is that interest payments on the loan would be subject to withholding tax at the rate specified in the double taxation treaty between Indonesia and the jurisdiction of the special purpose issuer. The intent of the structure is to reduce the withholding tax rate from twenty percent (20%) (the default position if no tax treaty applies) to the more favourable rate under the double taxation treaty. Variants on this structure were commonly used to reduce withholding tax payments on offshore bond interest payments to ten percent (10%), which was the best available treaty rate prior to ratification of the updated Netherlands-Indonesia tax treaty, which came into effect on 1 January 2004.

The commercial effect of the SPV issuer structure was to ensure that the withholding tax rate applicable to offshore bond issuances was at the same rate as that applicable to most offshore bank loans, as most offshore banks would be able to book their loans to Indonesian corporations through a branch office in a jurisdiction with a ten percent (10%) treaty rate. The turning point for the SPV issuer structure came with the ratification of the new Netherlands-Indonesia tax treaty, which provided for a zero percent (0%) withholding tax rate on interest payments. This created the potential for huge tax savings by Indonesian corporations, and the complete loss of an important revenue source for the Indonesian tax authorities. The Indonesian corporations were not slow to take advantage of the new treaty rate, and the Indonesian tax authorities responded with policy measures designed to mitigate the loss of this revenue stream.

Policy Response And Complications

The policy response by the Indonesian tax authorities was initially to issue two circular letters in 2005. The position taken in the first circular letter was that the zero percent (0%) rate under the new Netherlands-Indonesia tax treaty could not yet be implemented. This was on the basis that the treaty contemplated implementing measures which had not been agreed by the treaty parties, and accordingly the rate of ten percent (10%) under the previous treaty would continue to apply. The new Netherlands-Indonesia tax treaty closely followed the OECD model form, and this interpretation was challenged by the Netherlands (as well as Indonesian corporations) as being inconsistent with international OECD tax treaty practice.

The position taken in the second circular letter was to argue that the SPV issuer was not the 'beneficial owner' of the interest income as required by the treaty. If this position were correct, the SPV issuer would not be entitled to receive treaty benefits at all, and the default withholding rate of twenty percent (20%) would therefore apply. This argument was at the time being advanced before the English courts in the case of Indofood International Finance v JP Morgan Chase Bank, and was ultimately upheld by the English Court of Appeal. The English court held that the term 'beneficial owner' in the OECD model form tax treaty was to be given an 'international fiscal meaning', which essentially meant that Indonesia was entitled to adopt its own interpretation of the term, so long as it fell broadly within international norms.

The complications arose for a number of reasons. The first circular letter was never withdrawn and continued to be relied upon by the tax authorities from time to time, so Indonesian corporations were faced with two fundamentally inconsistent policy statements which would result in two different withholding tax rates for the same structure. In addition, the criteria for 'beneficial ownership' in the second circular letter were broadly expressed and difficult to apply in practice. An updated version of the circular letter in 2008 did not do much to clarify matters. To further complicate matters, the circular letters had no formal status under Indonesian law but only constituted guidance on the policy approach intended to be applied by the Indonesian tax authorities. Accordingly, the interpretations set out in the circular letters were open to challenge before the Indonesian tax courts.

As a result, the withholding tax position on Indonesian bond issuances has been unclear for some time. Issuers have generally taken two broad approaches. Some have gone ahead with a Netherlands SPV issuer and unilaterally apply the zero percent (0%) withholding tax rate, choosing to challenge the availability of such treaty benefits in the Indonesian tax courts. Others have chosen to establish an SPV in a jurisdiction which would result in a ten percent (10%) withholding tax rate under the relevant tax treaty. Based on our discussions with clients, we understand that the tax authorities have not generally challenged the application of a ten percent (10%) withholding tax rate. However, we have heard that corporations applying the zero percent (0%) rate have been informed that they will be charged at the full twenty percent (20%) rate (plus penalties) if they do not accept a compromise ten percent (10%) rate.

The New Regulations

The Regulations are intended to provide much needed clarification as to the criteria for a beneficial owner to obtain treaty benefits. They are a formal regulatory response and have binding force, unlike the earlier circular letters. The earlier circular letters have been repealed and superseded by the Regulations.

Under Regulation No. 62/PJ/2009, the conditions for income recipients to enjoy the treaty benefits include:

- The company is not established in the jurisdiction of the relevant treaty's counterparty merely to obtain the treaty benefits, and the transaction itself is not structured solely to take advantage of the treaty benefits.

- The company has independent management with sufficient authority to conduct its business.

- The company has employees.

- The company has an active operation or business.

- The company is subject to tax in its jurisdiction of residence on the Indonesia sourced income.

- 50% or more of the company's income is not used to satisfy an obligation to another party in a form of e.g. interest, royalty or other reward.

It is clear that special purpose companies established for Indonesian bond issuances under the current 'SPV issuer' structure would not meet these criteria.

Regulation Number 61/PJ/2009 provides procedures for obtaining the tax benefits, which includes submission of an original tax residency certificate by the income recipient. This is a major practical obstacle to claiming treaty benefits under international bond issuances. Bonds frequently change hands and issuers are often unaware of the identity of the holders, and it is generally impractical as a logistical matter to collect tax residency certificates from bondholders. This means that Indonesian issuers may not be able to obtain treaty benefits even if the bondholders are located in jurisdictions that have double taxation treaties with Indonesia.

Initial Conclusions

Our initial impressions are that these rulings will have significant implications for Indonesian bond issuances, and will likely affect existing issuances as well as new ones. This also seems to invalidate the commonly used practical approach of selecting an alternative jurisdiction to the Netherlands for the special purpose issuer and settling for a ten percent (10%) treaty rate.

With current Indonesian bond yields ranging from about seven point five percent (7.5%) to twelve point five percent (12.5%) (and higher for highly structured deals), the additional withholding tax burden will be significant. If our conclusions are correct, these rulings may make bond financing significantly less attractive to Indonesian corporations than bank financing. We are currently looking at alternative structures in compliance with the Regulations, with the intent of preserving the option of issuing bonds at a ten percent (10%) withholding tax rate - the rate which has historically been accepted by the Indonesian tax authorities. We are actively discussing alternatives with a number of onshore and offshore advisers and hope to provide an update on this soon.

O'Melveny & Myers LLP routinely provides advice to clients on complex transactions in which these issues may arise, including finance, mergers and acquisitions, and licensing arrangements. If you have any questions about the operation of the applicable statutory provisions or the case law interpreting these provisions, please contact any of the attorneys listed on this alert.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.