- within Transport and Strategy topic(s)

- with readers working within the Media & Information and Transport industries

Letters of Wishes (sometimes called Memorandum of Wishes) are non-binding documents that provide guidance as to the object and purpose of Estate Planning documents and also allow the formal documents (such as a Will or Trust instruments) to remain flexible and broad.

Common uses include:

- Wills – to provide guidance to the Executors and the Trustees of Trusts established under the Will.

- Minor children – to provide guidance to Guardians of minor children appointed under a Will.

- Potential contentious Estates – to provide reasoning to the Executor as to why a certain beneficiary is not named in a Will.

- Discretionary Family Trusts – to provide guidance to the Appointors, Guardians and Trustees.

- Charitable giving – to provide named Beneficiaries of a Will with an understanding that the Testator intended them to pass gifts left in their names to certain preferred charities.

Care must be exercised when drafting Letters of Wishes so that they are not deemed to be "informal wills", as if drafted incorrectly, they may conflict with the main Will and expose the estate to litigation. The Letter of Wishes should:

- be addressed to the correct person (e.g. the executor or the trustee of a relevant trust);

- contain a statement to the effect that the maker understands that it is unenforceable;

- state that it is not to be read as a formal testamentary document;

- be marked as private and confidential;

and should not:

- fetter a trustee's discretion;

- contain directive language; and

- impose any legal repercussions if it is not followed or if it is disregarded.

The case of Monaghan v Monaghan [2016] NSWSC 1316 explores Letters of Wishes in practice.

Monaghan v Monaghan [2016] NSWSC 1316

This case concerned a Memorandum of Wishes prepared by the deceased in connection with a discretionary family trust.

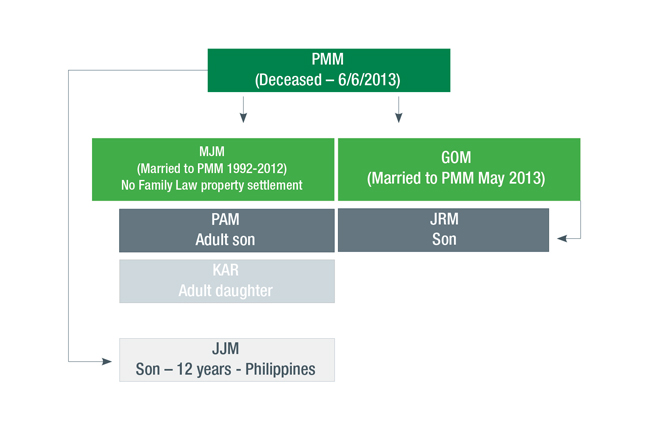

Family structure

Facts

- PMM's assets included The Monaghan Discretionary Trust (Trust), constituted by a trust deed dated 27 February 2003 (Trust Deed).

Trustee: Peter M Monaghan Pty Ltd (PMM sole shareholder and

director)

Principal: PMM

Upon PMM's death

Trustee: Peter M Monaghan Pty Ltd (PAM now sole shareholder and director) pursuant to section 201F(2) of the Corporations Act 2001.

- PMM's Will was dated 28 May 2013 (Will). Key elements of the Will included:

-

- Executor: PAM and accountant Dennis Banks.

- Gifts to children:

-

- PAM: $250,000 plus his grandfather's chair

- JMH: $100,000

- PAM and JMH: jewellery in equal shares

- KAR: $10,000

- Gift to ex-wife MJM: $50,000

- Gift to wife GOM: $50,000

- Gift of residuary estate: PAM and JMH in equal shares

- Wish concerning Trust:

"IT IS MY WISH that my executors in their role as directors of PETER MONAGHAN PTY LIMITED exercise their discretion to divide the Assets held on Trust in the Monaghan Discretionary Trust equally among my sons PETER ALEXANDER MONAGHAN and JUSTIN RYAN MONAGHAN."

- Outside of the Will, PMM had earlier prepared a memorandum of wishes in relation to the Trust on 4 June 2007 (Memorandum of Wishes) to declare his wishes as to the Trust assets in the event of his death, namely that they should be applied as though they notionally formed part of his estate.

"This Memorandum of Wishes has been prepared by me in connection with Monaghan Discretionary TRUST, being a Trust established by Deed of Settlement dated 27.02.03 between ACIS Settlements Pty Ltd as Settlor and Peter M. Monaghan Pty Ltd as Trustee as amended from time to time ('the Trust') to convey to the Trustee of the Trust my wishes in respect of the distribution of the capital and income of the Trust following my death.

It is my wish that following my death the capital and income of the Trust should be applied by the Trustee as if that capital and income formed part of my estate and accordingly was subject to distribution in accordance with my Will, to the intent that, the Trustee of the Trust should notionally add the capital and income of the Trust to the assets of my estate and deal with the capital and income of the Trust as if the capital and income of the Trust formed part of my estate for distribution along with the assets of my estate in accordance with my Will."

- MJM and GOM each brought proceedings under the Succession Act 2006 for family provision out of PMM's estate.

- The family provision proceeding were compromised and a Deed of Settlement evidencing the compromise was executed on 23 March 2016 (March 2016 Deed). The notable terms included:

-

- MJM to receive a property in lieu of the provision made in the Will;

- GOM to receive provision in accordance with the Will; and

- the Trust assets be distributed equally between MJM, GOM and PAM.

- The March 2016 Deed required, to give effect to the terms of the settlement, vesting of the Trust and distribution of the Trust assets. This was irrespective of the fact that no order was made by the Court to deem the Trust as notional estate.

- The Trustee requested the Court to provide judicial advice under section 63 of the Trustees Act 1925 as to whether it would be justified in agreeing to give effect to the terms of settlement in this way.

The Trustees dilemma

- The Trustee was faced with the Memorandum of Wishes and the March 2016 Deed.

- The Trustee contemplated giving effect to the Memorandum of Wishes to distribute all of the Trust assets as though they were part of the estate and so that they could be dealt with in accordance with the March 2016 Deed.

The Trustee position

- The Trustee is entitled to take into account a memorandum in exercising its discretions conferred under the Trust Deed, just as the Trustee is entitled to take into account the views of the beneficiaries.

- The questions that arise are:

-

- whether the Trustee is justified in acting in accordance with the Memorandum of Wishes; and

- whether the Trust Deed and trust law allows the Trustee to perform the wishes requested of him by the Memorandum of Wishes.

Does the Trust Deed allow for the wishes?

- The Court considered:

-

- the Trust Deed provided a procedure for the Trustee to determine in its absolute discretion the distribution of income or capital account;

- the Trust Deed permits the Trustee to advance the perpetuity date; and

- PAM as Executor of PMM's Will was permitted to exercise the Principal's powers.

The Court's view

- The Court provided the following judicial advice:

"that the Trustee would be justified in proceeding...by exercising the Trustee's powers...to advance the Perpetuity Date and then...distribute the Trust property in accordance with the Deed [March 2016 Deed] equally to Madeline, Gerlie and Peter in his personal capacity".

- That is, in this case the Court advised the Trustee that it would be appropriate to exercise its discretion in support of the terms of the Memorandum of Wishes (by treating the Trust assets as though they were part of the estate) which would give effect to the terms of the March 2016 Deed.

The result

- The Trustee exercised its discretion and followed the judicial advice, giving effect to the settlement and an equitable outcome for all parties.

- It is evident that it is important to:

-

- review, and if necessary, update Letters of Wishes / Memorandum of Wishes when there is a change of circumstance (E.g. ending of a marriage, commencement of a marriage, birth of children);

- assess the wishes expressed and whether the Executor or Trustee can in fact perform those wishes (that is, what is the scope of powers in the Will or Trust Deed); and

- understand that the wishes are non-binding and other factors may impact the decision making of the person to whom the wishes are directed.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]

")