- with Finance and Tax Executives and Inhouse Counsel

- with readers working within the Media & Information industries

For many financial services and credit businesses, holding an Australian Financial Services Licence (AFSL) or Australian Credit Licence is fundamental to operating lawfully in Australia. However, some businesses face licence cancellations or suspensions as a result of compliance failures or inactivity. Licence suspensions or cancellations can lead to forced cessation of business, reputational damage and banning or disqualifications of key individuals involved in the business. We explore some of the common triggers for licence cancellations and suspensions, as well as practical tips for how you can avoid them.

Common triggers for licence cancellations and suspensions include:

- ceasing to carry on a financial services business or engage in credit activities;

- failing to commence operations within six (6) months of the licence being granted – read more here;

- failing to comply with general conduct obligations under section 912A of the Corporations Act 2001 (Cth) or section 47 of the National Consumer Credit Protection Act 2009 (Cth) – these include but are not limited to:

- adequately supervising representatives and taking reasonable steps to ensure they comply with financial services or credit laws;

- maintaining the competence required to provide the financial or credit services under the licence, including replacing key persons who have left the business within the required timeframes, having active responsible managers, and ensuring training requirements are met – read more here and here;

- maintaining sufficient resources, including meeting the minimum financial requirements;

- maintaining membership with the Australian Financial Complaints Authority (AFCA) (where applicable);

- complying with financial services and credit laws, such as obligations regarding disclosure, breach reporting and lodgement of annual compliance certificates (for Australian Credit Licence holders);

- complying with conflict management and risk management obligations;

- failing to pay ASIC industry funding levies in full for at least 12 months after the payment due date – read more here and here;

- failing to prepare and lodge statutory audit and financial reports on time (for AFSL holders);

- failing to pay the Compensation Scheme of Last Resort (CSLR) annual levy;

- failing to pay an AFCA determination and the CSLR subsequently pays compensation – – read more here; and

- making false or misleading statements to ASIC.

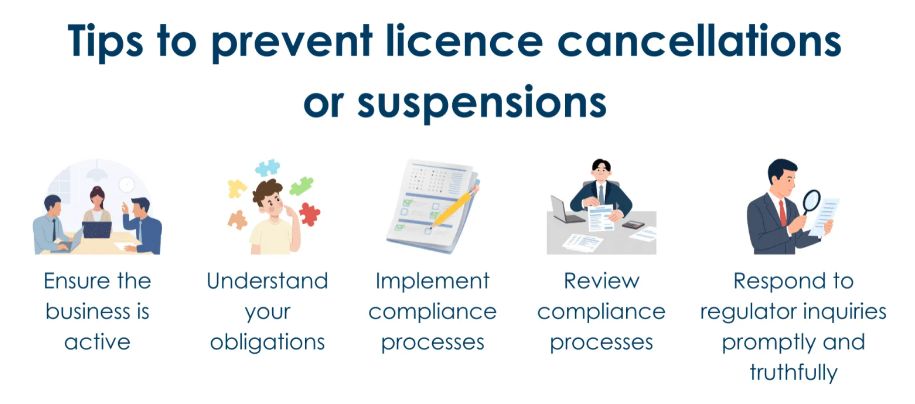

Practical tips for licensees

To prevent your licence being suspended or cancelled, we recommend:

- Ensuring the business is active – It is important that licensees are using their licence. There are various ways that ASIC could be alerted to the possibility that a business has ceased activities, such as through non-lodgement of required reports, non-payment of levies, and financial statements indicating a low level of activity.

- Understanding your obligations – Licensees must understand the obligations that apply to them and what actions they must or should take to comply. Representatives and Responsible Managers should undertake training that is appropriate to their roles.

- Implementing compliance processes – Licensees should implement effective policies and procedures to ensure they are meeting their compliance obligations. Licensees should consider assigning individuals to particular compliance responsibilities, establishing clear reporting lines and protocols within the business, and setting up reminders for key due dates (such as levy payments, reporting obligations, AFCA membership and PI insurance renewals). These processes should be clearly documented in a suite of compliance policies. Click here to find out how Sophie Grace can assist.

- Reviewing compliance processes – Licensees should undertake regular reviews of their compliance framework and assess their level of compliance. For example, licensees can hold quarterly or half-yearly compliance meetings with all key compliance personnel and responsible managers in attendance. Licensees should also look to breaches and complaints as a measure of compliance and possible systemic issues.

- Responding to regulator inquiries promptly and truthfully – Licensees must ensure that all correspondence received from regulators is attended to promptly. This means demonstrating allocating resources appropriately, responding within defined timeframes and with complete and accurate information. There are serious penalties for providing false or misleading information to a regulator. It is also important for licensees to keep their contact details up to date with various regulators to ensure no correspondence is missed.

As a reminder, compliance obligations cannot be outsourced. While licensees can seek assistance from external service providers, responsibility for complying with obligations remains with the licensee.

Further Reading

AFSL:

- Corporations Act 2001(Cth) – sections 915B and 915C

- ASIC cancels AFS licences of two Australian financial services providers for failure to pay industry funding levies

- ASIC cancels AFS licence of Financial Services Group Australia and permanently bans its responsible manager

- ASIC cancels AFS licence of Pulse Markets for serious and sustained breaches of duties

- ASIC Enforcement Action – Inactivity following change of control

Australian Credit Licence:

- National Consumer Credit Protection Act 2009 (Cth) – sections 54 and 55

- ASIC cancels seven Australian credit licences and suspends one Australian credit licence

- ASIC cancels Australian credit licence of Lendflex Holdings Pty Ltd

- ASIC bans Sydney mortgage broker for ten years and cancels her Australian credit licence

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]