- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Insurance industries

ASIC's enforcement priorities for 2023 focused on greenwashing, predatory lending, and interrupting investment scams. ASIC resources, both human and financial, were focused on these issues.

As we move into the new year it is important that Licensees keep in mind the 2023 enforcement priorities as ASIC is likely to continue to take enforcement action in these areas in addition to the 2024 enforcement priorities.

For 2023, ASIC's enforcement priorities were:

- Cyber and operational resilience

- Enforcement action targeting poor design, pricing and distribution of financial products

- Misleading conduct in relation to sustainable finance, including greenwashing

- Misconduct involving high risk products including crypto assets

- Combating and disrupting investment scams, with a focus on crypto assets and scams and other high-risk products

- Protecting financially vulnerable consumers, especially in relation to predatory lending or high-cost credit

- Misleading and deceptive conduct relating to investment products

- Misconduct in the superannuation sector

- Failures by providers of general insurance, particularly in relation to delivering on price promises

- Misconduct that involves misinformation through social media Governance and director's duties failures, with a focus on property schemes

- Manipulation in energy and commodities derivatives markets

- Unfair contract terms

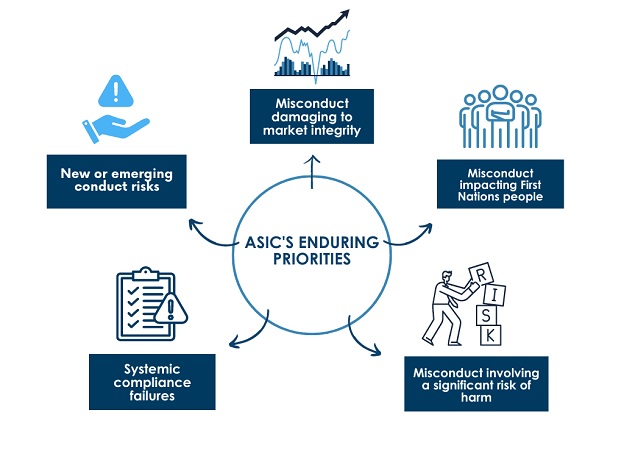

These priorities are underpinned by ASIC's enduring priorities, which underpin and guide the focus areas from year to year. The 5 enduring priorities are:

- Misconduct damaging to market integrity including insider trading, continuous disclosure failures, market manipulation, and breaches of director duties

- Misconduct impacting First Nations people

- Misconduct involving a high risk of significant consumer harm, particularly conduct targeting financially vulnerable consumers, addressing false and misleading advertising

- Systemic compliance failures by large financial institutions resulting in widespread consumer harm including fostering industry compliance

- New or emerging conduct risks within the financial system

Enforcement Action

ASIC's 2023 enforcement priorities aligned with ASIC's enforcement and regulatory action throughout 2022:

| July to December 2022 | January to March 2023 | |

|---|---|---|

| Criminal Charges Laid | 73 | 125 |

| Civil Penalties imposed by Courts | $76.3 million | $109.1 million |

| Investigations Commenced | 62 | 70 |

| Investigations Ongoing | 103 | 144 |

A summary of ASIC's enforcement outcomes can be viewed here.

What does this mean for licensees?

Licensees should take note of ASIC's enforcement priorities, particularly those in areas that overlap with operations and business strategy. One key area where we have seen ASIC take action is in relation to compliance with the Design and Distribution (DDO) regime.

ASIC has acted to place stop orders on a number of financial firms in response to deficiencies in their Target Market Determinations (TMDs). In the second half of 2022, ASIC issued 22 DDO stop orders.

Licensees that are required to comply with the DDO regime must ensure they:

- Have appropriate product governance arrangements in place;

- Update product governance arrangements on an ongoing basis, and in response to any significant dealings or complaints;

- Undertake proper consideration of the target market and the attributes of the product;

- Review and make any required amendments to TMDs;

- Ensure appropriate distribution of product, including by liaising closely with distributors to ensure significant dealings and complaints are appropriately responded to.

Misleading and deceptive conduct is also a key enforcement focus for ASIC. Whilst ASIC has specifically called credit, sustainable finance and superannuation products as important areas of focus, all licensees can take action to ensure they do not provide information or engage in conduct which is misleading or deceptive.

Important actions to mitigate this risk include:

- Reviewing marketing material prior to release against ASIC's good practice guidance in Regulatory Guide 234;

- Training representatives to ensure they understand the products and services the licensee is authorised to provide;

- Ensuring the risks and benefits of a product are appropriately and adequately disclosed to consumers;

- Ensure claims of sustainability or performance can be substantiated.

Further Reading

REP 757 ASIC enforcement and regulatory update: October to December 2022

Media Release (23-026MR): ASIC to expand enforcement focus areas in the coming year

DDO Enforcement – ASIC issue first DDO stop orders