Disney’s full buyout of Hulu in 2025 is a recent reminder of a broader pattern: Joint ventures (JVs) often begin as strategic solutions to shared opportunities — but unresolved commercial conflicts between shareholders can ultimately force fundamental restructuring or consolidation.

Commercial conflicts of interest are inherent to JVs. In many, the shareholders provide products or services to and share infrastructure with the JV, compete in markets directly adjacent to the JV, and have customers and contractors that overlap with the JV. This web of commercial relationships can give rise to numerous conflicts that — if left unchecked — can lead to suboptimal outcomes that are not in the best interests of the JV or its shareholders.

Case in point: Hulu, a multi-partner JV launched in 2007 that depended extensively on News Corporation, NBC, Disney, and later Time Warner to fill its library with premium streaming content that could compete with emerging digital platforms like YouTube and Netflix. The initial logic was compelling: Competitors could share technology costs, accelerate time-to-market, and have a single destination for high-quality content. At first, the venture succeeded because the partner’s interests were (temporarily) aligned around a common defensive objective. By 2010 the JV was profitable, second only to YouTube in streaming metrics, and considering a $2 billion IPO.

But Hulu’s success could not overcome the classic embedded conflicts of interest. Hulu needed a steady supply of low-cost, flexible, and broad content access, while parents wanted to maximize licensing fees and controls over their contributions — leading to a patchwork of restrictions that created a fragmented user experience and inconsistent availability. As the market matured, each partner began to pursue their own streaming strategies with different priorities and time horizons and began to fear Hulu would cannibalize their own networks or future streaming platforms. Strategic decisions that required unanimous approval became impossible, causing Hulu to continuously shift direction to manage partner infighting. Given a choice to invest in Hulu (shared upside, shared control) or their own platforms (full control, competitive differentiation), shareholders picked the latter. Within a decade, Hulu went from being a strategic asset to a strategic conflict, and Disney began a process of partner buyouts in 2019 that led to full ownership by 2025.

Dealmakers negotiating and structuring JVs are uniquely positioned to anticipate such conflicts of interest and proactively manage them. The purpose of this note is to help dealmakers identify — at the outset of the deal process — potential commercial conflicts that may arise post-deal close, and to provide examples of deal terms and policies that help manage conflicts in a way that promotes the long-term success of the JV.

Identifying Potential Conflicts

An initial step in addressing commercial conflicts is to identify and list the types of conflicts that JV board directors, management teams, and shareholder organizations will face post-close. Some potential conflicts are obvious, such as a decision by the JV to enter into a service or supply contract with one of the shareholders. Others are less obvious, such as a decision by a director to disclose to the JV knowledge of a business opportunity that could be attractive to either the shareholder or the JV.

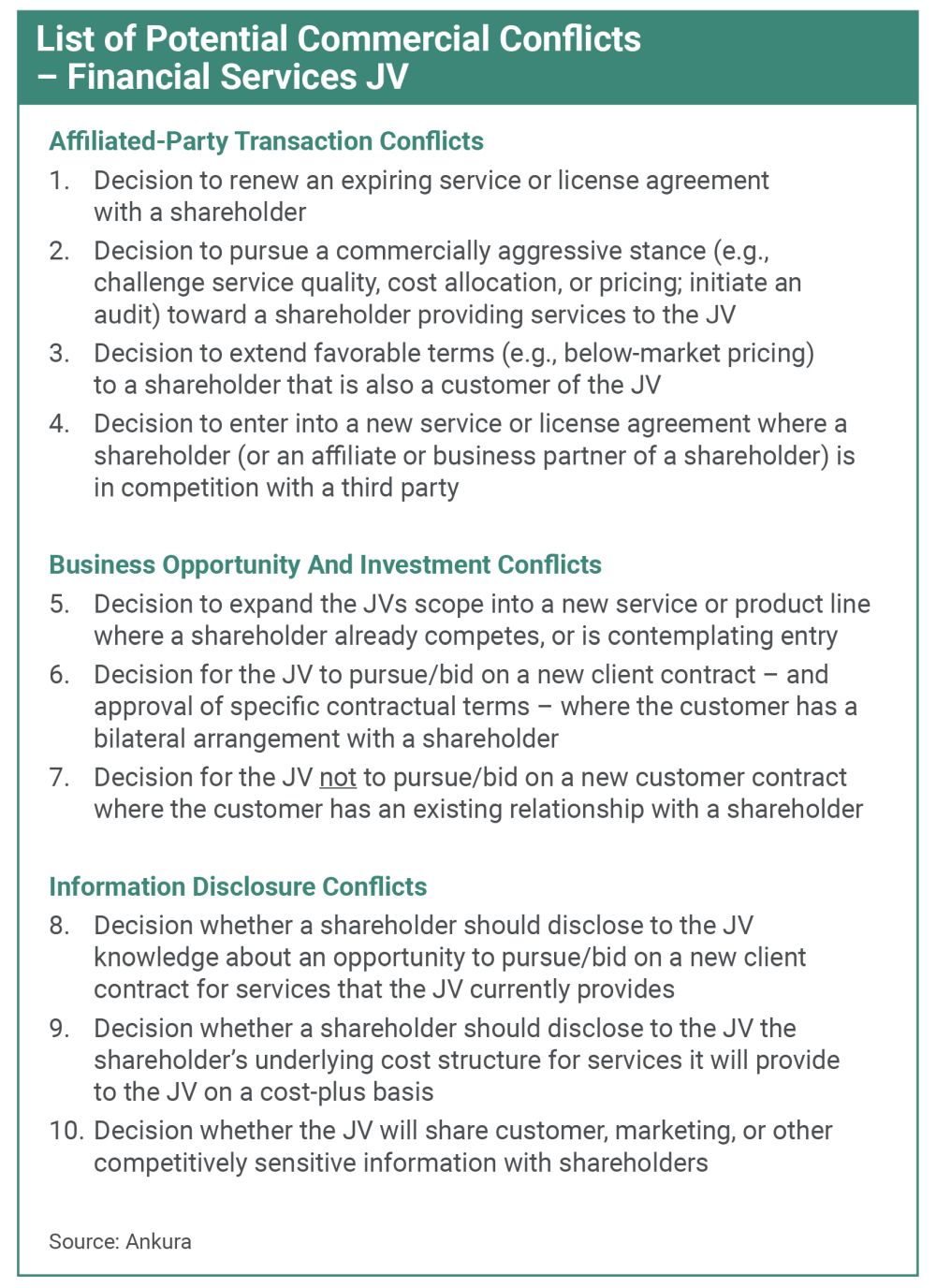

To illustrate the types of conflicts that a JV may face, consider a list of potential post-close commercial conflicts identified by the deal team in a fintech JV. The team organized commercial conflicts into three categories — affiliated-party conflicts, business opportunity and investment conflicts, and information disclosure conflicts — focusing on conflicts JV directors would confront (Exhibit 1).

Exhibit 1

The team then used this list as a starting point for considering deal terms and other approaches to mitigate the negative effects of these conflicts on the JV once operational.

These classes of conflict play out in different ways in JVs. For example, in a gas pipeline JV, a subset of the shareholders held upstream positions in gas fields that depended on the pipeline to bring their product to market. Because the financial returns from these upstream positions far exceeded those of operating the JV pipeline, the directors from these shareholders had an incentive to accelerate the schedule — rather than to minimize construction costs — of building the pipeline. This created a clear tension between promoting their individual shareholder’s interests, and the venture’s interests.

Or consider the situation of JV directors in a payments processing JV between two direct competitors. While the heart of the venture was to operate a payments processing platform for the shareholders, the JV also developed new products to meet its owners’ market needs. Directors sitting on the JV board, by virtue of the information they received or had the right to request, had the potential to reverse-engineer elements of the other shareholder’s market strategy, and then to use that to inform their own company’s plans in the market.

Anticipating these sorts of conflicts — and finding creative ways to address them through deal structures, contractual terms, or operating policies – is the role of the dealmaker.

Addressing Conflicts in Deal Terms and Policies

In drafting deal terms to help minimize conflicts, dealmakers need to balance three key considerations: promoting and protecting the JV’s interests, promoting and protecting the shareholders’ interests, and meeting JV director fiduciary duties and avoiding liability.

The JV’s shareholders should all have strong interests in avoiding JV director liability arising from alleged breaches of fiduciary duties.1 Shareholders may diverge, however, in where they fall in terms of the need to promote the JV’s interests versus their own. Certainly, protecting the shareholders’ interests will always be important to dealmakers when structuring a JV. But promoting the JV’s interests may also take on critical importance, particularly when (1) given the industry, market, or importance of the JV to the shareholders’ overall success, it makes business sense to give the JV room to grow; and (2) the JV partner has more commercial conflicts than does your company (e.g., your partner will be providing more services to the JV, competes in adjacent markets, or shares assets with the JV).

In our experience advising JVs and their shareholders before, during, and after JV launch, we have found that managing commercial conflicts by promoting the JV’s interests — with a focus on the following four areas — can significantly impact the short- and long-term value of a JV to its shareholders.

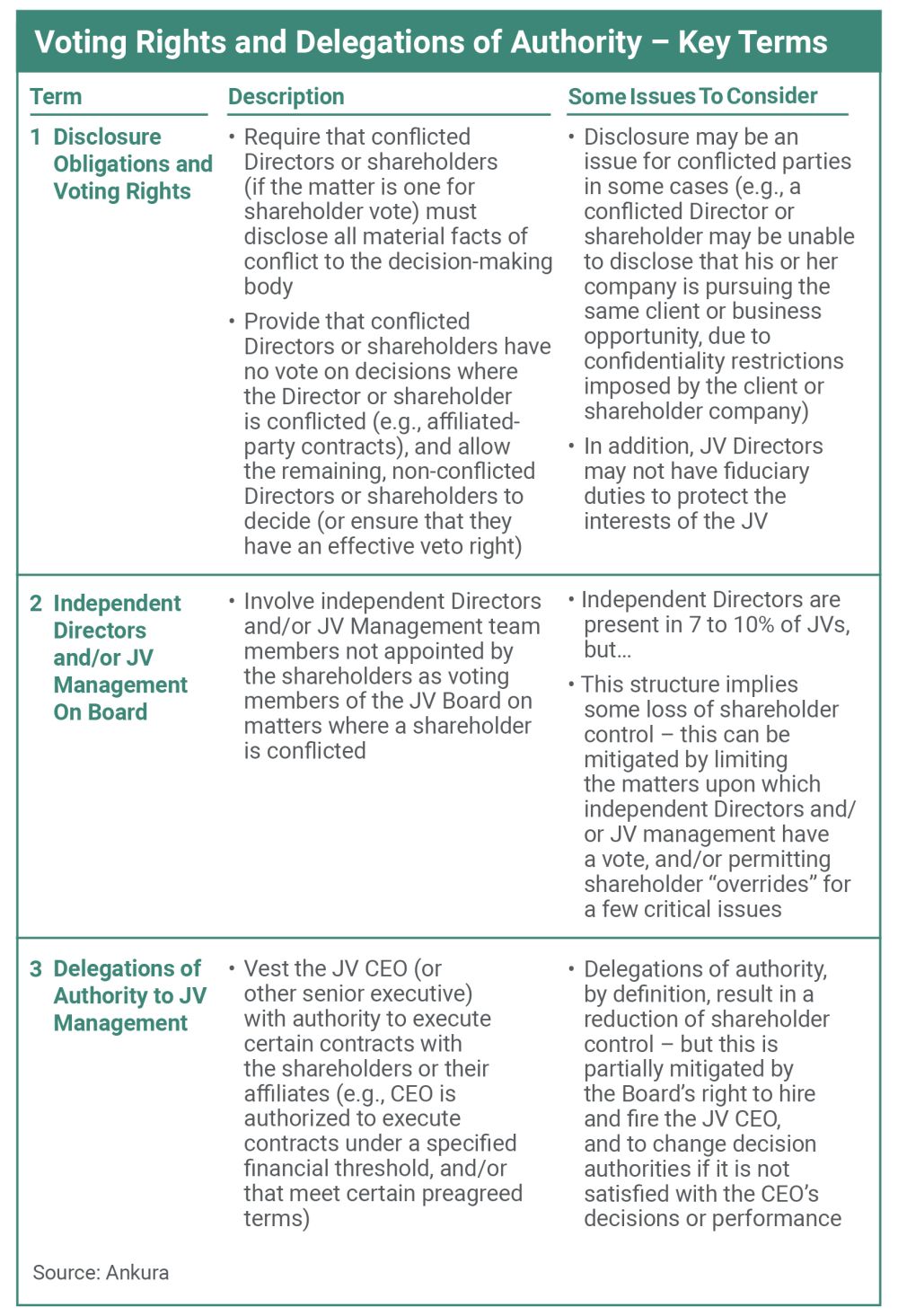

Voting Rights and Delegations of Authority. In many cases, voting rights and delegations of authority can help manage situations where shareholders are commercially conflicted, particularly where a shareholder is contracting with the JV. Example approaches include disclosure obligations prior to a vote, requiring conflicted directors to recuse themselves, appointing independent directors or management team members to the board, delegating matters to management, or carving out certain matters from the board and placing them in the hands of the shareholder companies (Exhibit 2).

Exhibit 2

For example, the dealmakers in one liquefied natural gas (lng) JV had the foresight to establish a number of terms that reduced commercial conflicts and helped to promote the success of the JV. They established an independent director position, delegated a number of key commercial decisions to management, and created a commercial committee composed of shareholder representatives not on the board to negotiate commercial issues.

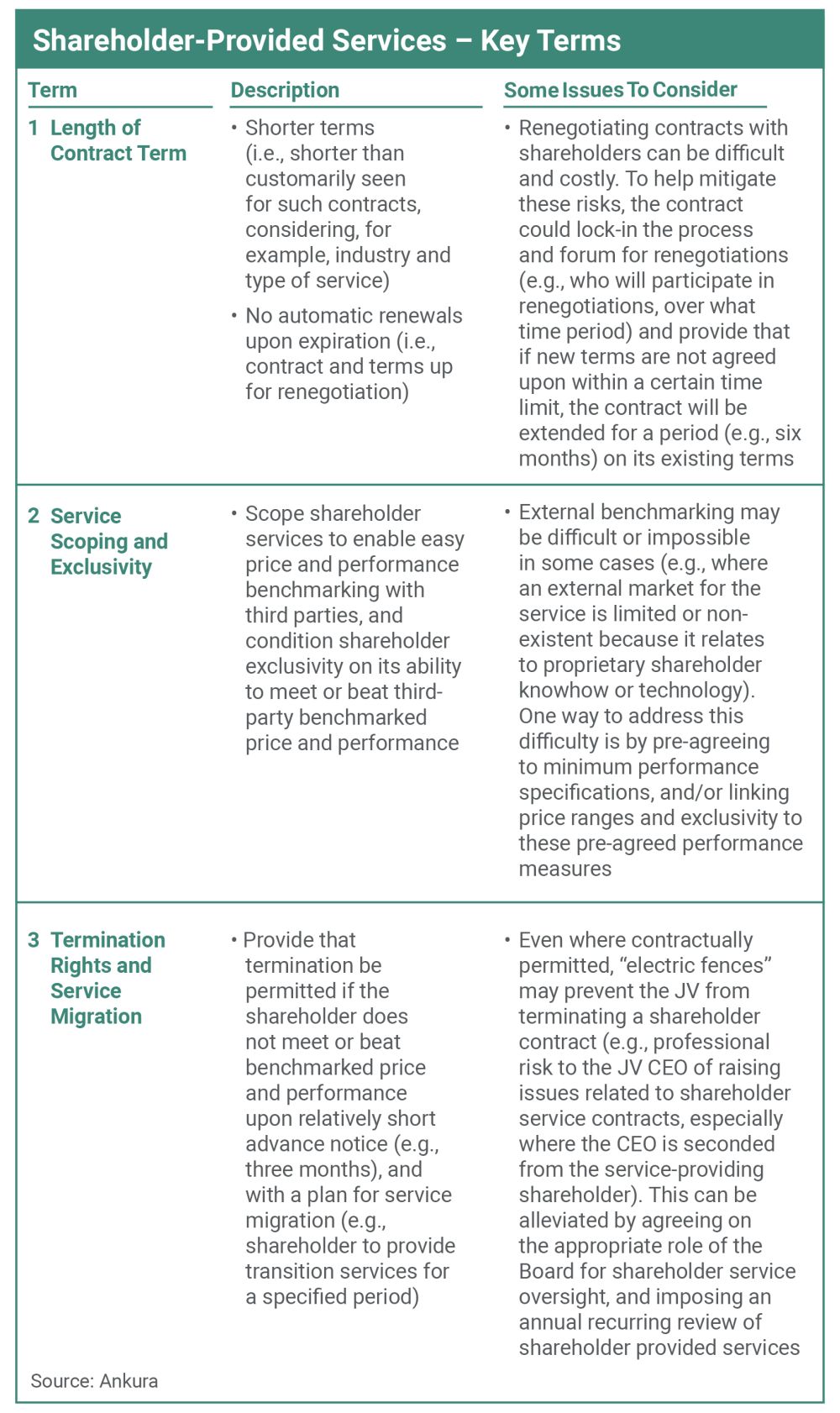

Shareholder-Provided Service Terms. JVs regularly depend on their shareholders to provide technical, administrative, and other services to help build or run the venture. Typically, the pricing and other commercial terms associated with such services are referenced in the JV agreement and detailed further in a master service agreement (MSA) and individual service-level agreements. Any changes to these terms, or entry into new shareholder service contracts, will usually require approval of the JV board, and potentially the shareholders.

While shareholder-provided services can be highly beneficial to a JV (e.g., to access specialized skills, reduce costs, and leverage shareholders’ scale), they are also fraught with conflicts. We have found such agreements often put JV CEOs in the uncomfortable position of directly or indirectly negotiating with their shareholders, and by extension, with members of their board. For example, a JV CEO trying to manage costs or improve performance may seek to renegotiate or terminate shareholder service contracts or challenge the quality of delivery. This can be politically dangerous. Listen to the words of one JV CEO:

“A few of my Board members, including the Chair of the Remuneration Committee, clearly don’t appreciate it when I try to squeeze their organizations for better terms or delivery on services. In fact, I have been pulled aside after Board meetings, and told by a Director that I should never raise these issues in the Board – that they are a matter between management and the shareholder.”

To help manage these conflicts, dealmakers should look closely at key service-related terms, including those related to contract length, service scoping and exclusivity, pricing mechanisms, reporting obligations and audit rights, termination rights, and service migration (Exhibit 3). For example, dealmakers might consider shorter terms on shareholder services, with no automatic renewals upon expiration — a practice that puts more power and flexibility into the hands of the JV CEO to evaluate where activities are optimally performed. Dealmakers might also consider scoping shareholder services to enable easy price and performance benchmarking with third-party providers — a practice that makes it easier for JV management to argue for better terms from a shareholder, or to switch service providers.

Exhibit 3

While the above addresses terms for shareholder-provided services, dealmakers may need to consider other types of contracts with shareholders, including supply agreements, offtake agreements, and licensing agreements. A number of the terms illustrated could also be applicable to those types of agreements, modified appropriately.

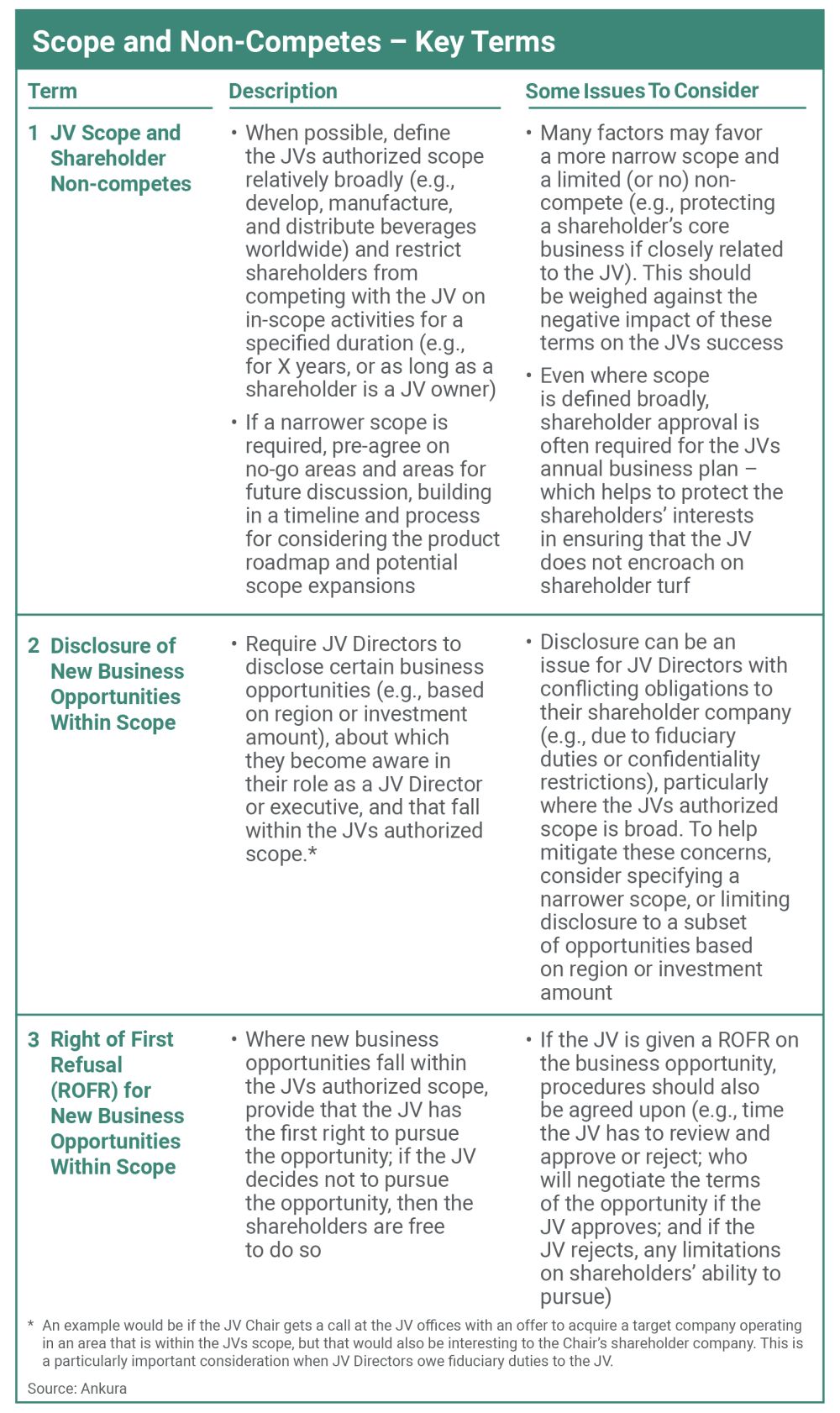

Authorized Scope and Non-Competes. Whether and how a venture and its shareholders may compete with each is another area rife with potential conflict.

Exhibit 4

Take the case of one technology commercialization JV where the JV agreement permitted the business to expand its initial authorized scope to pursue “reasonable and attractive opportunities in the same or adjacent technology or markets,” subject to board approval. But the JV agreement was silent on what should occur if one of its shareholders was pursuing the same opportunity. In the absence of guidance, JV directors were left to manage the balancing act in the face of an actual conflict.

Dealmakers can help their future JV directors by specifying upfront just how such conflicts should be handled. Examples of terms and policies to help manage such conflicts and promote the long-term success of the JV include those related to venture authorized scope, venture and shareholder non-competes, disclosure requirements regarding new business opportunities within scope, and right of first refusal for new business opportunities within scope (Exhibit 4).

Information-Sharing Terms and Protocols. Sharing information can be an issue for shareholders when they are contracting with the JV, or when considering investments or new business opportunities that fall within the scope of the JV’s business. In such cases, JV decision makers will want to know as much about a conflict as possible prior to making a decision, while the conflicted party may not want, or be able, to provide such information.

One way to handle this issue is to specify in the JV agreement the disclosures required to be made by a conflicted shareholder, and any exceptions to the requirement. For example, where a shareholder is providing services to the JV, the service-providing shareholder could be required to disclose specified cost information to the venture prior to entering into the contract, unless the services are at market price.

Information sharing can also raise antitrust problems for the venture and its shareholders, especially the problem of collusion (either between the JV and its shareholders, or among the shareholders). This is particularly true where the shareholders of the venture are also competitors of each other. To mitigate against antitrust risk, JVs can adopt policies on sharing competitively sensitive information with shareholders and others. Such policies may include guidance regarding what constitutes competitively sensitive information, participation by seconded personnel in internal shareholder meetings, ring-fencing of information, etc.

The product of a marriage between parties with often-competing commercial interests and goals, is that JVs are, by definition, conflicted. Managing these competing interests is a balancing act potentially fraught with peril. But by anticipating and providing guidance for resolving commercial conflicts at the outset, dealmakers can help ensure that the right balance is ultimately achieved.

Footnote

1 Your legal counsel can recommend ways to mitigate potential JV director liability for breaches of fiduciary duties to the JV, which may include modifying or eliminating JV director fiduciary duties to the JV.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]