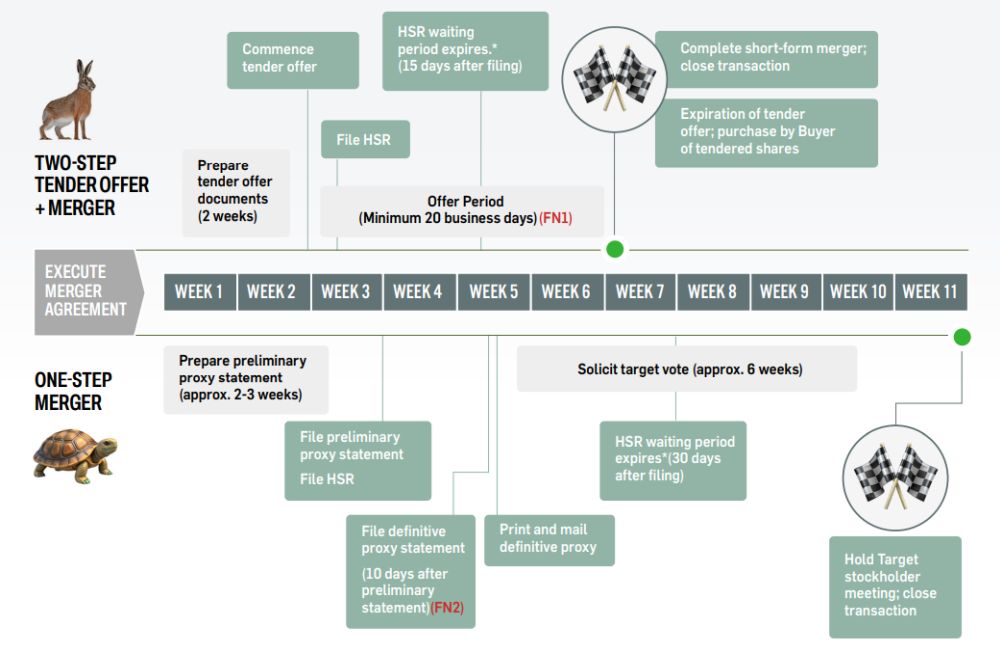

A two-step structure can be faster, but does slow and steady win the race?

- A take-private is typically structured as (1) a one-step merger involving the target and typically, a newly-formed merger subsidiary of the buyer or (2) a two-step merger, consisting of a tender offer by the buyer for all outstanding shares of the target, followed by a short-form merger that does not require stockholder approval.

- Under a two-step structure, lenders may not be comfortable financing at the consummation of the tender offer for shares of a target that is not a Delaware corporation, if less than 100% of the shares are tendered. A one-step structure ensures 100% ownership at the time of financing.

- A two-step structure should be avoided if a lengthy regulatory process is anticipated, as the tender offer cannot be consummated until required regulatory approvals have been obtained.

- As a result, a one-step structure may be preferred in the event of a lengthy regulatory process.

Footnotes

* Assumes HSR filing is made 3 weeks after signing and clearance is obtained after minimum waiting period

1. Assumes no SEC comments. If the SEC reviews, the timeline could be extended by 1-2 weeks, depending on the nature of SEC review

2. Assumes no SEC comments. If the SEC reviews, the timeline could be extended by 6-7 weeks, depending on the nature of SEC review

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.