- in European Union

- in European Union

- within Insurance, Privacy and Wealth Management topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- with readers working within the Accounting & Consultancy, Consumer Industries and Technology industries

Welcome to the May 2024 edition of Plugged In! This month, we delve into the nuanced developments shaping the future of EVs, from strategic challenges to investment trends.

Our exclusive interview with industry expert Mike Robinet offers insights into critical issues facing the EV supply chain. Robinet explores the challenges lurking beneath the surface, as the transition from internal combustion engine (ICE) to battery electric vehicle (BEV) production presents unique challenges for suppliers, from stranded capital to labor availability. He offers a rare glimpse into the profound impact on smaller suppliers navigating this monumental shift. Explore the intricate web of issues surrounding labor availability, cost, and the looming specter of underutilized facilities. Gain invaluable perspectives on the seismic shifts in manufacturing cadence and the implications for suppliers in this dynamic landscape. Robinet's candid discourse opens the door to a deeper understanding of the multifaceted challenges and opportunities driving the EV revolution.

Matt Miller, a contributing author from Cascade Partners, offers an update on investments and market activities in the EV space. Miller delves into the growing pains facing the EV market, including affordability hurdles, range anxiety, and charging infrastructure limitations. Uncover how industry giants like Honda and Toyota are doubling down on their commitment to an electric future with billion-dollar investments. Explore the shifting dynamics of EV funding and mergers & acquisitions, shedding light on key trends and cautionary notes. Miller's exploration also reveals crucial insights into government regulations, supply chain challenges, and the imperative for innovation in battery technology and charging infrastructure.

Finally, in his recurring column that addresses the latest developments and articles in EV, Bob Weiss explores the fascinating world of autonomous driving. Discover how the industry is addressing fierce competition from China.

As we navigate the complexities of the EV landscape, one thing is clear: the journey toward electrification is as much about overcoming challenges as it is about seizing opportunities. With strategic investments, innovative partnerships, and a steadfast commitment to sustainability, we're driving toward a future powered by electric possibilities.

Interview with Mike Robinet of S&P Global

Question 1

Bob: Mike, thanks so much for visiting with me this morning. There is so much going on in the EV space, and you have such a breadth of knowledge and experience that it is hard to know where to begin. Why don't we start with your views of a couple of subjects relating to the EV transition that, in your opinion, aren't getting the attention in the media that you think they deserve?

Mike: I believe that there are three subjects that are somewhat interrelated that will have an extraordinary impact on all levels of the supply chain, with particular impact on smaller Tier 1 and Tier 2 suppliers that are not getting enough attention and focus: (1) what I call "stranded capital," (2) challenge of the wind-down of ICE production by those suppliers transitioning to BEV, and (3) availability and cost of labor.

Question 2

Bob: Ok, let's start with number 1. What do you mean by "stranded capital"?

Mike: One of the by-products of the transition, with serious consequences, will be suppliers and OEMs experiencing higher levels of capacity underutilization. The build structure for ICE vehicles and BEV vehicles is very different. Today, the vast majority of manufacturing facilities are building ICE vehicles. There are very few plants that are configured or equipped to produce both ICE and BEV vehicles. Consequently, there are huge bets that are being made at the OEM and supplier levels regarding the rates of adoption of EVs. Accordingly, no matter what ultimately will be the rate of adoption, there is going to be a significant amount of what I would call "stranded capital," i.e., capital that was invested in either ICE or BEV facilities that will not be generating revenue based on market conditions. With stranded capital comes pressure to find some way to obtain a return. For example, if you have invested in a BEV facility and there are fewer programs being launched due to a slowdown in adoption, you will be tempted to take business at a lower margin to utilize capacity and obtain some return on scarce capital. This issue should continue over the next 6 or 7 years. With interest rates elevated and sources of financing becoming more discriminating, there will be a critical need to become more focused on efficient use of scarce capital.

Question 3

Bob: What companies will be most impacted by this conundrum?

Mike: Many of the OEMs have deep pockets and have likely planned for the fact that in this uncertain environment, with many variables impacting on the rate of adoption, they are going to have an underutilized BEV plant or ICE plant and will work that into their financial equation.

I am more concerned about the smaller suppliers. I would worry about the smaller suppliers that are taking a risk on navigating the transition from being an ICE supplier to a BEV supplier, which is a capital-intensive process and fraught with many variables and uncertainties. For example, they could take the approach that I used to be in the ICE world, I'm starting to abandon that world and I'm going over to the BEV world, but until the transition is complete, I am straddling both worlds. But the situation they face is I've got these ICE programs where the launches are delayed, while on the BEV side the timeline for BEV production is extended. ICE extension and BEV delays, and the combination of those is like kryptonite to the supply community.

When the supplier decided to transition, they were expecting that a certain footprint at their plant was going to be utilized. They were expecting a certain ramp-up, including a certain amount of revenue and margin that was going to come out of that footprint. They have people hired, capital invested, you get the general idea, all devoted to the new type of vehicles. And then the OEM taps you on the shoulder and says, oh, by the way, I'm delaying this launch by a year. It's like, whoa. I'm ready to go now and have already started transitioning out of the old ICE business.

So now it leaves some pretty significant holes in some businesses for a lot of suppliers. A larger organizations may have more wiggle room. The delay is going to be a pain, but not insurmountable. But I worry about smaller Tier 1's, Tier 2's that are focused on these programs. And it becomes a significant issue.

I think smaller tier ones and tier twos are the most impacted and the impact is potentially very significant. For example, the OEM has a program to build 250,000 units a year for 2 years. The supplier is awarded the program and makes the capital investment, including building a new facility, purchasing specialized equipment and tooling, and obtaining engineering talent to meet the requirements of the contract. The OEM then advises that the program is going to be delayed by 18 months.

How does the supplier get compensated for the cost of capital and carrying costs for the plant and equipment resulting from the delay? This will be an especially acute problem for suppliers with less than robust balance sheets and more limited access to financing.

Question 4

Bob: Is this really a new problem? The industry has always had problems with forecasting timing and estimating volume.

Mike: That's true. I have been in this industry for 35 years. There have always been delays and missed volume estimates; but the problem I am describing is massive, three or four times the magnitude of the historical problem. I think the impact will begin to be felt late this year and into next year.

Question 5

Bob: Let's discuss the second issue you mentioned – the challenge of working down ICE production while transitioning to BEV.

Mike: In an uncertain timeline for adoption, as BEV sales pick up and ICE sales decline, ICE manufacturers margins will decline over time. As the life of those programs are extended, the supplier is faced with declining margins, added costs (new tooling and perhaps replacement equipment) and underutilization of facilities. The suppliers of necessity will need aggressive price relief to justify the extension of production of a dying product. The supplier is going to have significant leverage, and addressing this problem will disrupt existing OEM/supplier relations and likely be costly to the OEMs.

Question 6

Bob: Now to the third issue – labor availability and cost.

Mike: There is often a significant issue of labor availability at the BEV plant location. If you want to add a third shift in a plant in the middle of Indiana and you are the biggest employer in this tiny town, there may not be an adequate available labor pool to staff that third shift. You can try the next town, but there is likely a major local manufacturer dealing with the same problem. In all events, it is a probable increase to the cost of labor to attract those scarce employees.

Frankly, the only way to avoid increased labor costs is to outsource or add more automation. But as you well know, every time we add automation we increase the capital investment, which brings us back to the issue we discussed earlier regarding availability of capital and adequate return on capital investment. Bank financing is now at 7, 8, and 9%, so you have to be smart about how you add/allocate capital and the resultant payback.

Question 7

Bob: How does the UAW's recent success in the South unionizing the VW plant impact on this issue?

Mike: It will definitely impact labor costs. The UAW will probably next target Mercedes, and then the VW and Mercedes' respective supply bases serving those plants. It is sort of a hub-and-spoke strategy.

Question 8

Bob: It is my understanding that manufacturers were attracted to locate in the South for two primary reasons: (1) non-union labor, and (2) abundant inexpensive energy.

Now that the UAW is making inroads and data centers are competing for energy resources, is that a failed strategy?

Mike: You raise a good point. Availability of adequate energy is a problem in a number of regions. The enormous demands for electricity by battery manufacturing plants is due to the fact that these batteries, as they are assembled, need to be charged. So in addition to the normal demand of a manufacturing plant for energy to support the manufacturing process, you have this significant supplemental demand. Frankly, anecdotally, I am told that some energy suppliers have welcomed the delay in EV adoption to give them time to attempt to deal with this problem.

Question 9

Bob: In what way will the different technology and configuration of the BEV impact suppliers?

Mike: There will be rapid advances in battery technology, with OEMs pursuing multiple paths dependent on the resiliency of mineral supply chains, such as lithium, graphite, nickel, etc. They are hedging their bets. As the technology evolves, certain technologies will be adopted and others rejected. Changing battery technology is not as complicated as in the ICE space.

So in the ICE world, if you had a new engine, you'd have to repackage that engine into the vehicle, you'd have to recrash test it, you'd have to do all the nonsense of making sure that you know that the weight dynamics are right and it is crashworthy , and all of that stuff. Just going though that process was extremely expensive. But now you've got a BEV with a battery box and they basically say, here's your battery box. We really don't care what you fill it up with. You can fill it up with water, but as long as it drives the vehicle, we don't care.

So, whether you put in a lithium, or nickel combination, or an NCM combination, what they call it, or maybe a LFP-type combination, they really don't care.

Also, there is going to be a secular change in the industry as we go from ICE to BEV.

The cadence being we were used to five or six-year programs. You know, here's the T 1 XX pick-up truck, you know, five or six years later, we probably should expect something where they're going to put some new engines in it, maybe lighten it up, do some other things, maybe change the dimensions a little bit, you get a general idea. And the whole industry is built on this five and six-year cycle mentality. If we're in the middle of the cycle, maybe we'll do a front-end refresh. Maybe we'll put a new IP in there to make it look good, whatever, but they would have an all-new, mid-cycle enhancement and then a major or another all-new redesign 5 to 6 years later.

But now, in the BEV world, as they develop these, for lack of a better word, skateboards, it's a lot more flexible. And now you don't have to worry about where the engine is in terms of where your wheels are because there's a lot more flexibility with engines, the motors, and all a lot smaller.

So you can change the wheelbase, you change the track a lot easier with these platforms. And so, with all that being said, it's more the "top hat" (upper body structure) that changes more often, at least from a structural perspective, vs. the skateboard (lower body structure) underneath. And so, it's a mindset difference that both the industry and the suppliers have to work with. This whole idea that, hey, I'm going have this program for five years, and then I'll requote on the program. I've got suppliers that have been told that you've got this program for eight years, and you better find a way to make money on this thing for eight years. We've got you for eight years, and then we'll start talking about what we do about changing the structure or redesigning or other major changes.

So, the cadence is a lot different. It's actually faster. The bottom structure is slower or at least longer. But for the top hat, the cadence will be faster, and I think a lot of suppliers are used to, hey, you know, you'll knock on my door 3 years before SOP, and then we'll go through this dance for six months and that all gets sourced and then I'll have two and a half years to get all my tooling and all my stuff in order. Those days are gone. Everything is so much more swift. I also think you're going to have more recalls because there's going to be kind of "shrapnel" along the way, and stuff's not going to get addressed like you should have because of the altered cadence.

Question 10

Bob: What about tooling?

Mike: Most automotive tooling capacity has moved offshore, which results in a competitive disadvantage. The speed of the industry means that you just can't make a tooling modification in let's say China and once completed it takes 6 weeks to arrive in the US and once it arrives the OEM says now we need a crease here , a dimension change etc. I think that the fact that we have lost our tooling mojo from a capacity and capability perspective is a big problem. Tooling used to rule this industry and was the backbone of getting stuff out the door. As we continue to utilize tooling manufacturing in Asia especially and other places overseas, it puts in danger our ability to react more quickly to market changes because we just don't have the capacity.

Question 11

Bob: Although this is a highly charged topic, let's take a leap and talk politics for a few minutes. Do you believe that who wins the presidential election in November will have a material impact on the trajectory and timing of the transition from ICE to BEV?

Mike: There is a lethargy and reluctance to make decisions waiting on November. I believe the die has been cast and no matter who the next president will be, the transition will continue for a variety of reasons. First, there has been enormous investment by the public and private sector. Much of these funds have already been invested, facilities constructed or in the process of construction, employees hired, R&D progressing, etc., and a good amount in red states. There would be enormous pushback if these investments don't achieve a return. Second, the president has limited authority and would need a compliant Congress to effect real change. Finally, the worldwide auto industry is not standing still and is moving aggressively to transition to EVs by perfecting manufacturing techniques, developing supply chains, increasing quality, and reducing costs. If the US wishes to remain competitive, it has no choice but to proceed on the course of transition. If not, China and Europe will dominate. In sum, in my opinion, if Biden wins, he will continue down his chosen path. If Trump wins, the time and aggressiveness will change and there may be some easing of regulations mandating change and reduction in investment, but the transition will continue. The real purpose of the IRA was to allow the US industry to begin the process of catching up to the Chinese. That was really the point of the IRA, and fundamentally, there are few people who disagree with that objective. In summary, I think the China factor and the extreme difficulty of turning around the titanic in mid-ocean will make it impossible to reverse course. If Trump is elected the momentum may slow, but the trajectory will remain the same.

Question 12

Bob: Any thoughts about China?

Mike: First, China is already here from a supply perspective. China will find a way to penetrate the sales market as well. Not a question of if, but when. Don't rely on government initiatives or tariffs to keep them out of the market. You have to find a way to become more efficient, increase productivity, and deliver quality products using state-of-the-art technology.

I would note that the threat to European manufacturers in their home markets is far worse than to US manufacturers selling in the US. European manufacturers have to deal with a high-cost manufacturing environment, restrictive labor rules, high energy costs, a slow growth economy and high regulatory structure not only relating to emissions, but sustainability, as well. In addition, the IRA local content requirement further impacts their export options.

Question 13

Bob: Intersection between AI and EV technology. Any thoughts?

Mike: Although I am not an expert in the area, I think AI will have its greatest impact on manufacturing. It will allow companies to identify and correct manufacturing problems more quickly and efficiently. It can also detect trends and allow us to react to them more quickly and effectively.

It will also have a significant impact on the development of autonomous driving in that it will have a role in making autonomous driving safer. The OEMs are going to be spending most of their time and effort on level 2 and maybe broaching slightly into level 3. They are going to want to find ways to make the vehicles safer to get the government off their back.

Let's just find a way to make sure these things don't crash into one another, and that will keep the government at bay. I really think that that's what level 2 is all about. It also makes it more convenient for the customer to drive it , but you know, saving the driver from themselves is really what level 2 is.

In my opinion, I think the more that AI helps bring that along and alters the software and figures out how you drive as a driver and modifies to that and kind of anticipates how you stop and how you accelerate and how you turn and all that kind of thing. I think that is definitely going to have a benefit going forward, but it's mostly a manufacturing play in the automotive industry, in my opinion.

Question 14

Bob: What is your view regarding the viability of startups and staying power of Tesla?

Mike: It's a different world in the startup space and, particularly, regarding EVs that are so custom. As we discussed, this is a capital-intensive industry. For the startup, there are no economies of scale and fierce competition from the legacy manufacturers, who may move more slowly, but have greater experience, expertise and resources. So, I think a couple of them are going to do okay, especially those backed by sovereign funds; but there is definitely going to be a lot of roadside collateral.

Regarding Tesla, it is going to survive. It had the market all to itself for a long time and was able to capture the high-end early adopters in a mostly competitor-free environment. Its challenge now is to compete in a highly competitive environment and at the lower end of the price range.

Closing Comment

Bob: Mike, thanks so much for taking the time to share your insights with me and our readers. I have learned a lot and thoroughly enjoyed our discussion. I hope we will have the opportunity to do this again in the near future.

Michael Robinet is the Consulting Executive Director at S&P Global. He has more than 37 years of experience in automotive market analysis, forecasting and supplier strategy functions. Mike joined S&P Global (formerly IHS Markit/IHS Automotive/CSM Worldwide) in 1996. As consulting executive director, he is a valued source for forecasts, commercial transition strategies and market dynamics.

Prior to his time at IHS Markit/S&P Global, Michael was a forecaster with two other automotive research houses as well as being active in finance at a major tier 1. Starting in 1996, Michael grew the CSM Worldwide forecast from a handful of clients to be the preeminent global production forecast utilized today. In 2011, he shifted his focus to consulting – driving market strategies for a shifting automotive ecosystem. Key career milestones include contributions to the 2009 Chrysler and GM bankruptcy agreements in Canada, innovations in both measuring vehicle production capacity and ongoing supply base strategies surrounding ICE to BEV transitions.

As EVs Experience Growing Pains,

Investors and Buyers Shift Gears

The growth in electric vehicles (EVs) adoption has shown remarkable progress, but recently, there are signs of slowing. As the EV market matures, early adopters have already made their purchases. The challenge now lies in appealing to a broader consumer base with varying preferences and needs.

Cost remains a significant barrier. Although automakers are working to reduce EV prices, affordability remains a challenge. Additionally, concerns about limited driving range and insufficient charging infrastructure impact consumer confidence.

Regardless, OEMs redoubled their commitment to an electric future during the last three months. Honda Motor announced plans to invest $11.0 billion in Canada to strengthen its North American EV supply chain, including an assembly and battery plant in Alliston, Ontario, as well as a battery cathode joint venture. Toyota disclosed a $1.3 billion investment at its flagship Kentucky facility for future electrification efforts, including the assembly of an all-new, three-row battery electric SUV for the US market and the addition of a battery pack assembly line.

Investors Focus on Bigger Battery and Charging Opportunities

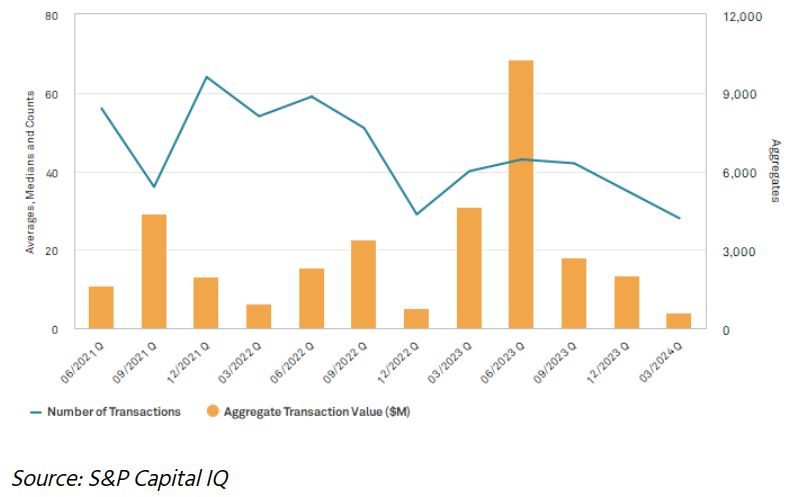

During the trailing twelve months (TTM) ended March 2024, 148 EV-related rounds of funding were announced or completed in the United States and Canada, a 17% downshift from the 179 transactions during the TTM ended March 2023. However, disclosed aggregate transaction value grew to $15.6B during the TTM ended March 2024 from $11.1B during the TTM ended March 2023, which was driven by the outsized quarter ended June 2023.

Some of the biggest rounds of funding completed during the six months ended March 2024 were investments in charging infrastructure and domestic battery materials and recycling.

- Northleaf Capital Partners agreed to acquire a controlling stake in EVPassport, an EV charging company based in Los Angeles. Northleaf also committed $200 million to accelerate the build-out of EV charging systems.

- United States Strategic Metals, a producer of cobalt and nickel and a domestic supplier of battery metals for electric vehicles and lithium-ion batteries to the clean energy transition sector, raised $120 million of non-convertible debt.

- Ascend Elements, a provider of sustainable, closed-loop battery materials solutions from EV battery recycling to production of lithium-ion battery precursor (pCAM) and cathode active materials (CAM), raised $162 million in a Series D funding round.

Chart: Rounds of Funding Announced and Completed in the United States and Canada

Source: S&P Capital IQ

Financial and Strategic Buyers Remain Cautious

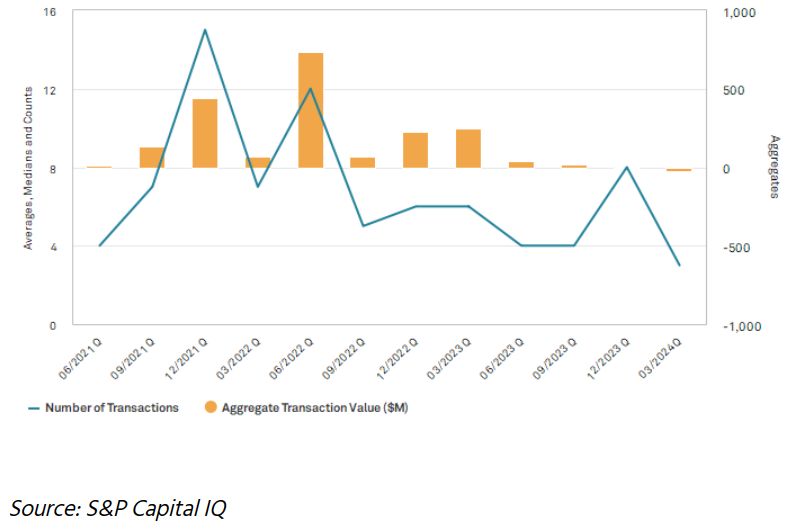

Only 19 EV-related M&A transactions were announced or completed in the United States and Canada during the TTM ended March 2024, a 34% U-turn from the 29 transactions during the TTM ended March 2023. The disclosed aggregate transaction value plummeted to $0.03B during the TTM, ended March 2024, from $1.3B during the TTM, ended March 2023.

Again, batteries and charging infrastructure were common themes. Notable transactions during the six months ended March 2024 included Komatsu America Corp.'s acquisition of American Battery Solutions, Salt Creek Capital's acquisition of Vantage Vehicle International, and Webasto's divestiture of Webasto Charging Solutions to Transom Capital Group. The transaction value was not disclosed for any of these deals.

Chart: M&A Announced and Completed in the United States and Canada

Source: S&P Capital IQ

Keep On Trucking

Government regulations and incentives will continue to create opportunities in the EV industry. To thrive, participants need to offer more low-priced EVs and solve the charging problem. Similarly, governments and industry alike are strongly inclined to nearshore to derisk supply chains and control intellectual property.

- According to McKinsey & Company, the North American supply chain for cathode and anode materials, electrolytes, and separators will be worth more than $35 billion annually but will require investments totaling $25 billion to build out.

- Global announced recycling capacity is more than three times the estimated supply of batteries in 2030; however, the International Energy Agency expects EV battery retirement to grow rapidly during the second half of the 2030s, which would require more capacity.

- To reach EV deployment levels in the Announced Pledges Scenario, public charging needs to increase sixfold by 2035. Moreover, as more electric buses and heavy-duty trucks hit the road, dedicated and flexible charging will be needed.

So, look for more investments, transactions, and partnerships in battery technology and materials and charging infrastructure, as well as electric commercial vehicles (eCVs), supply chain optimization, and emerging EV players.

Matthew Miller is a managing director at Cascade Partners. He has more than 30 years of experience in business development, corporate finance, and mergers & acquisitions, including buy- and sell-side advice for privately held and public traded businesses. Mr. Miller earned his BGS from the University of Michigan and MBA in finance from Loyola University of Chicago, holds the Series 63 and Series 79 securities licenses, and is currently an active member of the Association for Corporate Growth.

Cascade Partners is a boutique investment banking and restructuring firm headquartered in Detroit. Services include buy- and sell-side M&A advice, debt and equity capital raises, and financial and operational turnaround consulting. Cascade Partners serves clients in a variety of industries across the manufacturing, distribution, and services sectors, especially industries like automotive, healthcare, metals, and plastics.

In Case You Missed It

This issue of In Case You Missed It focuses on autonomous driving, its intersection with competition from China, and the arguably extraordinary approaches being proposed to attempt to level the playing field when competing with Chinese manufacturers.

Self-Driving Car Startup Wayve Raises More than $1 Billion from Investors Including SoftBank, Nvidia

Although the subject of autonomous driving has recently taken a somewhat proverbial back seat to EV specific subjects (e.g. slowdown in sales, charging infrastructure, China competition etc.), it would appear that investing in autonomous driving is alive and well. In an article appearing in the May 7, 2024 edition of the Wall Street Journal entitled, "Self-Driving Car Startup Wayve Raises More than $1 Billion from Investors Including SoftBank, Nvidia", the authors discuss Wayve Technologies recent successful series C round of in excess of $1 billion fundraising. Wayve Technologies specializes in the development of AI applications for autonomous driving. Nvidia and Microsoft are significant investors in Wayve.

https://www.wsj.com/business/autos/wayve-raises-more-than-1-billion-led-by-softbank-group-28d0cba8

China's Electric Cars Keep Improving, A Worry for Rivals Elsewhere

In an article appearing in the May 1 edition of the New York Times, the author sums up the premise of his article as follows: "Automakers in China are building a new generation of bigger, more technologically advanced and competitive electric cars, threatening to leap further ahead of their global rivals as they step up exports around the world." The author further notes that China is moving ahead aggressively with the technology and regulations for self-driving cars. China is eager to push the development of self-driving vehicles as it progresses to provide better technology in its electric vehicles. The article also discusses design and engineering developments being implemented by Chinese manufacturers.

https://www.nytimes.com/2024/05/01/business/china-electric-vehicles.html

When Every Car is Made in China

In the May 7 edition of The Dunne Insights Newsletter, Michael Dunne warns the reader to brace "...for the ultimate global automotive disruption." The author notes not only the increasing export of Chinese brands, but says that is only part of the story. The greater danger is global automakers "...racing to make China the epicenter for global automotive production."

https://newsletter.dunneinsights.com/p/when-every-car-is-made-in-china

Auto Execs Call for New Measures as EV Wars Heat Up

It appears that as described in the above article, China's lead in the race for EV sales dominance is not lost on the legacy OEMs. In an article appearing in the April 1st edition of the New York Times, entitled "Auto Execs Call for New Measures as EV Wars Heat Up", the authors discuss the out-of-the-box proposal by Renault's CEO to form an Airbus type alliance of European manufacturers to pool resources on battery and semiconductor research and production. Luca de Meo, Renault's CEO is quoted as saying that, "The prosperity of Europe is at stake". The EU's auto sector employs 13 million people and generates 8 percent of the bloc's GDP. Patrick Hummel, a UBS auto analyst is quoted as saying, "Chinese EV Makers have a structural cost advantage of 25 percent".

Biden to Quadruple Tariffs on Chinese EVs

Finally, as evidence of the extraordinary threat to the US automotive industry posed by Chinese EV imports, comes the report of the Biden administration's preparing to announce a major increase in tariffs on Chinese manufactured EVs. In an article entitled, "Biden to Quadruple Tariffs on Chinese EVs", appearing in the May 10, 2024 edition of the Wall Street Journal, the authors report that the Biden administration is preparing to announce the quadrupling of the existing tariff on Chinese imports of EVs (and critical minerals and batteries) from 25% to 100%.

Responding to the report, a spokesperson for the Chinese foreign ministry stated, "China will take all necessary means to defend its rights and interests". If the increase of the Tariffs are instituted, it will represent a major escalation of the trade war with China, with intended and perhaps unintended consequences for both nations.

All views presented in this newsletter are those of the authors and do not necessarily reflect the views of Dickinson Wright.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]