- within International Law topic(s)

- in United States

- within Technology, Strategy and Energy and Natural Resources topic(s)

Tariffs are inherently controversial because of their financial consequences. An importer wants to pay as little duty as possible while Customs (CBP) wants to collect as much tariff revenue as possible. The one constant in this battle between industry and government is the Harmonized Tariff Schedule (HTS). Because the HTS classification assigned to an imported article or commodity determines the duty rate, the classification is the fulcrum of this financial seesaw.

A smart importer constantly looks for ways to minimize customs duties just as it would try to minimize any other cost of doing business. This proactive search for opportunities to legitimately reduce duty liability has a name: tariff engineering (or TE). Tinkering with the design, timing, content, and order of the steps in a manufacturing process describes the traditional concept of TE, which addresses questions like: How much manufacturing should be done before importation as opposed to after importation? What ingredients can we include in our witch's brew recipe, and in what quantities? What if we configure our product into a different shape or weight, or otherwise tweak its physical characteristics such that we change the essential character? How does principal use factor into our analysis (if at all)? These are the types of questions relevant to a traditional TE analysis. But since TE is a term of art that isn't limited by a statutory or regulatory definition, in this article we will expand TE to include pretty much any proactive business decision intended to legitimately reduce a duty liability. We will, for example, look at how we can tariff engineer a transaction rather than a physical product, or how TE can be used to inform significant strategic business decisions.

A company may require a lot of data and analysis before making strategic business decisions, but the impact of customs duties on those decisions is generally self-evident. For instance, it's easy to see that saving five percent on the price of a gizmo by outsourcing it from Country A may be a poor business decision if the duty rate turns out to be ten percent, but buying the same item from Country B—even without a price reduction—may be a smarter decision if the item qualifies for duty-free treatment under, let's say, a free trade agreement, or another preference program. These are the kinds of TE decisions in which a fully engaged trade compliance manager (TCM) can have a major positive impact on a company's bottom line. By making sure that his or her company accurately classifies its imported goods and that the applicable customs duties are incorporated into the supply chain "landed cost" structure, a TCM ensures that duty costs are looked at with a critical eye by the bean counters and the decision makers.

The Supreme Court established the legitimacy of tariff engineering

Tariff engineering was first deemed to be an acceptable practice in Merritt v. Welsh,1 an 1882 decision by the Supreme Court that described how an importer can minimize duties by configuring a product so that its condition at the time of import allows it to be classified under a provision that offers a lower duty rate. In Merritt the court pondered whether it was acceptable to add molasses to sugar to satisfy a color-based tariff provision subject to a lower duty rate, ruling that "so long as no deception is practiced, so long as the goods are truly invoiced and freely and honestly exposed to the officers of customs for their examination, no fraud is committed, therefore no penalty is incurred."

Since then, the lower courts have consistently relied upon the Merritt precedent and its legacy of likeminded decisions to rule that tariff engineering a product to minimize duties is permissible, as long as all representations made to the government are accurate, transparent, and complete (to the extent required by law)—and no attempt is made to defraud the government by "artifice or deceit." An example of an illegal artifice would be the creation of an artificial product—a product that exists only as a fiction to influence the classification—like the sugar syrup at issue in the Heartland By-Products case discussed a bit later.

Two notable decisions issued in the wake of Merritt—namely Worthington v. Robbins and United States v. Citroen2—firmly established the tenet that a product is classifiable based on its condition at the time of import.3 This tenet remains crucial to modern customs administration. A sampling of the many court decisions relying on this tenet includes Carrington Co. v. United States,4 a 1974 TSUS-related case in which the Court of Customs and Patent Appeals (CCPA) said "it is a well-established principle that classification of an imported article must rest upon its condition as imported." In 1987's Bantam Travelware, Division of Peter's Bag Corp. v. United States5 the Court of International Trade (CIT) looked at whether the addition of braided material to luggage was commercially significant enough to influence the TSUS classification. CBP claimed that the braiding was an improper attempt to avoid a quota by adding material to the luggage that otherwise wouldn't have been added. Although the court's decision (in CBP's favor) was strictly classification-based, and therefore didn't offer an opinion on the importer's motive or TE per se, the court noted:

[CBP] suggests that [Bantam] began to construct certain importations with braid in an effort to avoid quota restraints, and to benefit from lower duty rates on luggage in part of braid. In this regard, [CBP] notes that the incorporation of braided materials into the subject merchandise roughly coincided with the institution of the aforementioned quota [and] reveal [Bantam's] intent to employ only enough braid to obtain favorable tariff treatment.

In 1989 the Court of Appeals for the Federal Circuit (CAFC) reinforced the condition-as-imported principle in Simod America Corp. v. United States,6 noting that "imported merchandise is dutiable in its condition as imported, except in the instance ... of deception, disguise, or artifice resorted to for the purpose of perpetrating a fraud of the revenue; what is going to be done with it afterwards is not relevant." In 1992 the CIT reaffirmed an importer's right to tariff engineer a product in Tropicana Products, Inc. v. United States.7 The court recognized the "fundamental right of an importer to so fashion his goods as to obtain the lowest possible rate of duty, absent any fraud, deception or artifice concerning the condition of the goods."

The most recent significant TE case was Ford Motor Company v. United States.8 At issue were cargo vans—or were they really passenger vans?—that were the subject of an internal advice ruling, HQ H220856 (January 30, 2013). Evidently the vans were imported "with characteristics indicative of passenger vehicles, then converted for cargo use after importation." CBP at the port of Baltimore claimed "that the temporary presence of seats and windows at the moment of importation is not relevant to the use of the good and thus should not affect the classification of the vehicle, and that the addition of these transitory features represents a deliberate attempt at circumventing" a higher duty rate. HQ agreed. Ford sued, winning in the CIT but, in a blow to TE, losing when CBP appealed in the CAFC.

Tariff engineering in CBP rulings

CBP has addressed TE in many HTS binding rulings. In an internal advice ruling, HQ 963753 (July 25, 2000), CBP acknowledged TE as an accepted practice but noted that the "rough header lumber" under review wasn't modified to an extent that caused a change in the HTS classification:

As such, we are not disputing an importer's right to "tariff engineer" his merchandise such that it may be classified in a provision with a lower duty rate. We merely cannot approve of such "tariff engineering" when the modifications (or in this case, processing) made to that merchandise do not change the nature of the merchandise enough to give rise to an alternate and viable classification under the tariff.

In HQ 963876 (February 12, 2001), which discussed the classification of wood truss components in chapter 44, CBP advised that "Customs must classify the merchandise in question in its condition as imported. ... The courts are clear that goods may be imported at various stages of manufacturing or processing even if at an artificially interrupted point, to obtain lower rates of duty." CBP's reference to an "artificially interrupted" truss manufacturing process shouldn't be confused with the creation of an artificial product, a distinction at the heart of perhaps the most high-profile recent example of the inherent dangers faced by importers who pursue TE. The case involved sugar syrup imported by a Michigan company called Heartland By-Products. The pickle Heartland found itself in was that, although the physical nature of the imported syrup was accurately represented by Heartland in a ruling request to CBP, the CAFC ultimately ruled that the physical characteristics didn't represent a legitimate commercial mixture. In other words, the syrup, as imported, was in a condition that never would occur at any point in the course of normal manufacturing, but for an attempt to tariff engineer the syrup into a lower duty rate.

In HQ 964978 (April 18, 2002), the classification of women's slip-on shoes with outer soles of textile and rubber/plastics was discussed. CBP provided insightful contrast between the permissible TE of the shoes and the impermissible TE of the syrup in the Heartland By-Products case:

With a significant disparity in duty rates, it may be financially advantageous to import a shoe with an outer sole of textile materials as opposed to one of rubber or plastic material. It is clear that a thin layer of textile material has been attached which covers most of the rubber portion of the shoe, which rests under the ball of the foot. Accordingly, the fundamental issue in this case is whether or not the textile material that has been applied to the contact surface of the outer sole is permissible tariff engineering.

The concept of tariff engineering is based on the long-standing principles that merchandise is classifiable in its condition as imported and that an importer has the right to fashion merchandise to obtain the lowest rate of duty and the most favorable treatment. In U.S. v. Citroen, ... Justice Hughes pointed out that "although dutiable classification of articles imported must be ascertained by an examination of the imported article itself, in the condition in which it is imported [,] this, of course does not mean that a prescribed rate of duty can be escaped by resort to disguise or artifice." In the case at hand, then, a determination must be made as to whether or not the addition of a layer of textile material to the otherwise rubber/plastic sole is a disguise or artifice. The textile material is part of the merchandise as imported. The textile appears to have been glued to the sole of the shoe and is not easily removed. We find that the textile material is not an artifice or a disguise but rather a constituent material of the outer sole.

Recently in Heartland By-Products, Inc. v. United States, ... the Court upheld Customs' determination that adding molasses to raw sugar prior to importation in order to obtain a lower duty rate and to avoid quota restrictions was improper tariff engineering. The Court upheld Customs' revocation of a New York ruling letter in which the agency concluded that "the processing in this case is not legitimate tariff engineering. But rather, it is merely disguise or artifice intended to escape a higher rate of duty such as a quota tariff rate." ... In Heartland the molasses was added to the sugar to form a syrup prior to importation. Once imported the molasses was removed. After the molasses was removed, the sugar was used in the same manner as sugar subject to quota. In its condition as imported then, there was no commercial use for the syrup. ...

The facts in the instant case are significantly distinguishable from Heartland. The layer of textile material in the instant case is a part of the sole when it is imported. The textile slip-on shoe is sold in exactly the condition as imported. Unlike the facts in Heartland where the molasses was added prior to importation and then removed once imported, the textile covering on the sole of the shoe is not removed prior to its sale. Accordingly, we cannot conclude that the addition of the textile layer to the instant shoe presents a disguise or artifice.

Examples of tariff engineering opportunities

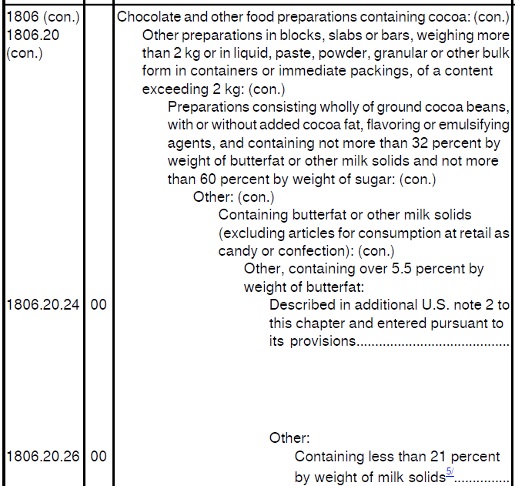

Some of today's HTS provisions include parameters that are better suited to TE than others—like many food, textile, or footwear provisions—because of explicit content requirements that can be used to configure a product to an importer's advantage. Look, for instance, at "Chocolate and other food preparations" under heading 1806:

As we work our way from the heading down through the subheadings, we find that subheading 1806.20.26 is subject to five discrete weight-content restrictions (2 kg, 32%, 60%, 5.5%, 21%). By adjusting the recipe, form, shape, and weight of its product, without artifice or deceit, a chocolate producer can import under a more tariffically advantageous HTS provision.

We can also tariff engineer a transaction rather than a physical product when pricing is a relevant classification factor, but this option comes with some potential risk under customs valuation rules and is available only for the handful of products classifiable under the HTS subheadings structured on the unit price of a product, with different duty rates assigned to each subheading. Sports footwear provides an excellent illustration of this. Certain sports footwear is classified under subheading 6402.19.50, which carries a compound duty rate of 76¢/pair + 32% when "valued over $3 but not over $6.50" per pair. But if the footwear is "valued over $6.50 but not over $12" per pair, the classification changes to 6402.19.70 and the duty rate is almost halved to 76¢/pair + 17%.

Let's say that Miranda, who is the TCM for a sports footwear importer, learns that Joe, one of the company's buyers, issued a purchase order to a shoemaker in Turkey for 50,000 pairs of shoes at $6.50 per pair. This order is projected to satisfy the company's needs for one year. Miranda learns that the shoemaker offers a discounted list price of $6.50 based on a standard volume discount freely given to any customer for any order of at least 40,000 pairs. And she learns that the standard list unit price is bumped up to $6.60 when fewer than 40,000 pairs are ordered. She also learns that Joe initially wanted to issue several purchase orders for smaller quantities, spread out over the year, but the discount offered on one large order seemed too good to pass up. Miranda understands that her job isn't necessarily to advocate for TE, but rather to identify regulatory or cost-saving opportunities that help her company's management make smart business decisions. With this mindset she schedules a meeting with Joe, senior operations and finance managers, and legal counsel to discuss the potential advantage—and risk—of placing two semi-annual orders, each for 25,000 pairs at the $6.60 unit price. She explains the advantage: based on a projected annual quantity of 50,000 pairs, the company would pay an extra $5,000 to the shoemaker, but by engineering a change in the HTS classification from subheading 6402.19.50 to 6402.19.70 the company would save almost $50,000 in duty. And by placing two orders per year rather than one, the company would enjoy the inherent advantages of carrying fewer shoes in inventory at any given time on its books and in its warehouse—tangible benefits unrelated to TE. But she also explains the risk: CBP may argue that splitting the order to obtain a lower duty rate is an illegal ploy intended to circumvent a tariff obligation, irrespective of the non-tariff advantages. Although a strong case be made that this is a legitimate activity based on smart business practices, Miranda advises that it would be wise to anticipate CBP's objections. She suggests that seeking a binding ruling from CBP would be a good idea, and everyone in the meeting agrees.

But not all transactional TE is controversial. Certain agricultural products, for instance, may be ripe for transactional TE based not on value but on import date. The HTS classification for some vegetables is designed to change with the calendar; in one example fresh cucumbers are dutiable under subheading 0707.00.50 at 5.6¢ per kilo if entered on November 30, but on December 1 the classification changes to 0707.00.20 resulting in a duty rate of only 4.2¢ per kilo. A competitive advantage is gained (presuming freshness and consumer safety aren't compromised) by delaying entry of a shipment of cucumbers until after midnight on December 1. A handful of other products are also subject to calendar-based tariff rates. As a possible method of TE this method offers practically no risk of adverse consequences from CBP.

A smart company will also consider TE (of a sort) in its infrastructure strategy. To illustrate this let's say that José is the TCM for a padlock manufacturer that currently operates two U.S. factories. One factory makes 3-inch cylinder-type padlocks (8301.10.90 at 4.2%), and the other makes 1-inch cylinder-type padlocks (8301.10.60 at 6.1%). Even though most sales for both versions are in the U.S. market, the company has decided to relocate one of these factories to a low-cost country. Regardless of which factory is offshored, the padlocks it produces will be imported into the U.S. under intercompany sale orders (and for simplicity we will presume the intercompany price is accepted by CBP). José's analysis, which also compares the duties paid on all the raw materials and parts brought into the U.S. against the duties applicable on similar imports into the low-cost country, concludes that almost $2M in customs duties will be saved each year if the large padlock factory is moved. All potential trade barriers and benefits must be considered. His tariff analysis may not be a game-changer when considered against all the other relocation decision factors, but as his company's TCM José has the obligation to bring this important information to the attention of management.

A 2011 decision by the CAFC, Dell Products LP v. United States,9 which affirmed the CIT's decision, suggests another possible way to tariff engineer a transaction, an option not limited by the tariff provisions themselves. Instead, the GRIs provided the means for the engineering. The crux of Dell's unsuccessful argument was that a laptop computer and a spare battery, sold separately but shipped together to an end-user in the same package, ought to qualify as a retail set under GRI 3(b). The Dell decisions give importers new insight into how to fashion a transaction so it satisfies the retail set requirements.

GRI 2(a) offers another way to employ the GRIs in a TE decision. Under GRI 2(a) a group of parts imported together are classified under the HTS provision of the higher-level assembly when the collective nature of the parts is sufficient to establish the essential character of the assembly. If the assembly carries, say, a duty rate of 10% but the effective aggregated duty rate of all the individual parts is only 7% when classified separately, then the importer might want to avoid the essential-character implications of GRI 2(a) by separately importing each of the parts (or groupings of parts).10

TE can also be applied to an importer's efforts to qualify a product under one of the many bilateral or multilateral free trade agreements (FTAs) negotiated by the U.S. FTAs have their own unique "rules of origin" that are fundamentally based on the comparison of the HTS classification used to import a finished good against the HTS classifications of the raw and semi-finished inputs used to produce that finished good. If the "tariff shift" specified in the applicable rule of origin is satisfied (along with, when applicable, the "regional value content" requirement), then the good qualifies to be imported at a free or reduced rate of duty, but ensuring that the product qualifies requires close collaboration with the producer or exporter, who must certify the FTA qualification. An importer with enough clout over its suppliers' supply chain decisions may induce sourcing or production changes that push an otherwise non-qualifying product over the qualification threshold. Also, a factory relocation decision can be impacted by whether a target country is an FTA partner with the U.S.

Antidumping and countervailing duties, as well as Section 232 and Section 301 duties, can be mitigated or eliminated with some proactive planning. As these duties are assessed against specific products from specific producers in specific countries, a conscientious TCM can conduct a review of the company's exposure (actual and, to the extent possible, forward-looking) and initiate internal discussions about potential sourcing options. It can be difficult to fully disentangle a company's supply chain from producers and countries saddled with 232/301 duties or hefty ADD/CVD margins, but it may be worth the effort.

TE is obviously a customs concept, but we can stretch the concept even further to include export activities. While the goal would not be to reduce duties, an exporter may gain a competitive advantage by engineering a product to fit under a less-restrictive ECCN. For example, a valve is largely controlled (licensable) based on the body material. The metal content of some alloys will cause a valve to fall under a highly controlled ECCN like 2B350 or 2A226, while the metal content of another valve will allow classification under a less restrictive ECCN like 2B999 or even EAR99. Import tariffs may not be affected, but an export license requirement may impose business risks and costs analogous to a tariff, so a customer in Singapore may appreciate the option of buying a product, made of a slightly different alloy (perhaps with a lower nickel content) but still perfectly suitable for the intended end-use, that can be delivered relatively more quickly because an export license (and subsequent reexport license) is not required.

Approach tariff engineering with caution

Tariff engineering is, as we've seen, a perfectly legitimate cost-saving practice as long as the product and the transaction are honestly described on the invoice and in any pre- or post-import representations made to CBP, and there's nothing ephemeral or artificial about the imported condition of the goods. Evaluating a company's business practices for TE opportunities may reveal a path to significant savings. Hence a TCM should always watch for TE opportunities when classifying as dutiable any product or component that presents a significant financial impact—and this can be especially impactful for a related transaction in which one company controls both ends of the transaction. TCMs may want to schedule meetings with selected managers to educate them on TE, so that they and their teams can also identify opportunities, but as the folks at Heartland By-Products discovered, a company's pursuit of a TE opportunity is like inviting a potentially dangerous stranger into your home, so extreme care must be taken. A TE opportunity that is poorly evaluated and executed can cost a company (like Heartland By-Products) far more than they expected to save. And TCMs must remember that TE is ultimately a business decision rather than a compliance decision, hence under no circumstances should the trade compliance department make the final decision about whether it's in their company's best interests to pursue a TE opportunity. Get the explicit advice and consent of internal legal counsel and the appropriate senior business leaders, and seek external legal guidance, when necessary. I can't stress this point enough. In the end, though, no matter how initially attractive a TE opportunity may seem to be, it may ultimately be determined that a TE opportunity is not worth the risk.

But if a TE opportunity is pursued, the who-what-when-and-why of the decision must be documented, preferably in a formal memo approved by all decision-makers. An importer is, of course, not obligated to explain its TE decisions unless CBP formally asks for an explanation (or unless an importer seeks the certainty of a binding ruling, the lessons of the Heartland By-Products debacle notwithstanding), but a smart importer presumes that sooner or later CBP will ask questions. When challenged, an importer must be prepared to defend its tariff engineering decisions.

Footnotes

1 Merritt v. Welsh, 104 U.S. 694 (1882).

2 Worthington v. Robbins, 139 U.S. 337 (1891) and United States v. Citroen, 223 U.S. 407 (1912).

3 ubsequent post-import use of the goods is typically irrelevant—unless goods are subject, for example, to a "principal use" or "actual use" provision.

4 Carrington Co. v. United States, 497 F.2d 902 (CCPA 1974).

5 Bantam Travelware, Division of Peter's Bag Corp. v. United States, 679 F. Supp. 8 (Ct. Int'l Trade 1987), affirmed without discussion in Bantam Travelware, Division of Peter's Bag Corp. v. United States, 858 F.2d 742 (Fed. Cir. 1988). Note that Bantam was represented by a future CIT judge, Judith Barzilay.

6 Simod America Corp. v. United States, 872 F.2d 1572 (Fed. Cir. 1989).

7 Tropicana Products, Inc. v. United States, 789 F. Supp. 1154 (Ct. Int'l Trade 1992).

8 Ford Motor Company v. United States, 254 F. Supp. 3d 1297 (Ct. Int'l Trade 2017), reversed by Ford Motor Company v. United States, 926 F.3d 741 (Fed. Cir. 2019).

9 Dell Products LP v. United States, 714 F. Supp. 2d 1252 (Ct. Int'l Trade 2010), affirmed by Dell Products LP v. United States, 642 F.3d 1055 (Fed. Cir. 2011).

10 In a response to questions raised by the WTO Appellate Body in a dispute with China over the interpretation of GRI 2(a), the United States' official answer noted that "if a manufacturer were to order all of the parts from one company and then, in order to obtain a lower duty, separate the parts into different containers and make separate entry of each shipment, the United States would not find it to circumvent [GRI 2(a)]. ... The United States does not investigate whether a manufacturer may be arranging multiple shipments in order to obtain lower duty payments, and does not consider such practice to constitute 'circumvention'". See AB-2008-10 (WT/DS339/R/Add. 1, WT/DS340/R/Add. 1, WT/DS342/R/Add. 1), 18 July 2008, A-254, -255.

Check out our new Digital Magazine Get the inside scoop on the Braumiller Law Group & Braumiller Consulting Group "peeps." Expertise in International Trade Compliance.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.