- within Criminal Law, Wealth Management and Intellectual Property topic(s)

Let's face it - the post-pandemic era has been good for many software companies as they have experienced rapid growth in response to higher demand for connectivity, flexibility, and scalability. Per our latest annual AlixPartners Disruption Index, growth has become one of the top priorities, particularly for software companies.

Unfortunately, disruption has remained the norm and as we continue into 2024, analysts are increasingly predicting a deceleration in growth rates across the board for software companies. Forecasts suggest that median revenue growth rate will drop from 16% last year to 11% this year, posing new challenges for software companies of all sizes. From a macroeconomic perspective, high interest rates and geopolitical uncertainties are leading customers to delay or reduce investments in enterprise software. Additionally, market saturation is increasing as many providers now offer similar solutions. Competition is getting intense in mature segments where technology has become widely adopted.

Last year, we had outlined a few specific levers in HBR for companies to drive top line in a down market. Since then, we have completed further analysis of the volatile market dynamics and developed an updated view on how software companies can drive growth in these turbulent conditions.

Understanding the software growth landscape

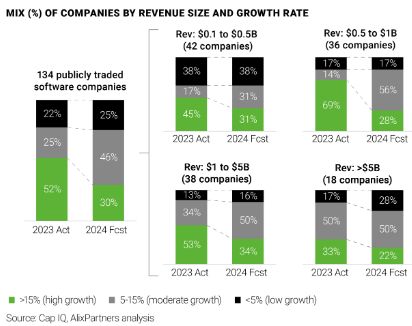

We analyzed 134 publicly traded software companies by comparing 2024 predictions against 2023 growth (Figure 1). While the mix of companies with 5% or higher growth will remain similar to 2023 levels (75% in 2024 vs. 78% in 2023), the mix of high-growth companies (15% or greater) is expected to decrease from 52% last year to 30% this year. Mid-size companies ($0.5-$1 billion in revenue) will be most impacted, as our analysis shows the percentage of high-growth companies in this segment will decline from 67% to 26%.

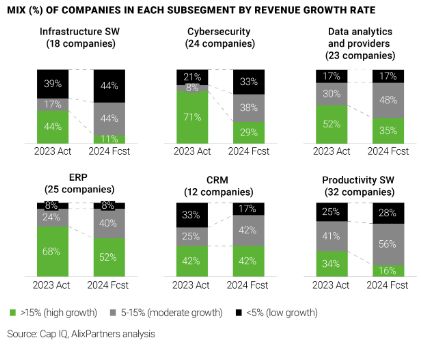

From our experience, growth rates and levers for top line expansion vary across software sub-segments. To determine the best approach for the software industry, we divided companies into six groups based on their operating models and go-to-market approaches, and then compared their 2023 growth rates against 2024 projected figures.

Figure 2 shows that the infrastructure software and cybersecurity sub-segments will see the biggest decline in percentage of high-growth companies, dropping from 44% to 11% and 71% to 29%, respectively. Meanwhile, the enterprise resource planning (ERP) and customer relationship management (CRM) sub-segments will maintain their momentum with a similar mix of companies hitting a 5% or higher growth rate this year versus last-customers here continue to invest, with a focus on improving core process efficiency through automation.

Key growth challenges in 2024

Here are some common operational challenges that companies must address in 2024 to drive growth:

- Challenging customer acquisition: Acquiring new customers will be challenging due to IT budget constraints and heightened competition, requiring innovative strategies to identify and convince buyers. As customers become more knowledgeable about competing products, CROs and CMOs need to strategically allocate marketing investments to generate meaningful leads.

- Increasing cost pressure to expand sales resources: Additional funding to increase sales team size will not be available in this budget-constrained environment. Instead, companies will need to improve go-to-market (GTM) effectiveness and explore creative ways to expand market coverage.

- Driving customer engagement while optimizing cost: As recurring revenue grows, a lack of proportionate investment in customer success and services can hinder the ability to drive customer adoption and consumption. This leads to a drop in customer satisfaction and renewal.

- Increasing price pressure: Given software price increases in the past year and increasing AI-based solutions requiring fewer seat-based licenses, industry players must evolve their pricing models (e.g., to usage-based) with a focus on demonstrating value to drive long-term growth.

Charting a course for growth

Over the past two years, software companies have emphasized normalizing cost structures after a pandemic-driven hyper-growth period. As market uncertainties persist, many remain cautious about capital allocation going into 2024 - which necessitates improving the productivity of existing investments to drive growth. Additionally, given advancements in AI and tech modernization, leaders across all software sub-segments must strategically prioritize targeted investments to enhance commercial functions.

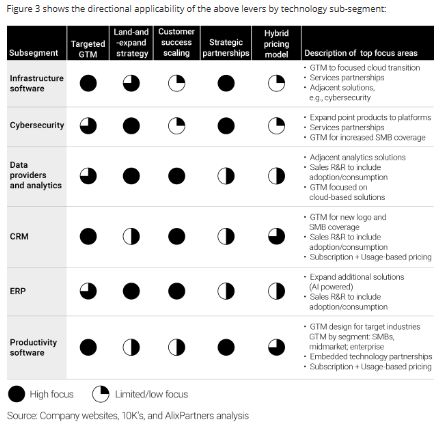

We evaluated successful strategies employed by high-growth companies across different sub-segments and noticed a few common levers., with varying degrees of emphasis by sub-segment. Based on the analysis, we outline five potential organic growth initiatives.

- Targeted GTM: In this budget-constrained environment, it is critical to focus sales and marketing efforts towards segments with a competitive advantage. This requires redefining customer segments using a data-driven approach and developing tailored GTM motions. For example, high-growth players such as HubSpot (CRM) and GitLab (productivity) are focused on growing small-and-medium business (SMB) market share through product-led growth and digital GTM. Similarly, many infrastructure software providers are undergoing cloud transformations requiring new segmentation and targeting. Employing AI-driven lead-scoring solutions can ensure a consistent pool of qualified leads, increasing sales capacity for the most important deals.

- Land-and-expand strategies: As acquisitions, software vendors need a land-and-expand strategy to secure initial foothold within the customer organizations. This starts with targeted sales efforts and then expands by upselling additional features to foster long-term relationships. For example, cybersecurity provider Palo Alto Networks is focused on expanding existing customer relationships with end-to-end security platforms. Similarly, ERP company ServiceNow is highly focused on a land-and-expand motions.

- Customer success focus: As recurring revenue increases, software companies need to incorporate customer success metrics into sales team incentives to drive customer adoption and consumption. This can provide necessary scale to cover additional recurring revenues while controlling investment levels in specialized customer success teams. Sub-segments that have mostly migrated to a SaaS model (e.g., ERP and data analytics providers) are in a better position to utilize this approach to scale customer success

- Strategic partnerships: Channel partners can provide a cost-effective method to reach target customers - our earlier whitepaper provides a list of focus areas by company size and growth rate. Vendors will need to first align their partner programs to new targeted GTM motions and incentivize desired behaviors such as new logo acquisition. In addition, they should develop a few ambitious strategic partnerships that include co-development, co-marketing, and co-selling models to drive accelerated growth. In our experience, strategic services partnerships can be valuable for infrastructure software and cybersecurity vendors, while technology and embedded partnerships can be beneficial for ERP, CRM, and productivity software companies.

- Hybrid pricing models: These allow flexibility by offering a combination of different pricing model tailored to diverse customer needs - for instance, subscription-based plans alongside usage-based pricing. In some cases, this approach may lead to temporary ARR (annual recurring revenue) decline, but by providing options that align with customers' budget constraints and usage patterns, vendors can enhance customer satisfaction and retention to drive revenue growth in the long run. We believe categories such as data providers and analytics, CRM, and productivity software would benefit most in the coming year from this approach.

Figure 3 shows the directional applicability of the above levers by technology sub-segment:

Conclusion

Despite the shifting landscape and decelerating growth, revenue remains a critical metric for software companies' enterprise value. By deploying targeted strategies centered around core value propositions, companies can navigate the challenges of 2024 while laying the groundwork for long-term success. Contact us to learn how you can tailor your strategy to drive growth.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.