- within Corporate/Commercial Law topic(s)

- in Asia

- within Corporate/Commercial Law topic(s)

- in Asia

INTRODUCTION

Welcome to the 19th survey of U.S. sponsor-backed going private transactions, prepared by Weil, Gotshal & Manges LLP. This survey analyzes certain key transaction terms and trends (and expected future trends) of sponsor-backed going private transactions of U.S. targets that signed in 2025 and that had an equity value of at least $100 million.

RESEARCH METHODOLOGY

We surveyed 35 sponsor-backed going private transactions involving the following U.S. target companies:

All dollar amounts and percentages referenced in this survey are approximate. Unless otherwise noted, such amounts and percentages are based on publicly available information about the surveyed transactions involving the targets listed above.

BEHIND THE SCENES WITH WEIL: A CLOSER LOOK AT THE DUN & BRADSTREET GOING PRIVATE TRANSACTION

On March 23, 2025, Dun & Bradstreet Holdings, Inc., represented by Weil, entered into a definitive agreement to be acquired by Clearlake Capital in a going private transaction valued at $7.7 billion, including outstanding debt.

In a testament to collaboration and teamwork across legal disciplines, the Weil team led negotiations to finalize the merger agreement on a highly compressed timeline. The transaction closed on August 26, 2025.

Below we include a few key deal points relating to this transaction, each of which is further discussed in the context of the other surveyed transactions in this study.

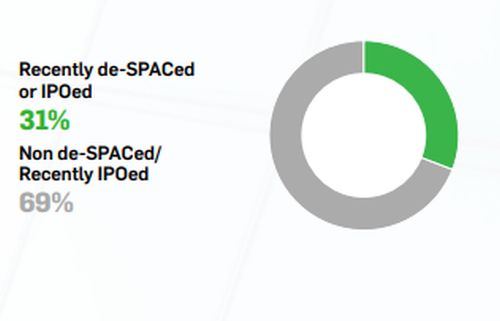

TARGET COMPANY RECENTLY de-SPACed OR IPOed

The Dun & Bradstreet transaction is one of eleven targets in the 2025 survey to have recently (i.e., in the last 5 years) gone public. In this case, Dun & Bradstreet went public via an IPO in 2020. Going private transactions involving recently IPOed targets (or targets that recently went public via a de-SPAC transaction) often involve unique process considerations (e.g., including whether to negotiate voting support agreements with any large minority stockholders and whether obtaining requisite stockholder approval is obtainable via written consent (a "sign-and-consent" structure)) often driven by the fact that these targets tend to have more concentrated ownership than companies that have been publicly traded for longer periods of time.

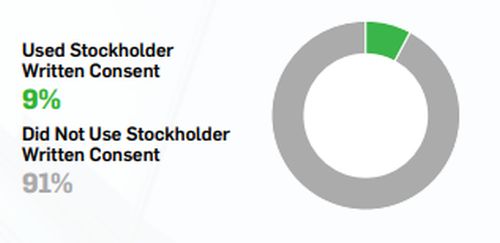

STOCKHOLDER WRITTEN CONSENT

Despite having a relatively concentrated stockholder base, the Dun & Bradstreet transaction did not use a sign-and-consent structure (where stockholder approval is obtained by written consent immediately following the signing of the merger agreement) and instead proceeded with obtaining the requisite stockholder vote through a traditional stockholder meeting (at which the requisite stockholder vote was obtained).

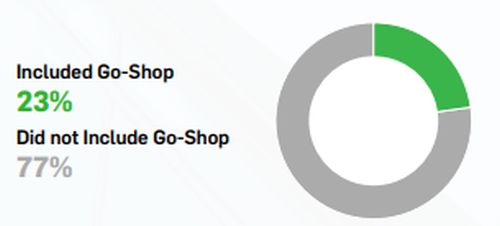

GO-SHOP

The Dun & Bradstreet transaction is one of eight transactions that included a go-shop period (in this case, a 30-day go-shop period, paired with a bifurcated termination fee structure).

BEHIND THE SCENES WITH WEIL: A CLOSER LOOK AT THE DUN & BRADSTREET GOING PRIVATE TRANSACTION

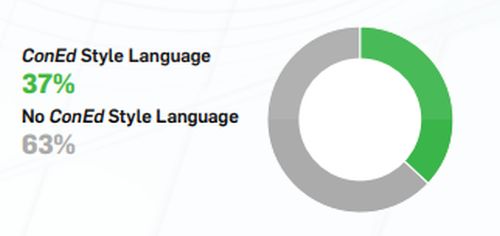

ConEd LANGUAGE

The Dun & Bradstreet merger agreement included ConEd-style lostpremium language, which preserves the ability of the target company to recover, on behalf of its stockholders, damages based on the lost premium if a buyer fails to close.

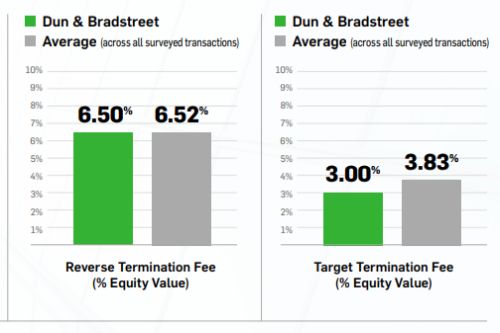

REVERSE / TARGET TERMINATION FEES

Both the reverse termination fee and target termination fee for the Dun & Bradstreet transaction, measured as percentages of equity value and enterprise value, generally were below the averages for the surveyed transactions. Larger deals often feature lower reverse termination fee percentages, since even a modest percentage may yield a significant absolute dollar amount generally sufficient to enhance deal certainty.

GENERAL MARKET OBSERVATIONS

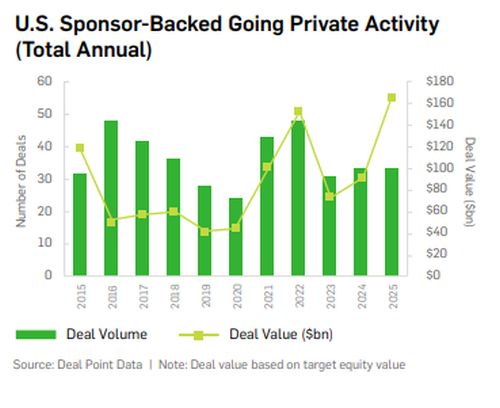

Following a robust 2024, sponsor-backed going private activity in 2025 held steady in terms of the numbers of deals announced, but skewed dramatically higher in aggregate deal value. While the deal count in our 2025 survey is the same as last year's (35), aggregate deal value increased by 90% in terms of total equity value. As discussed below, the increase in deal value was driven in part by several notable $10+ billion mega deals, rather than a broad-based increase in deal size across all transactions.

U.S. Sponsor-Backed Going Private Activity (Total Annual)

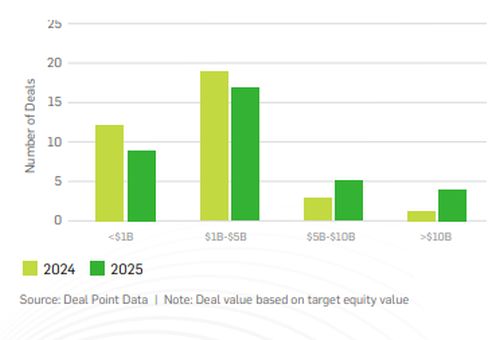

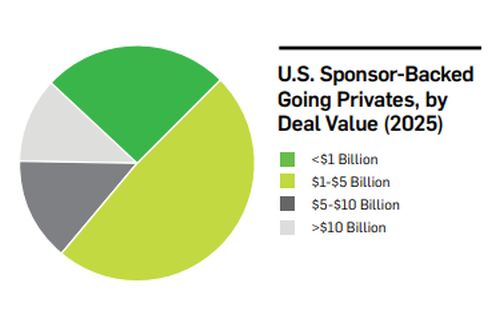

U.S. Sponsor-Backed Going Private Deal Value Concentration

By the Numbers. Building on a trend first highlighted in last year's survey, 2025 continued to exhibit an outsized concentration of sponsor-backed going private transactions at the top end of the market. Transactions with at least $1 billion of equity value again represented a significant share of overall deal activity, reinforcing the view that private equity sponsors continue to prioritize scale when considering public targets. Many sponsors view going private transactions as a primary avenue for deploying uninvested capital, especially in public companies that sit at the top end of the sponsor addressable market, where valuation dislocations have been more persistent. Large public companies with depressed market capitalizations present sponsors with the opportunity to deploy capital at scale. These opportunities have become increasingly prevalent as constraints on equity check size have eased, driven by larger fund sizes, the ticking time on investment periods, an increased appetite for Continuation Vehicle ("CV") transactions, more frequent use of club deals (fueled in part by sovereign wealth funds and other LPs looking to deploy large pools of capital) and a more accommodating debt financing environment.

Sector Concentration. Consistent with prior years, U.S. sponsor-backed going private activity in 2025 was concentrated in technology, with Software/Tech accounting for roughly one-third of the surveyed transactions. Business Services represented the second-highest number of deals at 14% of the surveyed transactions, reflecting continued sponsor interest in asset-light, cash-generative businesses with scalable operating models. Industrials, Retail, Consumer Goods and Real Estate Investment each represented 9% of the surveyed transactions, indicating a relatively even distribution of activity across several traditional sectors. Healthcare and Electricity/Utilities each accounted for 6% of deals, while IT Services comprised a smaller share at 3%. Overall, the data reflects a market skewed toward technology-enabled and services-based businesses, while still demonstrating broad sector participation across the U.S. sponsor-backed going private landscape.

To read this article in full, please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]