- within Employment and HR topic(s)

Note From the Editor

This year’s M&A Report offers a detailed review of the global M&A market, including an analysis of market activity across key geographies and industry sectors. We examine how easing interest rates, shifting macroeconomic conditions, and regulatory developments helped propel a worldwide recovery in 2025, led by growth in larger transactions valued at a billion dollars or more, and we analyze the factors shaping the market outlook for 2026.

We discuss a recent change in the tender offer rules and its potential impact on market practice generally, and public M&A in particular. And we take a closer look at common takeover defenses available to public companies and how market and investor pressures continue to influence governance practices.

We also review trends in VC-backed company M&A deal terms, examining how deal structures, indemnification practices, earnouts, and the use of representation and warranty insurance have evolved in recent years as companies and investors navigate a changing deal environment.

Please subscribe to our mailing lists to stay up to date on the latest developments related to M&A. And don’t forget to check out WilmerHale’s IPO Report and Venture Capital Report for additional insights.

Andrew Bonnes

PARTNER

Co-Chair, Mergers and Acquisitions Practice

Market Review and Outlook

2025 was a recovery year for M&A. The macroeconomic headwinds that have buffeted the market since 2022 started to subside, and total deal value increased significantly compared to 2024, surging toward the end of the year—particularly in the United States. These positive trends were not evenly distributed, however, and on closer inspection the picture was more complicated, with mixed storylines playing out in different sectors of the market throughout the year.

The year began with high levels of optimism, driven by expectations that a more business-friendly administration would restore confidence and unleash pent-up demand building since the end of the COVID-19 boom. Beginning in February 2025, however, the Trump administration unveiled a series of sweeping global tariff policies that introduced a fresh round of uncertainty. In the United States, Hart-Scott-Rodino filings—a good real-time indicator of M&A activity—dropped by 61% from February to March. Geopolitical and trade tensions amplified market volatility, while inflation remained stubbornly above the Federal Reserve’s 2% target. As a result, the dealmaking environment remained challenging. But as interest rates improved, credit markets stabilized, and businesses adapted to the new trade regime, deal activity accelerated in mid-2025.

This growth, however, was not felt across the entire market. Most buyers remained very selective, focusing on significant strategic acquisitions of premium targets. A perceived easing in antitrust enforcement may have also contributed to greater confidence at the top end of the market, and the second half of 2025 saw a surge in high- value transactions. Notable megadeals included multiple multi-billion-dollar transactions, such as the Netflix bid for Warner Bros. Discovery (now pending with Skydance/ Paramount as the buyer), Union Pacific’s merger with Norfolk Southern, and Electronic Arts’ $55 billion take- private buyout—each emblematic of renewed strategic confidence among corporate buyers.

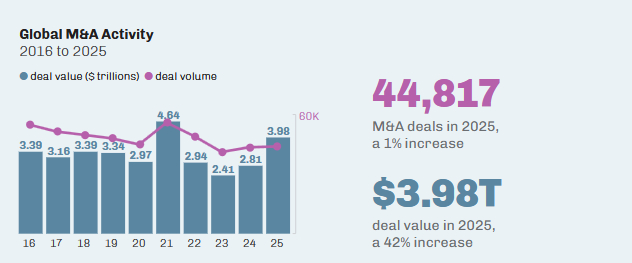

The growth in M&A deal value in 2025 was driven primarily by an increase in very large transactions, while overall transaction volume remained relatively flat. Global reported M&A deal value surged by 42%, from $2.81 trillion in 2024 to $3.98 trillion in 2025; by contrast, the number of reported M&A transactions worldwide increased by only 1%, from 44,379 deals to 44,817. Average deal size was $88.9 million in 2025, up 40% from $63.4 million in 2024.

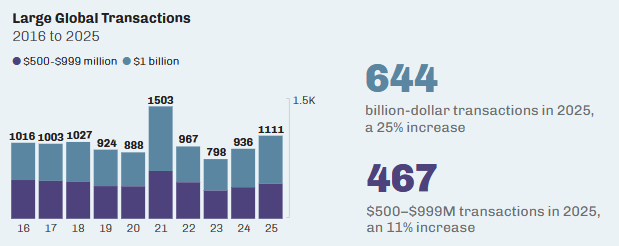

The number of billion-dollar transactions worldwide increased by 25%, from 514 in 2024 to 644 in 2025, while their total value increased by 61%, from $1.87 trillion to $3.00 trillion. Excluding billion-dollar transactions, total worldwide deal value increased by only 3% between 2024 and 2025, and the total value of deals under $500 million actually declined by a fraction of a percent.

The market dynamics in early 2026 feel eerily familiar. A strong start to the year, particularly at the top end of the market, once again ran into unexpected geopolitical headwinds during the first quarter. Hostilities between the United States and Iran have roiled global energy markets and threatened the stability of other sectors that are sensitive to the price of fuel, bringing fresh uncertainty to M&A decision-makers. Whether the market can again absorb these shocks and resume its growth trajectory remains an open—and central—question for 2026.

GEOGRAPHIC RESULTS

Deal volume and value were up across all major geographic regions in 2025, with deal volume increasing only modestly while valuations surged.

United States

Deal volume increased by 2%, from 17,963 transactions in 2024 to 18,330 in 2025. US deal value jumped by 55%, from $1.80 trillion to $2.80 trillion. Average deal size increased by 52%, from $100.5 million to $152.6 million. The number of billion-dollar transactions involving US companies jumped by 27%, from 341 in 2024 to 434 in 2025, while their total value increased by 68%, from $1.38 trillion to $2.32 trillion.

Europe

The number of transactions in Europe increased by less than 1%, from 16,390 in 2024 to 16,518 in 2025. Total deal value increased by 33%, from $943.3 billion to $1.26 trillion. Average deal size increased by 33%, from $57.6 million to $76.2 million. The number of billion-dollar transactions involving European companies increased by 24%, from 199 in 2024 to 245 in 2025, while their total value increased by 53%, from $621.5 billion to $950.2 billion.

Asia-Pacific

In the Asia-Pacific region, deal volume increased by 3%, from 11,631 transactions in 2024 to 11,937 in 2025. Total deal value in the region increased by 19%, from $798.0 billion to $948.0 billion, resulting in an average deal size that climbed 16%, from $68.6 million to $79.4 million. The number of billion-dollar transactions involving Asia-Pacific companies climbed by 13%, from 141 in 2024 to 160 in 2025, while their total value grew by 35%, from $451.6 billion to $608.6 billion.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]