Executive Directors, Richard Joynt and Amy Collins examine the correlation between a family office life cycle and a wealthy family's life cycle.

Having managed both single family and multi family offices for twenty years, and having worked with first, second, third and even seventh generation family members, we have observed that the particular needs of the family and their circumstances tend to dictate the complexity and shape of the family office.

The concept of a product having a life cycle was theorised in the mid-1960s by Raymond Vernon and has since passed into standard economic theory as one of the bedrocks of modern marketing. Our observation is that the family office also tends to follow a particular life cycle and this can be developed into a useful tool to assist private wealth practitioners understand how they can relate to, and complement, the services that a family office offers.

The stages of a wealthy family life cycle

Stage 1 - The Entrepreneurial Business Family

One or more members of the family have created a business which is still majority owned by the founders. The vast majority of the family's wealth is still tied up in the business and there is little liquid wealth. The founders spend most of their time working in the business to increase its value.

Stage 2 - The Wealthy Business Family

There have been one or more shareholder events creating liquid wealth for the family - this could be dividends from profits or a sale of a shareholding. The family still have a large stake in the business and the founders continue to spend a great deal of time working in that business.

Stage 3 - The Diversified Wealthy Family

The family are no longer the majority shareholder and driving force behind the business. The family's assets are in a variety of different assets and the head of the family usually sets the strategic investment plan. Often there will be new privately owned businesses in the portfolio of investments as this type of investment was the original source of the family's wealth. The head of the family may therefore see him or herself as a serial entrepreneur with a diversified wealth base.

Stage 4 - Pre-Transition Of Wealth

The head of the family is less active and seeks to enjoy the fruit of their labours as they become older. Wealth preservation is in the forefront of the mind of the founders and thoughts also turn to how this will be effectively transitioned to the next generation.

Stage 5 - Post-Transition Of Wealth

Generation 2 are now in possession of the wealth. They either decide to continue to invest their wealth together, as a family, or they decide to go their separate ways.

Stage 6 - Multi-Generational Family

If the family continue to invest their wealth communally they become a multi-generational wealthy family. At any point the different branches of the family can choose to go their separate ways.

These stages of a wealthy family life cycle are usually not of equal duration - and sometimes may be skipped altogether. An example of this might be a very active family head who continues to actively invest the family's wealth until death, thereby skipping Stage 4 altogether. Alternatively, the founder of the family business may decide to donate most of the family wealth to charity, thereby rendering Stages 5 and 6 irrelevant!

Relationship Between Family Life-Cycle and Family Office Life-Cycle

| FAMILY LIFE-CYCLE STAGE | DESCRIPTION | FAMILY OFFICE LIFE-CYCLE IMPACT |

| STAGE 1 - THE ENTREPRENEURIAL BUSINESS FAMILY | Cash-poor, time-poor, single business asset family | Manage issue of time poverty - however not much cash to spend. Often FD of family business or the family lawyer doing some of the "family office" type services |

| STAGE 2 - THE WEALTHY BUSINESS FAMILY | Cash-flow positive, time-poor, high concentration of assets still in family business | Bring order to chaos - think about the overall family wealth from overview and plan for the future. Look at de-risking overweight positions or hedging |

| STAGE 3 - THE DIVERSIFIED WEALTHY FAMILY | Cash-rich, partially or fully divested founder. Founder usually heavily in control of family investment outlook, often actively involved ("serial entrepreneur?") | Very active family who need lots of day-to-day support for their various investment activities and who wish to have their trusted advisers looking after their affairs |

| STAGE 4 - PRE-TRANSITION OF WEALTH | Cash-rich family with a settled lifestyle, time-rich, founders enjoying the fruit of their labours | Perhaps a little more passive than above - less day to day involvement and more desire to use external managers to preserve capital and seek returns |

| STAGE 5 - POST-TRANSITION OF WEALTH | Second generation - stay together? Conflict and different needs / wants? | Family office would appear to have a lasting place if the family wants to stay together |

| STAGE 6 - MULTI-GENERATIONAL FAMILY | Multi-generation - either stay together because of common interests or because of remaining interests in family business. Otherwise go their separate ways | Is the family office now a business in its own right which happens to be privately owned by a wealthy family? |

The table above summarises the effect that a specific stage of the family life-cycle will have on the related family office life cycle.

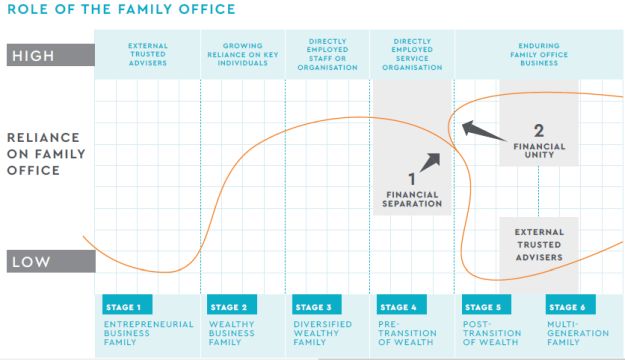

When the family are in stage 1 they are very unlikely to need a family office - they will instead rely heavily on external advisers such as lawyers and accountants and most of the advice will be surrounding active management of the increase in value of the business and business risk management. If they do have some personal financial issues that need to be examined urgently, the business's finance director may sometimes supply these services.

However, as they move through Stages 2 and 3 the need for a dedicated team becomes more pressing, especially if the level of wealth created is very substantial and the family's financial circumstances are complex. In these stages the family office can interact with the external advisers to co-ordinate and control the many complex issues facing the family, for which the family members themselves often have insufficient time or skills to deal with.

If the founder chooses to move to Stage 4 then the role of the family office changes to deal with inter-generational wealth transition issues. Once these issues are largely resolved, and if the founder continues to become less active, the family may decide to revert to using third party accountants, lawyers and investment managers. This decision may be heavily influenced by whether the second generation intend to continue investing together. If they do, continuity of a family office may be desirable to ensure smooth wealth transition and continuity of investment strategy. If this family office endures into the third generation and beyond it may even become a business of its own right that happens to be under private family ownership.

Pictorially this can be demonstrated in the chart below, which shows the level of reliance on the family office that the family will have in each stage.

Impact on private wealth professionals

Trustees, accountants, lawyers and investment managers may therefore act as advisers to families who go on to have family offices as their needs become more complex. They may also be successors to family offices in situations where the family becomes less active and therefore no longer needs dedicated staff. Most important to recognise are those situations where future generation family members choose to separate their financial interests from other family members and appoint their own advisers. It is therefore very important for private wealth professionals to recognise the life cycle stage that a particular family is currently in, and also where it is likely to go in future, and shape their advice accordingly.

Download our Guide to Family Offices

With each family office set up to meet the demands of a specific client family, there is no blueprint for how an effective family office should operate. Therefore, wealth professionals often need to access specialist family office expertise in order to fully understand the bespoke operational aspects their client's family office requires.

In response to this need for clarity and to act as a helpful indicator of what key issues are worth considering when establishing or operating a family office, we have produced A Guide to Family Offices. Download the full guide via the form here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.