MESSAGE FROM THE EDITOR

Welcome to the April edition of Clyde & Co's quarterly MENA Corporate News.

In this issue we cover:

-

Stop Press: Impact of the New UAE Companies Law on Foreign Investment

The UAE Government announced on 1 April 2015 that the new UAE Companies Law will come into effect three months after the date of publication in the Official Gazette. But what impact will the new law have on foreign investors? Click here for a link to the full article.

-

In Focus: Kingdom of Saudi Arabia

Investing in or sending employees to KSA? Then be aware of both the crackdown on breaches of the anti-concealment law and the new SAGIA fast track and impact program. Click here for a link to the full article.

-

In Focus: Franchising in Qatar

Franchising allows businesses to expand into the rapidly growing Qatar market although, as this article notes, it is not without risks. Click here for a link to the full article.

-

In Depth: Abu Dhabi Global Market – Update on the draft Legal Framework

In January the Board of ADGM published drafts of various key regulations. In this article, we examine in detail the draft Company Regulations which are based on the UK Companies Act 2006. Click here for a link to the full article.

With regards to deal flow, since our last newsletter in December, we have seen continued growth in the number of M&A deals we are working on across the region. Despite concerns in the market at the turn of the year that the dip in oil prices might affect confidence we still see a lot of movement in education, health and infrastructure along with increasing interest in the retail sector. Overall the fundamentals remain positive with a solid deal pipeline supported by strong business performance, particularly in the GCC countries.

We hope that you find MENA Corporate News a useful and informative read. In the coming weeks we expect to issue a number of specific updates on the new UAE Companies Law (once its full impact becomes apparent). In the meantime if you have any feedback or comments please do not hesitate to contact us.

STOP PRESS: IMPACT OF THE NEW UAE COMPANIES LAW ON FOREIGN INVESTMENT

The issue of the new Commercial Companies Law, Federal Law No. 2 of 2015, was announced by the UAE Government on 1 April 2015 and will come into effect three months after the date of publication in the Official Gazette. The new law introduces changes which will affect some of the structures used by foreign investors to establish businesses in the UAE. This article looks at some of the key changes and where the UAE government has left the previous position unaltered.

Foreign ownership restrictions

The nature and extent of the UAE foreign ownership restrictions has been the subject of political debate for a number of years. This is against a backdrop of increasing economic liberalisation in other GCC countries, at least on the face of the law. For example, in 2010, the Qatari government introduced the possibility of foreign investors owning more than a minority stake in Qatari companies in certain specified business sectors, such as tourism, health and education.

For now, the position in relation to the percentage capital which must be held by a UAE national, or a company wholly owned by UAE nationals, remains unchanged from the previous Commercial Companies Law (Federal Law No. 8 of 1984) (the 1984 Law). One or more UAE nationals must hold at least 51% of the share capital of any UAE company under Article 10(1) of the new law (where the company is partly owned by non-GCC nationals).

The new law reserves the power to the UAE Cabinet of Ministers to introduce additional regulations which restrict certain business activities to UAE national ownership only (such as commercial agencies and recruitment agencies which must be owned by Emiratis). There is no express provision which empowers the UAE Cabinet to relax the ownership restrictions. The UAE Minister of Economy has made clear that foreign ownership will, instead, be covered in a new Foreign Investment Law, which may allow wholly foreign owned companies in certain sectors of the economy.

Branch offices: sponsorship requirements

Under the new law, the requirement to appoint an agent who must be a UAE national, or a company which is wholly owned by UAE nationals, remains unchanged. Therefore, foreign companies wishing to do business in the UAE, without incorporating a new corporate entity, will still be required to appoint an agent and produce a notarised agency agreement as part of the branch establishment process.

Although the UAE requirements for local branch sponsors have not been relaxed, it is important to bear in mind that the option of using a branch entity to operate a services based business onshore in the UAE is not generally available in other GCC countries. For example, Kuwait does not allow non-GCC investors to operate through a branch at all and, in Qatar, the use of a branch is limited to companies which have entered into a contract with the Qatar government (or government owned agency or company), and only in order to perform that contract.

LLCs: changes which affect foreign investors

LLCs are the most commonly chosen investment vehicle for foreign investors looking to establish an entity with separate legal personality and with limited liability for its shareholders. Generally, an LLC offers the most flexibility for structuring management and shareholder control (subject to the foreign ownership restrictions).

The following is a list of some of the amendments made by the new law which may affect the structuring of LLCs used for foreign investment:

- No cap on number of directors: the 1984 Law set the maximum number of directors which an LLC could have at five. Under the new law, the maximum has been removed. Where there is more than one director, they form a board with such powers and functions as set out in the memorandum of association. The removal of the cap enables more flexibility in structuring the management of the LLC. For example, often foreign investors are interested in having a high number of directors, with a spread of overseas and local representatives with delegated authorities, and different layers of management control.

- Share pledges: Under the 1984 Law, there was much debate as to

whether it was legally permissible for a shareholder to pledge its

shares in an LLC as security. Article 79 of the new law makes clear

that it is possible for a shareholder to pledge its shares to

another shareholder, or to a third party. The pledge must be

registered in the Commercial Register, created in accordance with

the LLC's memorandum of association and under a specific

document for that purpose. Article 81 goes on to state the method

by which the pledge may be enforced against the shares in the case

of insolvency of a shareholder. If the creditor is another

shareholder in the same LLC, it may agree with the pledgor and the

LLC to acquire the shares. If the creditor is a third party, the

shares must be offered for sale by way of public auction, although

the LLC may elect to buy-back those shares from the bidder on the

same terms within 15 days of the auction. In either situation, the

remedies for the creditor are not self-help remedies because the

agreement of third parties is required in order to obtain the

shares, or the cash equivalent, to recover the debt due.

This change was widely anticipated following the release of the 2011 draft of the law and due to a policy change in the Dubai Department of Economic Development in relation to the ability to register a share pledge in the Commercial Register in favour of a UAE financial institution. However, there are a number of areas in relation to the pledge which will need to be clarified in practice under the new law. In particular, the interaction between the pledge provisions and the foreign ownership rules and the way in which a pledge may be perfected as regards other creditors of the shareholder is not clear. For example, the Commercial Register is not open to public inspection and therefore it is difficult for a prospective creditor to be certain as to prior competing interests without the co-operation of the LLC. In addition, the new law does not require a share certificate to be issued (which could be retained by the creditor). The memorandum of association may require a note of the security to be made in the company registers, however, as some protection for the creditor.

Share pledges are an important topic for foreign investors choosing to incorporate an LLC in the UAE. The foreign investor will often lend the amount of the capital to the UAE national shareholder to enable it to acquire its 51% interest and the foreign investor will require security for that loan. Therefore, confirmation that share pledges are legally enforceable is welcome. - Increase in shareholder numbers: it is now possible for LLCs to have up to 75 shareholders. This is an increase from 50 shareholders in the 1984 Law. In practice, this is unlikely to have a significant effect on most LLCs. It is unusual for an LLC to have a large number of shareholders because all share transfers are subject to pre-emption rights and any change in the memorandum requires all shareholders to attend the public notary to approve the change.

- Shareholders meetings – notice: there have been a number of modernising changes made to the way in which LLC shareholder meetings may be conducted. First, the notice period for a shareholder meeting has been reduced from at least 21 days to at least 15 days. It is also possible for the shareholders to consent to shorter notice with unanimous approval. In addition, the method of providing the notice of meeting to shareholders is no longer restricted to registered letter: the memorandum of association may set out any other permissible method of notice, which may presumably include email notice.

- Delegation by shareholders: it is now possible for a shareholder to delegate attendance at a shareholder meeting to a third party who is not another shareholder of the LLC. This provides more flexibility for individual shareholders. In the case of a corporate shareholder, different authorised representatives of that shareholder (usually employees) may attend and vote on behalf of the corporate shareholder.

- Quorum and voting rights: the quorum and voting requirements of

LLC shareholder meetings have been amended. It was previously the

case that, in order to pass an ordinary shareholder resolution,

shareholders representing at least 50% of the share capital had to

vote in favour of the resolution. There was not, however, any

separate quorum requirement. In practice, the quorum for the

meeting also had to be shareholders representing more than 50% of

the share capital (and potentially more, if there was no certainty

that all the shareholders present would vote in favour).

Under the new law, there is now a separate quorum requirement. For a shareholder resolution to be passed, there is a two step process: shareholders holding at least 75% of the share capital must be present at the meeting for the first time the meeting is called, in order for the meeting to be quorate. Resolutions are then passed by the majority of shareholders present at the meeting voting in favour, or such higher number as specified in the memorandum of association. This is a numerical majority of shareholders at the meeting, and not based on percentage capital holdings. It is not clear whether the memorandum of association may provide, instead, for all shareholders (whether present or not) to vote in favour. Any change to this effect will need to be approved by the public notary.

If the requisite quorum is present first time, there is no material effect on the "typical" UAE LLC comprising one foreign shareholder holding 49% of the shares and one UAE national holding 51% of the capital if the meeting goes ahead the first time it is called. For companies incorporated under the 1984 law, the memorandum of association usually requires that all shareholder resolutions to be passed by the votes of shareholders holding at least 75% of the capital (or with unanimous approval). Therefore, the UAE national shareholder is unable to pass a shareholder resolution acting alone and the foreign investor had a blocking right. Under the new law, provided that all the shareholders attend the meeting first time, the foreign investor will have the same blocking rights because the meeting will not be able to proceed without it and, with two shareholders present, both would need to vote in favour.

However, there are certain situations in which the effects of the new law will need to be considered more carefully. In particular, if there are more than two shareholders in a UAE LLC, it will be important to determine which combination of shareholders may hold quorate meetings together, without all being in attendance. In addition, it will be critical for shareholders to have watertight powers of attorney or other delegations of authority in place for others to attend meetings and vote on their behalf. Missing the first shareholder meeting may have a negative impact: if a quorum is not reached first time, the requisite quorum decreases to holders of 50% of the share capital needing to be present in person and, on the third attempt, no specified quorum is required. This means that the UAE national shareholder would be able to pass shareholder resolutions without the foreign investor being present, if the first meeting does not occur and that any shareholder could single-handedly pass a shareholder on the third time a meeting is convened. The new law does not state that it is possible to provide for a higher quorum under the memorandum of association.

It is important to note that proper notice of the meeting must be given, but the new law still requires shareholder meetings to be attended in person. There is no provision which expressly allows the memorandum to provide for other ways of passing shareholder resolutions. In practice, the memorandum of association may provide for written resolutions, but these require all shareholders to sign to reduce the risk of the validity of the resolution being challenged. - Holding companies: the new law allows for an LLC (and a joint stock company) to be established the sole object of which is to hold subsidiaries incorporated in the UAE or overseas. A Holding Company may undertake ancillary activities to that primary object which are set in an exhaustive list in Article 267: management of its subsidiaries, providing loans, guarantees and finance to its subsidiaries and acquiring moveable assets, real estate and intellectual property assets for the purposes of its holding activities. A Holding Company will not be entitled to trade or undertake any other activities. Such a company will be required to have the words "Holding Company" in its title. Under Article 270, it will be required to produce consolidated group accounts in accordance with internationally accepted accounting and audit practices and standards. This is a welcome addition to the company structuring options which was not available under the 1984 law under which foreign companies frequently had to find an appropriate licence category. The practical requirements related to these Holding Companies, such as the commercial premises requirements, are however yet to be clarified.

What do we need to do to implement the new law?

The new law does not contain any provisions which deal with the implementation of the new law by existing companies, such as "grandfathering provisions" under which the old legislation continues to apply to companies established under the previous law. The new law will apply to all UAE companies from date falling three months after its publication in the Official Gazette, as well as all UAE companies to be established in the future.

The law makes some important changes to the way in which a UAE LLC operates from a management and shareholder perspective. In certain cases, LLCs will want to ensure that their current memorandum of association allows them to take advantage of any new flexibility provided for in the law and takes into consideration any more restrictive amendments. We recommend that all companies reconsider their memorandum of association and shareholder arrangements, together with any corporate governance guidance provided to directors, as soon as possible to ensure that they get the best from the new UAE company law regime.

IN FOCUS: KINGDOM OF SAUDI ARABIA

Doing business in KSA? Sending employees to KSA? Not without a licence!

Sending employees to KSA

The Kingdom of Saud Arabia(KSA) is one of the largest economies in the Middle East and a market which has attracted more and more activity in the past six years. Often businesses will seek to explore the market through a partner or a third party with which employees are placed and through which they seek to operate in the Kingdom.

Such operations will more often than not fall foul of KSA legislation designed to prevent a non KSA entity using a KSA entity's trade licence to do business in the Kingdom. Over the past three years, we have seen the KSA authorities clamp down on activities they regard as harmful to the economy and in breach of legislation.

In 2013 a six month immigration amnesty resulted in millions of individuals correcting their status, and thousands being deported for illegal working.

This regulatory clampdown has continued into 2015. In the past few months the Ministry of Commerce and Industry (MOCI) has intensified its campaign against illegal business ventures being conducted by expatriates in the name of Saudis (Concealment) (referred to in Arabic as ''Tasattur'') as part of efforts to put an end to what it called "the most dangerous practice" affecting the business community in the Kingdom.

Article 1 of the Saudi Arabian Anti Concealment Law issued by Royal Decree No. (M/22) dated 4/5/1425H (corresponding to 22/6/2004) (Anti Concealment Law) provides that any Saudi who enables a non-Saudi to use the Saudi's licenses and other facilities to invest or engage in commercial activities in KSA without (where available) the necessary authorisations and licenses shall be considered as committing the offence of "concealment". Articles 4 and 5 of the Concealment Law provide that a party guilty of "concealment" may be punished by:

- A fine not exceeding SAR 1 million (approximately USD 266,667)

- Imprisonment for a term not exceeding two (2) years

- Deportation from the Kingdom

- Being barred from re-entering the Kingdom

In addition, the foreign party involved in any "concealment" may be assessed for tax by the Department of Zakat and Income Tax on the basis of the deemed profits earned in the course of the activities that were "concealed".

Various arrangements can fall foul of the Anti- Concealment Law, including the placement of employees into an agent, client or other partner. The key concern is to monitor employees' activities, business cards and their presentation to the market.

Recently, the Council of Ministers has instructed relevant agencies to carry out surprise inspections in the market and report Tasattur businesses to MOCI. As a tool of enforcing the Anti Concealment Law, the Kingdom is planning to monitor the foreign currency transfers of expats, in order to check if such transfers are coming from Tasattur business activities.

New measures impacting foreign investment

In recent months the Saudi Arabian General Investment Authority (SAGIA) has introduced a number of changes that will impact foreign investors. These include:

- the announcement in June 2014 of a fast-track license application procedure for certain qualifying applicants (Fast Track Procedure);

- the implementation in October 2014 of a new programme to measure the impact of foreign investment in KSA (Impact Programme).

Overall this appear to be part of an emerging twin track approach of encouraging foreign investment whilst simultaneously being more choosy about which foreign investors can come into the market (and which can stay).

The Fast Track Procedure

Under the Fast Track Procedure the following type of foreign investors may be eligible to submit an abbreviated licence application:

- Multinational companies

- Publicly listed companies on an international stock exchange

- Foreign companies that manufacture products that are classified and approved by independent agencies and employ certified process technology

- Foreign companies that own certain registered trademarks, patents, or copyrights

- Foreign companies that are establishing a regional office in KSA

- Foreign construction companies that are classified as Class A in their home country

- Foreign companies with assets worth more than USD 13.33 million, that have above 2,000 employees, and that have completed at least one project with a value of at least USD 133.3 million

- Foreign companies contracting with the KSA government or a KSA government-owned entity or entering into a joint venture with a KSA company listed on the KSA Exchange

As a firm we have successfully made a number of Fast Track Procedure applications. In some cases the SAGIA licence was issued in as little of one week – although it should be noted that it still takes time to gather together all the application documents.

The Impact Programme

Under the programme, the impact of licensed entities will be measured according to the following foreign investment objectives:

- Transfer and localization of technological know-how

- Diversification of KSA's economy

- Increasing of exports and decreasing of imports

- Developing KSA human resources

- Reinforcing economic competitiveness in both domestic and international markets

- Balanced development among the different regions of KSA

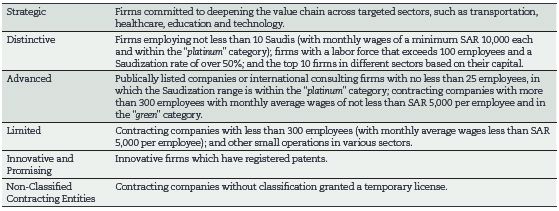

Entities which demonstrate that they are fulfilling these objectives will be granted special incentives and privileges to help promote and motivate excellence and sustainability. According to the programme, licensed entities will be divided into the following categories:

It will take time to see the full impact of this programme in practice. However, the potential advantages and benefits will be granted to licensed foreign investments according to their categorisation. For example, longer SAGIA license periods will be available to entities which are strategic (5 years), distinctive (3 years) and advanced (2 years)together with enhanced service priority in business centres.

SAGIA has also confirmed its intention to develop new formulae to measure the 'added value' provided by licensed entities. These are to be based on quantitative data derived from the balance sheets of such entities together with qualitative data derived from analysis of their operations in practice.

Conclusion

In summary, the Fast Track Procedure and Impact Programme represent a new approach by SAGIA to encourage and measure the foreign investments into the Kingdom. It is too early to assess fully the impact these initiatives will have on foreign investments, however, both existing licensed foreign investors and those considering an investment in the Kingdom will wish to examine and assess the new SAGIA objectives carefully.

To continue reading please click here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.