- within Wealth Management, Employment and HR and Transport topic(s)

- with Senior Company Executives, HR and Inhouse Counsel

- with readers working within the Law Firm industries

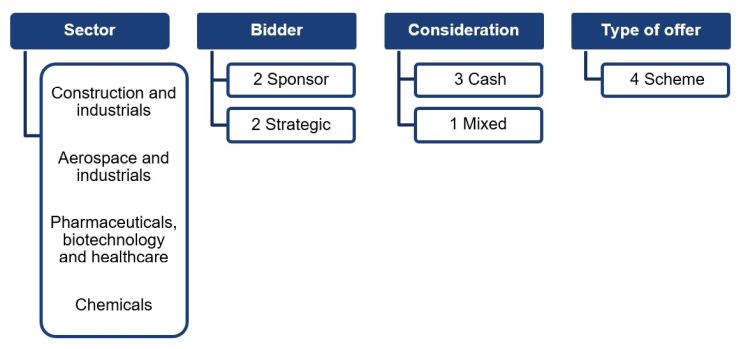

In April 2026, there were four Rule 2.7 announcements made across the UK public M&A market and six further possible offers / sale processes announced.

Firm Offers announced this month:

- Recommended cash offer by Tinicum Incorporated and Blackstone Inc. for Senior plc – £1.28 billion – public to private

- Recommended cash offer by STRABAG SE for Van Elle Holdings plc – £58.8 million

- Recommended cash offer by Charterhouse Capital Partners LLP for Animalcare Group plc – £235.2 million – public to private – unlisted securities alternative

- Recommended cash offer by Döhler Group SE for Treatt plc – £183 million

Possible Offer announced this month:

- Private sale process announced by Gemma Communications plc

- Strategic review including formal sale process announced by Aptitude Software Group plc

- Possible offer by Acceler8 Ventures plc for Intuitive Investments Group plc – £600 million – share consideration

- Possible offer by EQT X EUR SCSp and EQT X USD SCSp for Intertek Group plc – £8.93 billion (increased from £8.31 billion and £7.93 billion) – cash consideration

- Possible offer by TA Associates (UK), LLP for Advanced Medical Solutions

- Possible offer for Deltic Energy plc – in discussions with three separate parties: Capricorn, Petrogas and Blue Concept – cash consideration

Firm Offers breakdown this month:

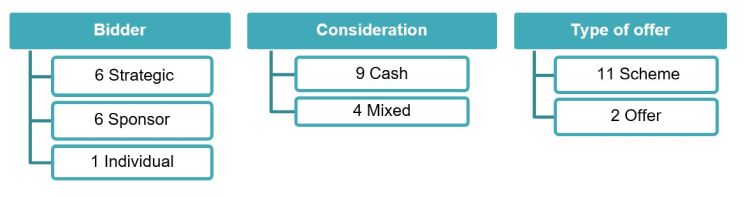

Year to date breakdown:

April 2026 Updates:

Latest FCA guidance in Primary Market Bulletin 62

The Financial Conduct Authority (FCA) has published Primary Market Bulletin 62 (PMB 62), its newsletter for primary market participants.

The main topics covered in PMB 62 are the FCA's enforcement cases against Carillion and its former directors and a review of sponsor services provided on transition to the equity shares (commercial companies) category (ESCC) (see our blog post here).

FCA warning about fake takeover approaches

The FCA expressed concerns in PMB 62 that UK micro- and small-cap issuers are being targeted as part of potentially manipulative schemes to affect their share prices.

In particular, the FCA warned of an increase in fake investor takeover approaches, whereby parties pose as genuine investors seeking to make a takeover offer. They then either leak the news to the press or push the issuer to disclose it, with the aim of increasing the share price, at which point the parties can profit from the price movement – under Rule 2.2 of the Takeover Code, a potential target is required to make a possible offer announcement following an approach if it is the subject of rumour or speculation or if there is untoward movement in its share price.

|

Market manipulation under Article 15 of the UK Market Abuse Regulation (UK MAR) A fake takeover approach would fall squarely under the prohibition on market manipulation in Article 15.

Article 12 also prohibits the dissemination through the media of information which the disseminator ought to have known was false or misleading. |

The FCA encourages issuers to carry out appropriate due diligence on an approach before engaging with any proposal. This includes making sure they:

- know who the investors are;

- confirm that the offer is genuine; and

- review the investors' track record for any similar deals.

If an issuer identifies concerns that they may have become the target of such activity, it should report it to the FCA.

April 2026 Insights:

The number of firm offers announced this month has had a slight decline, with only four firm offers compared to seven in April 2025. The number of possible offers has also fallen, down from nine to six. This probably reflects the uncertainty in the market at the moment due to geopolitical destabilisation with the Iran conflict and pressures on interest rates.

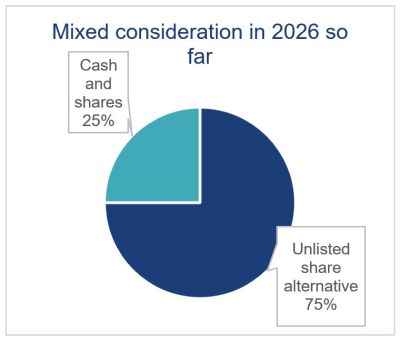

So far in 2026 there have been 13 firm offers announced. Nine have included cash consideration and four have included mixed consideration. Out of the four mixed consideration offers, three included unlisted securities alternative as part of the proposed consideration (often called "stub equity"). Stub equity allows some shareholders to retain a minority equity interest in the target company after the acquisition. This structure was for example used in Charterhouse Capital Partners LLP offer for Animalcare Group plc and Helios consortium offer for CAB Payments Holdings plc. The Takeover Panel's Practice Statement 36 discusses its approach to unlisted share alternatives.

Useful links

- Herbert Smith Freehills Takeovers Portal.

- Herbert Smith Freehills Public M&A Podcast Series.

- The Takeover Code.

- The Takeover Panel’s Disclosure Table (detailing offeree companies and offerors currently in an offer period).

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]