- within Energy and Natural Resources topic(s)

Institutional and private capital are turning to single-family housing as a scalable route into UK residential investment. This note examines the drivers behind the sector's growing momentum and the considerations for investors entering the market.

Single-family housing (SFH) is an increasingly prominent segment of the UK built-to-rent (BTR) market and is capturing the attention of institutional and private capital.

A combination of structural housing undersupply, strong demand for family housing in suburban locations and sustained investor appetite for residential income is bringing SFH into sharper focus. This momentum is increasingly visible across the country, with Savills reporting that nearly 40% of local authorities in England and Wales have had SFH brought forward within their housing delivery.1 These dynamics are prompting investors to explore SFH as a route to accessing residential rental income through a distinct development and operational model.

This note considers why the sector is gaining momentum in 2026 and highlights some of the opportunities and considerations for investors exploring SFH in the UK.

The advantages of SFH

Whilst sharing many of the hallmarks of conventional multifamily BTR (being professionally managed, institutionally owned and purpose-built for rental) SFH represents a distinct product. SFH typically takes the form of houses rather than flats and is commonly located in suburban areas. These characteristics create a number of advantages in the current residential market.

Tenant demography

Located in suburban areas with greater private amenity space (such as gardens) and offering a relatively low-density setting, SFH tends to appeal more strongly to families. Around 38% of SFH households comprise single-family households compared with 21% in the wider private rented sector (PRS), and only 6% of multifamily BTR.2 As a result, SFH tenants tend to be older, with evidence suggesting that 35% are over 35, compared with 25% multifamily BTR occupiers.3

Family households are viewed as less transient, as relocating can disrupt schooling and employment arrangements. This can lead to longer tenancy durations and lower turnover, reducing void periods and supporting more stable occupancy levels. For institutional investors, the resulting stability of income can resemble the long-duration, bond-like cashflows sought by pension and other liability-driven capital. When combined with the potential for rental growth over time, this can provide an income profile that aligns well with investors seeking inflation-linked returns.

SFH portfolios also benefit from a high degree of income granularity. Rather than relying on the performance of a single building, income is generated across large numbers of individual homes often spread across multiple locations. This diversification can reduce the concentration risk associated with single-asset rental blocks and contribute to more stable portfolio-level income streams.

Relative regulatory simplicity

Regulatory complexity has become an increasingly prominent theme in discussions across the UK living sector, with developers and investors frequently citing it as one of the key challenges affecting residential delivery.

Much of this stems from the Building Safety Act 2022, which represents the biggest change to building safety in forty years. For higher-risk buildings, the Act has introduced additional regulatory scrutiny through the Gateway regime and a more extensive compliance framework during both the development and operational phases of a building.

The Act has also increased the technical burden on high-rise schemes, with the design and construction stage requiring far greater documentation, while significant ongoing responsibilities have been imposed on accountable and responsible persons during the occupancy phase of the asset.

SFH developments are not exempt from the wider building regulations framework, and new-build suburban BTR must still comply with modern safety and construction standards. However, SFH will typically fall outside the higher-risk building (HRB) regime and is therefore not subject to the same Gateway approvals process, or the same level of regulatory oversight during development and occupation. As a result, SFH may offer a comparatively more straightforward compliance framework for investors and operators and reduce the scale of ongoing operational compliance obligations associated with HRBs.

Delivery efficiency

SFH schemes are often delivered using standardised house types constructed by national housebuilders, supporting efficient construction programmes and relatively predictable build costs. Many of the transactions we are seeing involve forward funding or forward purchase arrangements with regional housebuilders, allowing investors to influence design and delivery while securing early access to completed homes. Homes can then be handed over in stages, with completed units progressively transferred to the operator as they are delivered.

This enables homes to be "drip fed" into the leasing programme over time, rather than entering the rental market simultaneously. The phased approach reduces concentrated lease-up risk and allows income to be generated earlier in the development lifecycle as homes are occupied on a rolling basis. For investors, this delivery model can support a smoother stabilisation profile as schemes mature.

The relative simplicity of suburban houses as an asset class also reduces an investor's exposure to cap-ex volatility through the lifecycle of the investment.

Strategic flexibility

Against a backdrop of increased market scrutiny and capital discipline, investors are increasingly focused on the resilience of residential assets and the ability to adapt strategies over the life of an asset. The degree of flexibility available within a scheme is therefore often a factor considered in investment committee discussions when assessing downside protection and exit optionality.

As the multifamily BTR sector has matured, many urban planning authorities have begun to recognise it as a distinct housing product and an important component of the urban housing pipeline. In some cases this has resulted in planning permissions being granted subject to obligations (typically secured through section 106 agreements) that restrict developments to BTR tenure in order to preserve long-term rental supply. It seems that to date, planning authorities haven't applied similar tenure restrictions to SFH schemes in suburban locations. As a result, investors may retain greater strategic flexibility, with the potential to pivot between long-term rental investment and alternative exit strategies, including for-sale disposals. This tenure optionality can provide an additional layer of downside protection for capital deployed in SFH schemes.

Energy efficiency and tenant affordability

Increasingly, SFH are eschewing traditional fossil-fuelled heating in favour of sustainable and decarbonised energy provision – with projects delivering a diverse mix of homes that benefit from air-source heat pumps, solar panels, and electric vehicle (EV) charging points, forming part of a wider Sustainable Urban Extension.

Beyond the environmental benefits, highly energy-efficient homes can significantly reduce (and in some cases largely eliminate) tenants' energy bills. This can improve affordability for households and limit their exposure to energy price volatility. Where "all-inclusive" rental models are adopted, the economic benefits of improved energy performance can also contribute to stable operating costs and income resilience for investors. This alignment between tenant affordability and asset performance is increasingly attractive to both institutional and private capital allocating to residential strategies.

Untapped potential in 2026

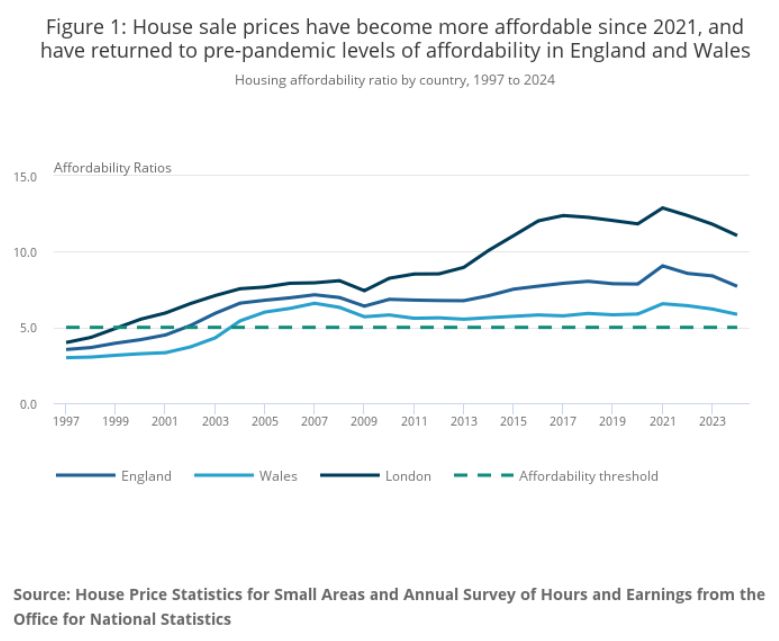

Residential has established itself as global private capital's preferred real estate investment sector, with investors frequently citing the systemic undersupply of housing stock as a key driver.4 This chronic shortage has been identified by the UK Government as a central factor in the housing affordability crisis, which has seen house prices outpace median wages since the early 2000s.5

ONS, Statistical bulletin - Housing affordability in England and Wales: 2024

Tackling the shortage is high on the Government's agenda, with a commitment to deliver 1.5 million new homes in England by the end of the current parliament. 6 SFH has the opportunity to play a significant role in meeting this target, helping to bridge the affordability gap while providing quality, professionally managed long-term homes for households. There are already signs that this shift is underway, with Knight Frank's survey of 60 of the largest investors in the UK living sectors earmarking SFH as the biggest growth area in the next five years.7

The UK Government's approach to tackling the housing affordability crisis differs markedly to that of the US, long-viewed as the most established and leading BTR market, where a recent executive order has sought to restrict institutional investment into SFH and the Senate has passed the bipartisan 21st Century Road to Housing Act, which, if enacted, would require institutional developers of BTR housing to sell new SFH to individuals within seven years. While the UK Government's legislative agenda is directed at strengthening tenant protections, its emphasis on professional standards and regulatory compliance may in practice favour institutional operators, reinforcing the UK's position as a compelling destination for private capital in residential real estate at a time when the US appears to be moving in the opposite direction.8

Nonetheless, England is predicted to experience a further short-term contraction in PRS supply. The combination of increased tax on second home ownership and the introduction of the Renters' Rights Act 2025, the biggest legislative reform to the PRS since the 1980s, is continuing to accelerate the exit of smaller landlords from the market. Data demonstrates landlords are selling homes to owner occupiers faster than they are being replaced while as many as 46% of private landlords indicated they were considering selling properties within the following 12 months.9 Additional supply will therefore be necessary to accommodate the more than three million renters already living in suburban areas in the UK.

Taken together, these conditions suggest there remains significant untapped potential. Despite growing investor interest, Knight Frank analysis indicates that institutional investment currently represents just 0.2% of privately rented homes in the UK as of April 2025, highlighting how early the sector remains in its development and the large scope for further participation from both institutional and private capital.10

Looking forward: the keys to success

SFH investment has traditionally been deployed via forward funding and forward purchase structures, with transactions often forming part of joint ventures or strategic partnerships with regional housebuilders.

These models can be economically aligned for investors and housebuilders: the former gaining greater control of the end product, influencing design and safeguarding quality, and the latter receiving funding certainty early in the process, reducing exposure to open market sales risk – particularly relevant in a higher-rate environment where working capital discipline is critical for many SME housebuilders. Consequently, housebuilders are increasingly turning to institutional capital to offset open-market headwinds.

As the public increasingly view renting as a long-term housing solution, greater demands may be placed on landlords. High-quality, professionally managed housing with strong infrastructure connectivity will be expected by tenants – and consumer demands will be reinforced by regulation. Enhanced energy efficiency standards in the coming years, and the forthcoming expansion of the Decent Homes Standard (also known as Awaab's Law) to the PRS are just two examples. Investors who have established strategic delivery partnerships and built quality-led brands, synonymous with "best-in-class" regulatory compliance, will be particularly well placed to realise SFH opportunities at scale.

In addition, the nature and structure of SFH transactions (often involving multifaceted joint ventures and forward funding arrangements) means that a wide range of stakeholders are typically involved, including investors, developers, landowners, public authorities and delivery partners. Many SFH investments are delivered within complex masterplans where homes are acquired alongside other housing tenures and infrastructure obligations, requiring careful coordination between these stakeholders. This can involve navigating complex land arrangements, infrastructure delivery obligations and multiple overlapping rights between neighbouring parcels of land, often within compressed commercial timelines.

Investors and their advisers with deep UK development expertise and the ability to navigate these dynamics efficiently and commercially will therefore be best placed to scale SFH strategies successfully.

Conclusion

Suburban living has long been a defining feature of the British housing market: the enduring aspiration to live in a house with a garden. More than three million renters already live in suburban locations, and current demographic trends suggest that demand for this form of housing is unlikely to diminish. As the gap between average house prices and median wages continues to widen, renting is increasingly viewed as a long-term housing solution, with many households willing to allocate a greater share of their income to secure the space and stability associated with suburban living.11

Against this backdrop, SFH is well placed within the current political, regulatory and economic landscape. As residential continues to attract global capital, but with institutional participation in SFH still at an early stage, the sector is emerging as one of the most scalable and "institutionalisable" prospects within the UK living market.

Footnotes

1. Savills, Single Family Housing Spotlight 2025, p.3.

2. British Property Federation, BPF Spotlight Series: Who Lives in Build-to-Rent?, p.22.

3. Ibid, p.23.

4. INREV, Investment Intentions Survey 2026, executive summary.

5. Office for National Statistics, Housing Affordability in England and Wales: 2024, pp.4 - 5.

6. Homes England, Policy paper: Homes England strategic plan – 2025 to 2030, p.18.

7. Knight Frank, The SFH Report 2025, p.2.

8. INREV, Investment Intentions Survey 2026, executive summary.

9. Knight Frank, The SFH Report 2025, p.11.

10. Knight Frank, The rise of new entrants in the UK's single family market, 9 April 2025.

11. British Property Federation, BPF Spotlight Series: Who Lives in Build-to-Rent?, p.24.

Macfarlanes is a pre-eminent law firm advising a global client base across Private Capital, Private Wealth, M&A and Disputes.

Visit our website to learn more about our services and how we can assist.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]