- within International Law topic(s)

- with readers working within the Banking & Credit and Transport industries

- within Criminal Law, Wealth Management and Intellectual Property topic(s)

U.S. brands and retailers have understandably focused on tariff pain at the border, but the real sleeper threat sits upstream: margin pressure turning a fragile supplier into a single-point failure. Early intervention to stabilize and, where needed, support in supplier restructuring is critical to keep goods on shelves and profitability intact.

As global manufacturing braces for a second year of shifting U.S. trade barriers and uncertainty over where tariff policy goes next, the supply chain's key pressure point remains unchanged: smaller suppliers in China and other hubs are still the most likely to buckle. Compounding this, the ongoing conflict in the Middle East is adding upward pressure on input and logistics costs, further squeezing already‑thin margins across manufacturing hubs. For American brands and retailers importing everything from rubber gloves and toys to apparel and electrical appliances, the riskiest counterparties are those suppliers that entered 2025 under strain, and are now seeing tariffs eat through margins that were already compressed. With small and mid-sized factories, financial distress may not be visible until it shows up as a missed shipment – or an abrupt default. It's a third-party risk no U.S. brand or retailer can afford to ignore: today's fissures in the supplier base can quickly escalate into crises that demand turnaround and restructuring support to maintain product flow and contain the P&L hit.

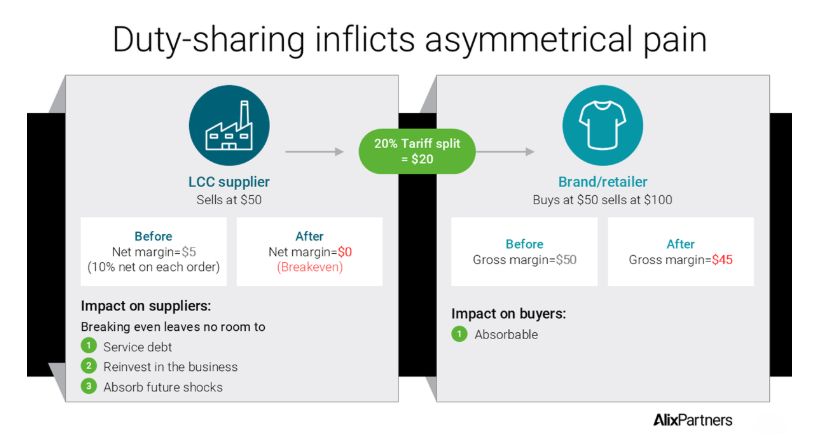

Duty-sharing inflicts asymmetrical pain

There is little public disclosure on how buyers and suppliers renegotiated prices in the months after the imposition of new tariffs, but industry feedback suggests a 50:50 split is a common outcome, with each side agreeing to absorb half the extra duty. That's equitable on paper, but in reality, the impact on profitability is deeply uneven and, for those suppliers that started the year with strained balance sheets and thin liquidity, possibly existential.

Take a simplified example: a brand or retailer buys a T-shirt at $50 and sells at $100. A 20% duty, split between both sides, lowers the buyer's gross margin from $50 to $45. With a mixed assortment and some pricing flexibility, that hit is unwelcome but absorbable. For the supplier, which may earn only 10% net on each order, a $5 tariff contribution effectively wipes out its profit. Breaking even leaves no room to service debt, reinvest in the business, or absorb future shocks.

The details may vary, but the underlying dynamic is the same across tariff-sharing deals. Even in instances where U.S. importers and consumers absorb most of the levy in the aggregate, the share that falls to a factory running on razor-thin margins can be enough to tip a knife-edge balance sheet into full-blown distress.

Thin cushions and sharp shocks

For many smaller manufacturers, balance sheets were already under strain. The Federal Reserve Bank of Dallas Global Institute reported in December that even prior to the tariff hikes, nearly 30% of China's industrial firms were operating at a loss – up 20% since the pandemic – with many of the pressures concentrated in investment-heavy manufacturing sectors. The typical SME exporter is often highly leveraged, with cash flow already committed to servicing interest payments. When tariffs cut into prices and/or reduce order volumes, cash flow no longer covers interest or working capital needs, and liquidity can dry up quickly.

The pressure doesn't hit every manufacturer equally: better-capitalized firms with diversified customer bases and higher value-add production can absorb more of the shock, while smaller suppliers that rely on a handful of key U.S. customers are closest to the brink.

Hidden dependency and limited visibility

For brands and retailers, the real risk is supplier dependency. If, for example, a retailer buys half of its electronic toys from a single supplier that falls into a liquidity crisis and stops shipping, then 50% of its assortment in that category is in danger of vanishing from shelves, translating directly into lost sales and customers. The risk is most acute when that dependency involves long lead times, complex construction or heavy compliance requirements that hamper quick substitution. Even trusted mitigation strategies like dual sourcing are not failsafe: if a brand sources 60% from Supplier A and 40% from Supplier B, and B collapses, A may not have the capacity, financing, or regulatory approvals to make up the volume shortfall.

To compound this, many of these firms are privately owned, in jurisdictions where financial disclosure is limited and reliable credit scoring is either patchy or absent.

The silence problem

The structural risk is compounded by a behavioral one, particularly in Far Eastern markets: suppliers under strain are often slow to speak up. Management and shareholders hold out in the hope of improving conditions, or fear that transparency will drive customers away. The first clear signal of supplier distress comes far too late, erupting as a cluster of issues including:

- Factory strikes that disrupt production as workers protest non-payment of wages;

- Sub-suppliers refusing to supply raw materials and components due to overstretched credit;

- Corner-cutting in sourcing, production, or compliance to save cash – raising operational, quality and regulatory risk for the buyer.

Turning supplier fragility into a managed risk

All of this means that for brands and retailers, the danger isn't the headline tariff itself, but the underlying vulnerability that turns a previously reliable vendor into a supply continuity risk. One consumer brand, for instance, risked losing more than 10% of its sales when a major supplier's financial distress surfaced as workforce strikes.

This underlines the importance of proactive scrutiny: procurement, finance and risk teams need to treat tariff-hit suppliers as third-party financial risks to be tracked and actively managed, not left to chance.

Practical steps:

Map tariff-exposed categories – and suppliers

Understanding which categories account for most of the tariff bill helps pinpoint suppliers experiencing the most severe cost shocks. Priority attention should go to small and mid-sized manufacturers that a) have recently been stretched financially, e.g., by opening a new plant, and b) account for a high percentage of the buyer's spend or a key share of a flagship category.

Look past KPIs to the balance sheet

Step up monitoring of behavioral red-flags: requests for shorter payment terms or price increases, or the sudden introduction of factoring. Where the supplier uses approved sub-suppliers, confirm directly with them that payments are being made as normal.

Develop and rehearse continuity options

Line up and vet backup suppliers or locations early – recognizing that this usually means swapping one risk profile for another rather than eliminating risk altogether. Then stress-test scenarios in which a key supplier loses funding or enters restructuring, and turn those tests into clear playbooks for inventory, pricing and customer commitments.

Be ready to intervene – when the numbers support it

If everything else has failed, be willing to step in. When a critical, high-dependency supplier is sliding towards failure, buyers may need to offer support – from temporary price relief to a structured rescue – when intervention costs less than letting the supplier go under.

Focusing now on suppliers that are both vulnerable and critical can be the difference between a disruption that stays manageable and one that spills over into empty shelves and missed sales.

If you are reassessing how robust your supplier base really is, AlixPartners Asia can help: we work with brands and retailers to benchmark risk, design practical responses, and move quickly from concern to action.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]