The UK patent box regime, which applies a 10% rate of corporation tax to profits derived from patents, is now two years old. Has your company considered the potential benefits?

If your company owns UK or European patents (or is considering patenting items) then the patent box should be on your agenda. BDO has a multi-disciplinary team of experts to assist you at all stages of the process to make the most of this favourable incentive from the UK Government.

Early stages – let us help you plan

Tax relief through the patent box could eventually halve your corporation tax bill so you may now want to consider applying for patents where previously this was not cost-effective.

We can help you model the patent box profit and tax savings with our RealiZer tool. This gives you a high level indication of potential savings and identifies areas to maximise your benefit. We also have links with patent attorneys who can undertake the application process for you.

The benefits of the patent box come into force once a patent is granted but, by opting into the scheme during the patent application process, you can also claim the benefit for the patent pending period. So waiting until you have a patent could lose you money in the long run. Talk to us to find out what you need to do.

Navigating the eligibility rules

We can also help you navigate the rules on eligibility for either the patent, the company or the income streams. For example, the company must have made a significant contribution to the creation or development of the patented item or a product incorporating this item. In a group situation, provided the company holding the patent actively manages its portfolio of qualifying rights, another group company can undertake the qualifying development.

Alternatively, if you licence in patent rights, you must have exclusivity which is at least countrywide

Timing

We can advise you on the best time to elect into the patent box regime. It will not always be the case that the sooner you opt in the better: there may be some occasions when your company may want to wait.

Additionally, the 10% rate is being phased in over five years with the full benefit of 10% only achieved from 1 April 2017 onwards.

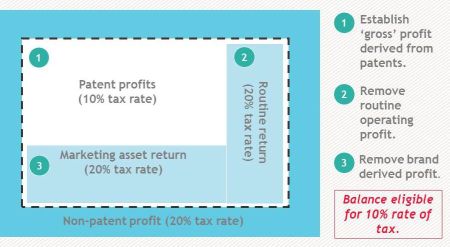

Calculation of the patent box profits

The calculation works by identifying the worldwide income and profits derived from the patented invention (or items incorporating it). This figure is then reduced by applying formulae for the return that you would have achieved regardless of the patent with a further reduction for an element of the profit derived from your brand.

Clearly, it is sensible to ensure that you maximise the profit going into the box and that the reductions are kept to a minimum. It is possible to take a more bespoke approach to the calculation and this may be beneficial. BDO's team of specialists can help you find the best result.

R&D and the patent box

The patent box is just one of a suite of tax incentives available to UK companies to encourage innovation. It is designed to complement the existing tax reliefs available for qualifying R&D. It is worth talking to us about your overall R&D and patent box strategy as the two often go hand-in-hand.

Transfer pricing and the patent box

Transfer pricing methodology may also play a key role in the calculations — even if your company is exempt from the normal transfer pricing rules.

BDO's patent box team comprises dedicated transfer pricing specialists who are able to ensure that both your patent box, R&D and transfer pricing strategies work together to give you the best tax result.

Groups of companies

Groups of companies, particularly those operating across international borders, may wish to consider their current structures and whether these remain appropriate in the light of the patent box regime. The international and transfer pricing specialists in our patent box network can assist you with such structuring decisions.

Recent developments

The UK patent box has been the subject of recent press coverage, raising uncertainty over its future. In December 2014, the Financial Secretary to the Treasury confirmed that the Government will retain the competitive patent box regime, with some amendments, such that it will now align more closely to R&D activity carried out in the UK.

The UK Government announced that the legislative process to introduce changes to the existing IP regime, so that it conforms to the re-modified nexus approach, will begin in 2015. In line with the normal tax policy-making process, the Government intends to consult with businesses and their advisers on these changes.

How we can help

In summary, we can offer help and advice at any stage of your thinking around patent box including:

- Working with you to identify qualifying IP and mapping this onto revenue streams

- Assessing the merits of electing into the regime

- Establishing where qualifying patents should be held

- Designing appropriate UK corporate structures

- Modelling the benefit with our RealiZer tool

- Analysing the different bases for calculation

- Developing transfer pricing methodologies and tools for data collection for computing income and expenses at the various stages

- Assisting with your compliance obligations and making the patent box benefit a reality on your corporation tax return

- Integrating use of the patent box into your overall R&D strategy.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.