Issues affecting all schemes

PENSION SCHEMES BILL

The Bill was reintroduced and received its first reading in the House of Lords on 7 January 2020, before its second reading on 28 January 2020.

The Bill broadly mirrors the provisions included when it was first published in October 2019, prior to Parliament being dissolved ahead of the general election. However, some minor drafting amendments have been made to the Bill, as well as some more substantial changes.

In particular, the wording relating to the statutory defence to contribution notices under the new "employer resources test" has been amended. Condition C has been updated so that it now refers to a requirement that it must have been reasonable for the individual to conclude that the act or failure would not bring about a reduction in the value of the employer's resources that would be a "material reduction relative to the estimated section 75 debt". The previous version of the Bill required the individual to be satisfied that the change would not bring about a reduction in the value of the employer's resources, regardless of whether that reduction was material or not. This change effectively widens the circumstances in which the defence can be used.

In addition, "relevant time" (for the purposes of estimating the section 75 debt for the employer resources test) is now defined as the time immediately before the first of the acts occurred, or the first of the failures to act first occurred where there has been a series of acts or failures. In all other cases, it will be the time immediately before the act, or failure to act, first occurred. Under the October version of the Bill, the Pensions Regulator was able to determine the relevant time during which there had been a continuing failure, effectively giving the Pensions Regulator the power to determine the amount of the debt that was due.

The Bill will now pass to the Committee stage, which will start on a date to be announced.

|

Action Trustees and employers should monitor developments in this area. |

RPI/CPIH CONSULTATION

On 13 January 2020, it was announced in a letter from Sajid Javid to the Chairman of the Economic Affairs Committee that the joint consultation between the Government and the UK Statistics Authority on proposed changes to RPI will be launched on 11 March 2020 (the same day as the 2020 Budget).

The proposed changes to RPI seek to address the shortcomings of RPI by bringing the methods of the CPIH measure of inflation into it.

The UK Statistics Authority currently has the unilateral power to change RPI from 2030, but to do so before then will require the Government's consent. The consultation will address the question of whether the proposed change to RPI should be made before 2030, and if so at what point between 2025 and 2030.

The consultation will run for six weeks and it is intended that the Government and the UK Statistics Authority will respond to the consultation before the Parliamentary summer recess.

|

Action Trustees and employers should keep progress of the consultation under review. Trustees with CPI-linked liabilities which are currently matched by RPI-linked assets may wish to speak to their investment consultants. |

Issues affecting DB schemes

BENEFIT CHANGES

The Ombudsman has published its determination in relation to Mr R (PO-19569) who had complained that a detrimental modification had been made to the scheme without his consent.

In April 2017 the scheme was amended so that benefits would accrue on a career average revalued earnings basis, rather than a final-salary basis. The amendments also detailed how pre-April 2017 accrued benefits would be increased for active members and how pre-April 2017 benefits would be revalued for deferred benefits. Notably, the manner in which active members' pre-April 2017 benefits were increased was less generous than the rate of revaluation applied to the pre-April 2017 benefits of deferred members.

Mr R's complaint was that:

- The amendments froze his final salary benefits at that point in time and revalued them at a less generous rate than applied to the preserved benefits of deferred pensions;

- This amounted to a detrimental modification and therefore required his consent; and

- As his accrued final salary benefit had been frozen at the time of change, they were now deferred benefits and should be treated as such under the scheme's rules.

The Ombudsman dismissed the complaint. In his determination he explained that the active member's subsisting rights at the time of the 2017 amendments did not include revaluation of a pension in deferment.

|

Action For noting. |

PRIVATE MEMBERS' BILL

On 16 January 2020, the Pensions (Amendment) Bill 2019-20 was published and had its first reading in the House of Lords.

The Bill is a private members' Bill and its aims are to:

- Remove the cap on compensation payments from the Pension Protection Fund; and

- Require the approval of the Pensions Regulator and scheme trustees for the distribution of dividends.

It is currently uncertain whether the Bill has Government support and so it remains unclear whether the Bill has a realistic chance of becoming law.

The date of the second reading of the Bill is still to be announced.

|

Action Trustees and employers should monitor developments in this area. |

BRITVIC CASE

The High Court was required to determine whether Britvic's interpretation of certain provisions of its trust deed relating to increases to the pension paid to members was correct.

The relevant rule stated that the rate of increase was to be in line with RPI, subject to a capped increase each year of either 2.5% or 5%, "or any other rate decided by the principal employer".

Britvic argued that the "any other rate" language enabled it to substitute a rate that was higher or lower than would otherwise apply.

However, the Court held that when the rule was introduced the draftsmen had in mind only increases. According to the Court, the phrase introduced a two-stage mechanism to be used in any year, which meant that the employer had to apply the RPI default rate unless it exercised its discretion to introduce a higher, but not lower, rate.

|

Action Trustees and employers should take note of the decision, paying attention to the fact-specific nature of the decision. |

Issues affecting DC schemes

CHAIR'S STATEMENT

The Pensions Regulator has fined the trustees of the FCA's defined contribution pension plan for failing to comply with the requirements regarding the chair's statement.

The FCA's pension plan had applied to become an authorised master trust. Following receipt of the application, the Pensions Regulator noted that the chair's statement contained inadequate detail on the training received by the trustee board and the charges and costs levied by fund managers.

The Pensions Regulator issued a fine of £2,000 and stated that it "will take action against the Trustee of any scheme which fails to comply with the chair's statement requirements".

|

Action Trustees should ensure that their chair's statement contains the relevant details on how the scheme meets certain standards and regulations, its default fund, governance and costs and charges. |

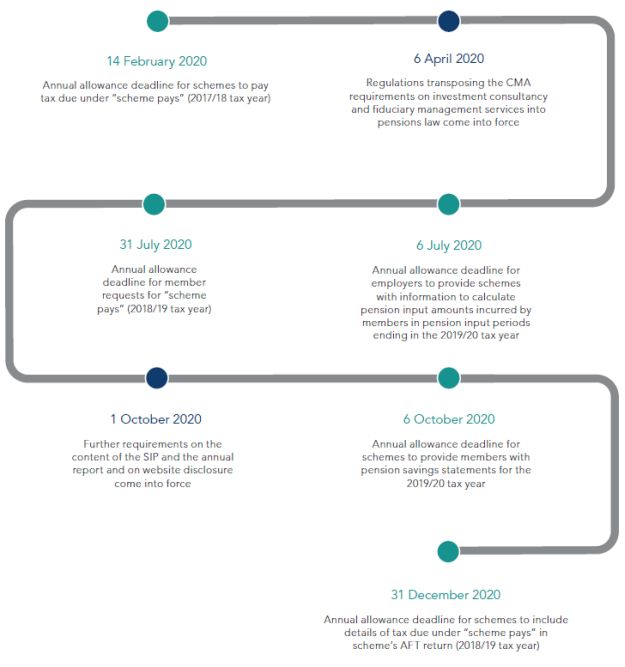

Dates to note over the next 12 months

January 2020

Visit us at mayerbrown.com

Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices"). The Mayer Brown Practices are: Mayer Brown LLP and Mayer Brown Europe – Brussels LLP, both limited liability partnerships established in Illinois USA; Mayer Brown International LLP, a limited liability partnership incorporated in England and Wales (authorized and regulated by the Solicitors Regulation Authority and registered in England and Wales number OC 303359); Mayer Brown, a SELAS established in France; Mayer Brown JSM, a Hong Kong partnership and its associated entities in Asia; and Tauil & Chequer Advogados, a Brazilian law partnership with which Mayer Brown is associated. "Mayer Brown" and the Mayer Brown logo are the trademarks of the Mayer Brown Practices in their respective jurisdictions.

© Copyright 2020. The Mayer Brown Practices. All rights reserved.

This Mayer Brown article provides information and comments on legal issues and developments of interest. The foregoing is not a comprehensive treatment of the subject matter covered and is not intended to provide legal advice. Readers should seek specific legal advice before taking any action with respect to the matters discussed herein.

[View Source]