Over the past several years, the use of a private trust company in combination with a purpose trust has been increasingly attractive to many clients - notably for clients from civil law countries, for those wishing to establish a family office structure, or for those who do not wish to use public trust companies.

What Is A Private Trust Company?

It is a company with trustee powers which is not required to be licensed under our trust legislation, the Trusts (Regulation of Trust Business) Act 2001 (the "Act"), provided that it fulfils the following criteria: (a) it is not carrying on the business as a trustee. In essence, this means that the private trust company cannot offer its services to the general public; and (b) by the terms of its memorandum of association, it is empowered to act as trustee of only a limited number of identifiable trusts.

The Private Trust Company must also certify to the Bermuda Monetary Authority ("BMA") in writing that it qualifies for the exemption from licensing by virtue of the above restrictions. It must also provide details to the BMA of the trusts of which it is to act as trustee.

A Private Trust Company cannot use any name which could indicate that it is carrying on a trust business unless it is licensed or has the benefit of an exemption order under the Act.

The minimum capital for the Private Trust Company is US$12,000 or its equivalent in some other currency.

Who Will Make Up The Board And What Presence Must The Company Have In Bermuda?

Bermuda law requires a company to have a minimum of two directors who are individuals. Corporate directors are not permitted. The board may, but need not, include one or more Bermuda-resident directors. The requirement for the board of directors in relation to a Private Trust Company provides an opportunity to create a "round table" forum in which family members can participate, perhaps together with trusted advisors. In this way, the client can be reasonably assured that there is a sufficient understanding of the family's background and dynamics and that, at the end of the day, the client's wishes with respect to the administration of the underlying trusts will be carried out. Board meetings may be held anywhere.

What Accounts And Records Must The Company Keep?

While it will be necessary for the Private Trust Company to observe all of the operational requirements applicable to exempted companies generally (e.g. with regard to the holding of the annual general meeting and related board meetings and so forth), it is unlikely that its activities will be such as to warrant the appointment of an auditor and the undertaking of an annual audit. However, it will be necessary for the company to maintain books of account. Ideally, these should be maintained in Bermuda. Certainly, where the principal books of account of the Private Trust Company are maintained elsewhere, it is necessary for there to be sufficient records available to the directors or representatives in Bermuda to enable them to ascertain with reasonable accuracy the financial condition of the Private Trust Company on a quarterly basis.

Who May Own The Company?

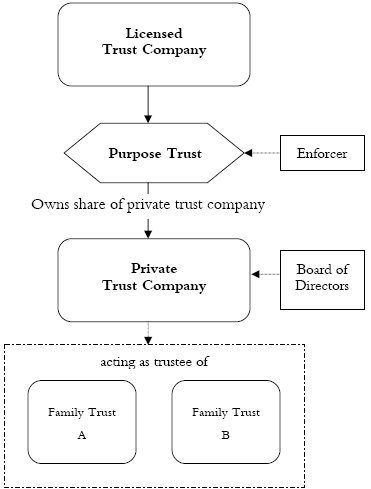

The company may be owned by an individual or a company, either in person, or through nominee arrangements. However, particularly for clients from civil law countries, it is generally thought to be undesirable that the ownership should have, or be perceived to have, any link with the client or any beneficiary of the trust of which the Private Trust Company is trustee. This is where the Purpose Trust comes into play. In order to fully understand how the purpose trust ownership is beneficial, it is important to understand what a Purpose Trust is. This is described below.

The Company In Commercial And Private Settings.

It is usual for a Private Trust Company to be incorporated to act as the trustee of one or more private family trusts or connected trusts. However, it can also be used to act as the trustee of commercial trusts. For example, financial institutions will sometimes use a wholly-owned Private Trust Company to act as trustee of 'in-house' collective investment trusts, such as unit trusts or mutual funds. There may be tax or accounting reasons for doing so, or a desire to isolate any risk associated with such a structure.

What Is The Difference Between A Purpose Trust And A Traditional Trust?

Unlike a traditional family trust, a Purpose Trust does not and cannot have beneficiaries. Rather, a Purpose Trust is created solely for the purpose stated in the trust document. Therefore, where the Purpose Trust will own a Private Trust Company, it will be established for the exclusive purpose of incorporating the Private Trust Company, acquiring and holding its shares and generally dealing with those shares.

How Long Can A Purpose Trust Exist?

A Purpose Trust can continue indefinitely or, as with a traditional family trust, its existence can be limited in duration in the trust deed. If a definite termination is wanted, the Purpose Trust's life is generally limited to 100 years from the date of the Purpose Trust.

Who Ensures The Purpose Trust Is Properly Administered?

For a trust of any kind to be valid, there must be someone who is responsible for enforcing the provisions of the trust document.

The trust document may, although it need not, appoint an enforcer (who, incidentally, can be one person, a committee of persons or a corporation). Other persons entitled to enforce the purpose trust include the settlor/grantor of the trust (unless the trust document prohibits this), a trustee of the trust and any other person whom the Court considers has a sufficient interest in the trust. Usually, the settlor/grantor wishes to be excluded. We would usually recommend the appointment of a corporate enforcer. Our affiliated company, Appleby Protectors (Bermuda) Limited, is available to serve as an enforcer where the circumstances are appropriate (as where the trustee of the purpose trust is not also associated with this firm). Fees are subject to negotiation and agreement by the Managing Director of Appleby Protectors (Bermuda) Limited.

For your added convenience, we can provide the following materials relative to the incorporation and organisation of an exempted company in Bermuda:

- Sample objects clause for memorandum of association, ·

- Standard bye-laws, ·

- A pamphlet describing the corporate administrative services customarily provided by our affiliated company, Appleby Corporate Services Ltd., ·

- A brochure on our affiliated licensed trust company, Appleby Trust (Bermuda) Ltd., ·

- Details regarding Appleby Protectors Bermuda Limited

This Brief does not address the creation and administration of the trust or trusts of which the private trust company will act as trustee and the incidental costs. These topics are covered in the Appleby Spurling Hunter Guide to Trusts in Bermuda.

This publication is intended only to provide a summary of the subject mattered covered. It does not purport to be comprehensive or to provide legal advice. No person should act in reliance on any statement contained in this publication without first obtaining specific professional advice. May 2005 © Appleby Spurling Hunter