- within Corporate/Commercial Law topic(s)

- in United Kingdom

- with readers working within the Banking & Credit and Property industries

- within Media, Telecoms, IT, Entertainment, Transport and Finance and Banking topic(s)

At a glance: PE usually involves larger, control-oriented investments in established businesses. VC typically backs earlier-stage companies through minority investments and staged funding rounds. Those commercial differences drive the legal terms, governance rights, fund regulation and exit mechanics.

The UAE has become a regional center for private capital. DIFC and ADGM offer common law frameworks, independent courts and specialist regulators, making them popular platforms for PE and VC funds, holding companies and investment structures. Structure matters: a mainland operating company, a DIFC fund and an ADGM VC Manager each raise distinct regulatory, tax and enforcement issues.

PE AND VC: THE BUSINESS DIFFERENCE

Both strategies invest in private companies, but they differ mainly by the target's maturity, risk profile and capital needs.

Target Companies and Risk

VC typically funds early-stage, high-growth businesses that may not yet be profitable.

PE usually targets mature businesses with established trading histories, with value created through operational improvement, acquisitions and margin growth.

As a result, VC carries higher company-stage risk and is often funded in rounds. PE is generally more capital-intensive and focused on control, governance and execution of a business plan.

Equity Stakes and Deal Structure

VC investors usually take minority stakes, often through successive funding rounds. UAE VC deals may be made directly into the operating company or through DIFC or ADGM holding companies, SPVs, SAFEs, convertible instruments or preferred shares, depending on tax, licensing, enforceability and investor requirements.

PE investors often seek control or significant governance rights. Deals are commonly structured as buyouts using a new acquisition vehicle, with founders or management rolling over part of their proceeds so that they remain aligned with the new owners.

KEY CONTRACTUAL DIFFERENCES

Because the commercial objectives are different, PE and VC deal documents use similar concepts in different ways. The key points are below

Leaver Provisions

Leaver terms protect value if a founder or manager leaves before exit. In PE, good leaver definitions are usually narrow, and pricing consequences are used to keep management committed. In VC, leaver terms focus on founder retention and are commonly linked to vesting, compulsory transfers, buybacks or conversion of shares, depending on the relevant company law regime.

Vesting

Vesting is central in VC. Founders typically earn equity over time, often over four years with an initial cliff, with possible acceleration on a sale or wrongful termination.

In PE, traditional founder vesting is less common. Management equity is more often managed through leaver provisions, ratchets, hurdles, escrow arrangements or forfeiture mechanics.

Ratchets

In PE, ratchets reward management if agreed performance targets are met. In VC, ratchets usually operate as anti-dilution protection, giving investors additional shares or economic adjustment if a down round occurs.

Drag-Along Rights

A drag right lets specified shareholders force a sale by the minority. PE investors usually want broad control over the drag. VC investors often require investor-majority consent, giving them both influence over an exit and protection against being forced into a sale they do not support.

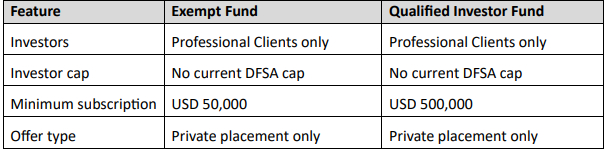

DIFC FUND FRAMEWORK

Fund Categories

DIFC PE and VC funds are typically structured as Exempt Funds or Qualified Investor Funds (QIFs), offered only by private placement to Professional Clients.

DFSA TREATMENT: PE VS VC

Private Equity Funds:

- DIFC Private Equity Funds are usually closed-ended, reflecting the illiquid nature of the portfolio.

- They are subject to the 25% single-venture concentration limit unless the fund is established to invest in a single venture.

- Related-party transactions are controlled and generally require prior investor approval by special resolution.

- If no eligible custodian is appointed, an investment committee is required.

Venture Capital Funds:

- A DIFC VC Fund must be an Exempt Fund or QIF that invests at least 90% of committed capital in qualifying unlisted ventures incorporated for no more than 10 years at first investment.

- Permitted investments include shares, convertible debt and instruments with equity participation rights issued by the portfolio company.

- VC Funds are not subject to the PE single-venture concentration limit.

- The regime is lighter: internal audit and finance officer appointments are not mandatory, self-custody is permitted, and an investment committee is optional.

- DIFC VC-only managers may benefit from lighter capital treatment, but the precise capital, liquidity and financial resources position should be checked against the manager's licence and current DFSA PIB requirements.

- Subsidised DFSA and DIFC Registrar fees may also be available

To view the full article clickhere

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]