Index Highlights Downward Trend of Default Rates, Which Continue to Fall Since Peaking in Q2 2020

NEW YORK, October 21, 2021 – Proskauer, a leading international law firm, today announced the results of the Proskauer Private Credit Default Index for the third quarter of 2021. The report revealed an overall default rate of 1.5% as of the end of Q3 2021. Default rates have trended lower since Q2 2020 when the default rate peaked at 8.1%. The quarterly index tracks the default rates of senior-secured and unitranche loans.

"As we continue to press forward with reopening our economy, default rates have declined to record low levels as borrowers return to financial health. We see an unprecedented amount of liquidity in the market, which is allowing borrowers to refinance or extend their loans on more favorable terms," said partner Stephen A. Boyko, co-chair of Proskauer's Private Credit Group. "Given these trends, our clients remain optimistic about the health of their portfolios."

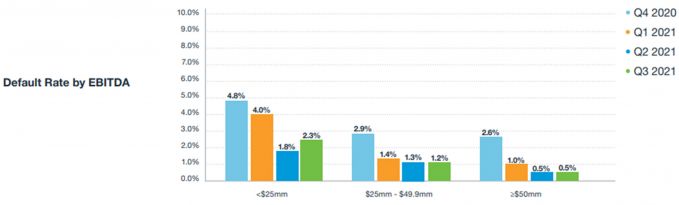

For Q3 2021, the Proskauer Private Credit Default Index reported that companies with more than $50 million of EBITDA at the time of origination had a 0.5% default rate, continuing a downward trend in the default rate from a peak of 5.3% in Q2 2020. Similarly, companies with $25-49.9 million of EBITDA had a 1.2% default rate continuing a downward trend in the default rate from a peak of 6.7% in Q2 2020.

The Index also includes proprietary analysis of defaulted loans by industry including: consumer/retail, food/beverage, healthcare, manufacturing and software/ technology. These are further refined by EBITDA band (0-$25mm, $25-49.9mm, and $50mm+), by default type (payment, bankruptcy, financial covenant, other material default, etc.) and by comparison to the publicly reported default rates for leveraged loans as reported by the rating agencies.

"The Proskauer Private Credit Default Index is just one of the many tools that we offer clients to help them make informed decisions about their businesses and the market. This Index includes a breakdown of more than 825 active private credit deals from over 75 lenders. While the influx of new deals may drive down overall default rates, we believe it is an accurate portrayal of the current health of the market and one that our clients have come to rely upon each quarter," added Boyko.

In addition to the Proskauer Private Credit Default Index, which is released quarterly, the Firm's Private Credit Group creates additional tools that offer unique insights to their clients, including an annual survey that features predictions from top lending institutions and a proprietary Private Credit Insights annual report.

Methodology

The Proskauer Private Credit Index includes companies across all major industry groups with EBITDA (earnings) from $0 to more than $1 billion. It is based on U.S. dollar denominated senior-secured and unitranche loans. Default rates are calculated by dividing the number of defaulted loans by the aggregate number of loans in the Index. While there are varying conventions of what is considered a default for purposes of calculating a default rate, the Index includes loans that have a payment, financial covenant or bankruptcy default, loans that are otherwise in default if the default is expected to continue for more than 30 days (excludes immaterial defaults) and loans that were amended in anticipation of a default.

A default is assumed to take place on the earliest of:

- The date a debt payment was missed

- The date a distressed restructuring occurs

- The date the borrower filed for, or was forced into, bankruptcy

- The date a financial covenant default occurs

- The date that a default occurs if that default is expected to continue for more than 30 days (excludes immaterial defaults)

- The date the loan is modified in anticipation of a default

For the purposes of the index, if a borrower re-emerges from bankruptcy, or otherwise restructures its defaulted debt and reestablishes regular, timely payment.