Law firms in Spain that

survived the crisis have reasons to be cheerful, but they now face

new challenges that could require a change in approach to

leadership

Law firms in Spain that

survived the crisis have reasons to be cheerful, but they now face

new challenges that could require a change in approach to

leadership

While law firms in Spain that successfully navigated the crisis

may be breathing a huge sigh of relief, they face a new set of

challenges. Research conducted by global legal consultancy Redstone

shows that firms currently have three key issues to address:

firstly, the need to ensure their `key' lawyers are happy and

motivated; secondly, the need to change their style of leadership

and possibly change their leaders; and finally, they have to make

difficult decisions about whether to focus on high-value work or

lower value commoditised work, provided it is done efficiently and

profitably.

Redstone's study analysed changes in the Spanish legal market

between 2008 and 2015 using data from Spanish newspaper

Expansión. The analysis focused on three key metrics –

income per partner, number of partners and turnover. This data was

used to plot different strategies that were adopted pre-crisis

– whether it was "growth at all cost" or

"quality work and profit first" – and then how the

strategies changed. For some firms size became a proxy for growth

strategy, while a higher income per partner reveals those firms

more concerned with the quality, and presumably profitability, of

work undertaken.

Key conclusions from the research include:

- Since 2008, it's clear the Spanish legal market has undergone unprecedented change in a relatively short period.

- Large and small firms adopted different strategies in response to the crisis, and the market will continue changing as firms adapt.

- As the crisis broke, transactions slowed , leading to an over-supply of services. Prices fell rapidly, though not for the highest value work. Firms that were well positioned at the top end, therefore, benefited from a softer landing as the economy slowed. For those providing more general services, it must have felt like a crash landing.

- Prices fell more quickly across Spain (and in Portugal) than in some other comparable jurisdictions.

Redstone chairman Peter Cornell, previously head of Clifford

Chance in Spain and the firm's former global managing partner,

says: "Our surveys of Spain's general counsel in this

period show the tables turning in their favour. Many said they had

a wider range of firms hungry for work. Under increasing cost

pressure and unable to perceive a quality difference between

providers, they were able to drive down prices." But Cornell

adds that general counsel were helped by the firms in this respect.

"As a former lawyer, I see the temptation to reduce prices to

win work," he says. Consequently, Redstone concludes, as many

of those lower-fee agreements were not agreed under a short-term,

emergency basis, it is unlikely the pricing issue – for

standard-type work – will be quickly overcome.

With revenues falling rapidly, some law firms reduced lawyer

numbers. Meanwhile, in andem, many firms also offered salary

partners a place in the equity, neatly moving what were fixed

salary costs into part of the profit share, with the additional

benefit of developing a higher sense of ownership among those

promoted. And, as part of the new selection for equity, it was no

surprise that some firms took the opportunity to filter out poorer

performers. As a result, the largest firms reduced headcount

drastically.

So who fared best, and worst, during the crisis? The Redstone study

highlights four different approaches adopted by law firms.

The Spanish elite

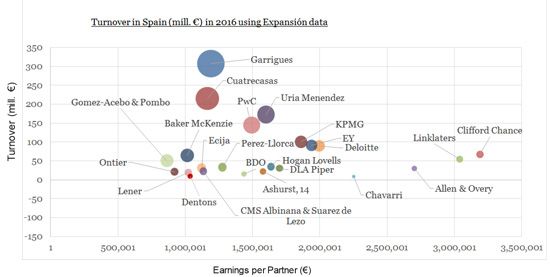

The biggest Spanish firms emerged stronger with Garrigues reporting

revenue of more than €349 million in 2016, an 18 per cent

increase on the 2008 total of €296 million.

Similarly, Cuatrecasas reported €269 million in revenues in

2016, up 12 per cent from €240 million in 2008. Meanwhile,

Uría Menéndez reported revenue of €222m in 2016,

an increase of 28 per cent on the 2008 figure of €174

million.All three firms can boast of being in a better position.

Credit must be given to these firms for their resilience, and their

ability to make tough decisions and adapt. The crisis demonstrated

that the largest firms aren't necessarily the slowest moving,

with the aforementioned 'Big Three' leading the way in

terms of structure and approach, which have, in turn, been adopted

by other firms.

New entrants

During the crisis, the former accountancy firms made significant

progress, with their legal arms going from strength to strength,

according to the study. PwC, EY, Deloitte and KPMG reported huge

increases in revenue. For example, turnover at KPMG stood at

€67 million in 2008 and by 2016 it had reached €103.8

million, despite challenging market conditions.

The impact of the rise of the 'Big Four' raises interesting

questions – these firms have taken an opportunity to grow at

low cost during the crisis years, making lateral hires from major

firms, without the usual high investment required in training and

development. The 'Big Four' now have the challenge of

keeping their top hires within a business environment that will

seem alien to many lawyers.

Global firms

The 'global elite' firms in Spain have fared well, likely

due to their focus on "higher value" work, with the

ability to project manage assignments, and costs, behind the scenes

and still returning a much higher "income per lawyer"

than that achieved by major Spanish firms. Clifford Chance and

Linklaters achieved "income per partner" of €2.8 and

€3.3 million in 2016 respectively, strikingly higher than that

recorded by Garrigues and Cuatrecasas, both of which achieved

between €1.1 and 1.2m. Among the locals, Uría

Menéndez has the highest income per partner, reporting

€1.6m last year.

Mid-market blues

The bottom-left of the bubble chart (see box) was the most crowded

area pre-crisis, with the "mid-market" firms sharing a

similar space. Some find themselves with difficulties, with neither

the brand for the highest value work nor the infrastructure

required to do standard work profitably. Noticeably, during this

period some firms dug themselves out of this predicament - in

particular, DLA Piper, which reported revenues of €30 million

in 2016, compared to €17 million in 2008. Meanwhile,

Pérez-Llorca is another firm experiencing strategic growth,

achieving €1.27 million "income per partner" in

2016.

What happens next?

Post crisis, many lawyers in Madrid are, unsurprisingly, enjoying a

brief "good to be alive feeling", but, according to

Redstone, they now have a new set of priorities, which are as

follows:

- Firms must look after "key" lawyers more than ever. High performers stay put during a downturn, even if unhappy, deciding to move on only once the climate improves.

- Firms that benefited from strong, decisive leadership during the crisis will now be looking for a change in approach and possibly new leaders. After the pain of change and redundancies, people want downtime to recover, Redstone says, so "peacemakers" are required.

- For the highest performing lawyers, who forgo higher incomes for the good of the firm during the bad years, remuneration systems will be "firmly on the agenda for review", says Redstone director Moray McLaren, who leads the consultancy's Iberia practice. "Firms must find a balance between keeping the junior partners within equity while appropriately rewarding top lawyers."

The good news for law firms is that, for higher value services, prices will be rising as transactions increase and lawyers get busy again. But prices for standard work will remain low. Firms need to do standard work profitably – for instance through the use of technology – or make difficult decisions about the type of work they should do going forward.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.