- within Law Department Performance, Strategy, Litigation and Mediation & Arbitration topic(s)

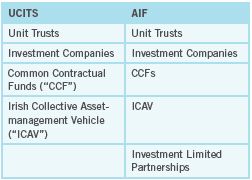

CATEGORIES OF FUNDS IN IRELAND

There are two broad categories of regulated investment funds in Ireland:

- UCITS; and

- AIFs.

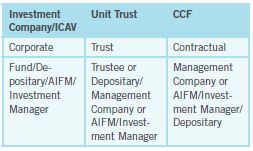

Either category of fund may be established as a single fund or as an umbrella fund comprising one or more sub-funds, each of which may have different investment objectives and policies. The forms which both categories of Irish fund can take are broadly as follows, with the main characteristics of each outlined later in this bulletin:

UCITS

The principal benefit of a UCITS classification is that the fund may be offered to the public throughout the EU subject to compliance with the cross-border notification procedures specified by the UCITS Directive (the "UCITS passport"). UCITS may be offered to both institutional and retail investors. Due to the potential for distribution to retail investors throughout the EU, UCITS are subject to an EU-wide regulatory regime in terms of eligible investments and diversification requirements. From a regulatory perspective, UCITS funds may invest in financial derivative instruments (exchange-traded or over-the-counter ("OTC") for investment purposes as well as for efficient portfolio management ("EPM") purposes subject to certain conditions including:

- the reference item or index to which the derivative relates must be an eligible investment and must come within the UCITS investment objectives;

- the counterparties are regulated institutions of a type approved by the Central Bank of Ireland ("Central Bank");

- the derivatives are subject to reliable and verifiable valuation on a daily basis and can be sold, liquidated or closed by an offsetting transaction at any time and for fair value; and

- compliance with the global exposure, counterparty exposure and cover requirements prescribed by the Central Bank's UCITS Notices and the derivatives risk management process adopted in respect of the UCITS.

AIFS

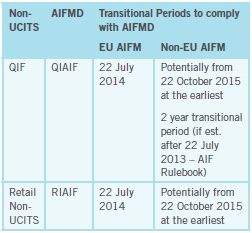

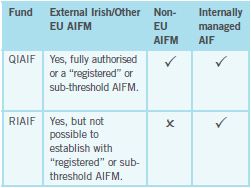

The other category of regulated investment funds in Ireland are AIFS, the managers of which are subject to the regulations implementing the EU's Alternative Investment Fund Managers Directive ("AIFMD"), which came into effect under Irish law in July 2013 and introduced the changes summarised in the table below. The two principal types of AIFs are QIAIFs and RIAIFs. The professional investor fund ("PIF") category was discontinued but the Central Bank allowed existing PIFs as at 22 July 2013 to continue in existence.

AIFMD regulates:

- EU AIFMs who manage AIFs in the EU; and

- Non EU-AIFMs which manage EU AIFs or which market EU or non-EU AIFs in the EU.

AIFMD provides for the marketing of AIFs to professional and retail investors across the EU and the opportunity to manage AIFs domiciled in Member States (other than the AIFM's home Member State) (the so called "AIFMD Passport"). The rules applicable to AIFs are set out in the Central Bank's AIF Rulebook. QIAIF's and RIAIF's can be managed in the following manner:

There are certain borrowing, investment and subscription requirements applicable to QIAIFs and RIAIFs. QIAIFs are invested in by qualifying investors belonging to one of the following categories:

- an investor who is a professional client within the meaning of Annex II of MiFID; or

- an investor who receives an appraisal from an EU credit institution, a MiFID firm or a UCITS management company that the investor has the expertise, experience and knowledge to understand the investment in the QIAIF; or

- an investor who self-certifies that they are an informed investor.

The minimum subscription amount for a QIAIF is €100,000 and it is not subject to investment, borrowing or leverage limits. Nevertheless, there is a statutory requirement to spread risk if the QIAIF is established as an investment company. In contrast, there is no minimum subscription requirement for a RIAIF. However, borrowings cannot exceed 25% of a RIAIF's net assets but, in contrast to a UCITS, borrowings can be effected for investment purposes as well as to meet redemption requests.

AIFMD PASSPORT

AIFMD Passport automatically became available to EU AIFMs managing EU AIFs when AIFMD was transposed into Irish law in July 2013. However, different rules apply in respect of non-EU AIFMs. A non-EU AIFM of an Irish QIAIF will not be able to avail of the AIFMD Passport until late-2015 at the earliest.

The European Securities and Market Authority ("ESMA") is to issue advice to the European Commission on the application of the AIFMD Passport to non-EU AIFMs by 28 July 2015. If that advice is positive, the European Commission must, by 22 October 2015, adopt a delegated act specifying the date when the non-EU AIFM passport will be "turned on". While this process is underway QIAIFs can continue to be managed by non-EU AIFMs under the existing transitional arrangements until at least 22 October 2015 at which time the Central Bank's will revisit the position and, if necessary, revise to align it with the European Commission's decision and any transitional arrangements provided.

RIAIFs cannot avail of an EU Passport to distribute their funds to retail investors in the EU. As a consequence, the marketing of an RIAIF in any EU Member State will depend on the relevant fund's offering rules in that Member State.

KEY CHARACTERISTICS OF IRISH FUNDS

DOCUMENTING DERIVATIVES WITH FUNDS: KEY ISSUES

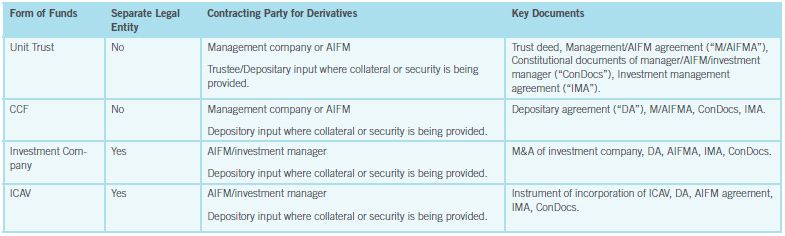

In documenting derivatives with Irish regulated funds the category and form of the particular fund has a material bearing on the detail and nature of the document and assessment of legal risk. The primary task lies in identifying the correct parties to contract on behalf of the fund and ensuring that those parties and their respective obligations are described accurately.

It is important to review the constitutive documents of Irish regulated funds in particular to determine:

- Nature of the Entity/Party: Consider the nature of the entity, who should be a party to the contract and applicable regulation.

- Representations and Warranties:

Consider what additional representation, warranties and additional termination events may be required.

- Confirming the counterparty's eligibility.

- Conclusive reliance on any instruction, request, certificate or representation from the investment advisor or manager of the fund.

- The fund has the power to enter into the transaction documents.

- Additional Termination Events

- Maintenance of the net asset value ("NAV")

- Supervision of dealings in the fund and/or the fund's NAV.

- Key personnel or delegation e.g. the AIFM, the investment manager, the depositary and the removal or reorganisation of the AIFM or investment manager.

- The constitutional documents or the disclosure documents of the fund will not be altered in a material way without the prior consent of the counterparty.

- Breach of UCITS requirements or AIF Rulebook

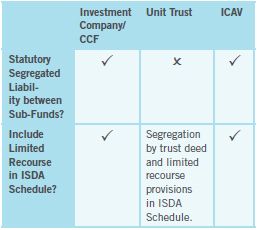

Liabilities of Parties/Segregated Liability: Establish the respective liabilities of the parties

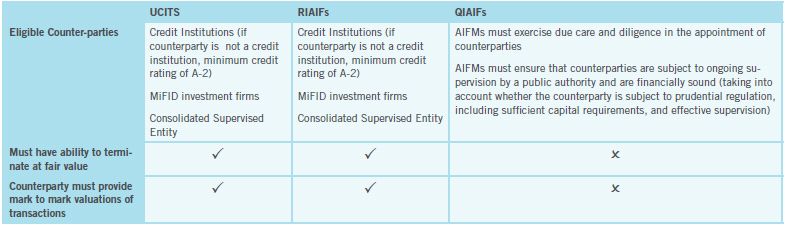

- Additional Provisions: Consider eligible counterparties, termination at fair value and mark to mark valuations of transactions.

EUROPEAN MARKET INFRASTRUCTURE REGULATION ("EMIR")

EMIR is the EU Regulation on OTC derivatives, central counterparties and trade repositories. Amongst other things, it imposes:

- mandatory central counterparty clearing of certain standarised OTC derivate contracts. Funds will need to negotiate documentation at the appropriate time to allow derivatives transactions entered into after the relevant clearing obligation date to be cleared through a central clearing counterparty;

- funds are required to have in place risk management procedures that require the timely, accurate, and appropriately segregated exchange of collateral in respect of uncleared derivatives contracts and;

- EMIR requires that each party to a derivatives contract report prescribed details of the transaction to a trade repository.

Parties may consider incorporating the terms of the ISDA 2013 EMIR Portfolio Reconciliation Dispute Resolution and Disclosure Protocol into their agreement.

MARKETS IN FINANCIAL INSTRUMENT REGULATION ("MIFIR")

The primary purpose of the MiFIR trading obligation is to determine which of those derivatives subject to the EMIR clearing obligations should also be required to trade on a regulated market, Multilateral Trading Facility ("MTF"), Organised Trading Facility ("OTF"), or equivalent third country venue when traded by relevant counterparties. MiFIR will apply to derivative contracts that are both cleared through and a central counterparty ("CCP") and deemed sufficiently liquid to trade on a trading venue and concluded with the following counterparties:

- Financial Counterparties as defined by EMIR which broadly are investment firms and credit institutions; and

- Non-Financial Counterparties that meet conditions stipulated by EMIR to be covered by the clearing obligation.

These trading venues must report details of transactions which are executed through their systems by a firm which is not itself subject to the MiFIR transaction reporting regime. MiFIR is expected to come into force in Ireland on 3rd January 2017.

NETTING

A favourable regime for netting exists in Ireland for netting in the context of Irish regulated funds. Of note, the Netting Act 1995 will apply, amongst others, to the National Treasury Management Agency ("NTMA"). The NTMA was established as a statutory corporation to perform the delegated functions of the Minister for Finance such as engaging in transactions of a normal banking nature. The entry by the NTMA into ISDA Agreements and similar banking arrangements are likely to be of a private law character for commercial purposes, and not within the sphere of Government or sovereign activity.

IRELAND STRATEGIC INVESTMENT FUND ("ISIF")

The NTMA also controls and manages the ISIF, which was established in December 2014 with a statutory mandate to hold or invest assets (whether in Ireland or abroad) in order to support economic activity and employment in Ireland. Provided that certain conditions are satisfied, such as the rights and obligations of the NTMA acting on behalf of ISIF being identical, the Netting Act may apply to an agreement where the ISIF is a counterparty.

PRIME BROKERS

QIAIFs will not be subject to the Central Bank non-UCITS guidance note on prime brokers 1. The new regime will instead rely on provisions of AIFMD which require care and due diligence in the selection and appointment of prime brokers and for the prime brokers to discharge reporting obligations. The prime broker must be subject to ongoing supervision by a public authority, be financially sound and have the necessary organisational structure and resources to perform the services which are to be provided by them to the AIFM or the AIF. The prime broker is defined in

1. Qualifying investors funds ("QIFs") that do not have an EU AIFM and continue to operate under the Central Bank's non-UCITS Notices continue to be subject to the Central Bank non-UCITS guidance note on prime brokers and other OTC counterparties.

AIFMD and generally includes a credit institution, a regulated investment firm or another entity subject to prudential regulation and on-going supervision.

REGULATION

The Central Bank of Ireland is the relevant regulator in Ireland for funds established as UCITS or AIFs in Ireland. It has issued UCITS Notices which apply to UCITS. Copies are available here. The Central Bank AIF Rulebook June 2015 can be found here.

This article contains a general summary of developments and is not a complete or definitive statement of the law. Specific legal advice should be obtained where appropriate.

[View Source]