- within Real Estate and Construction, Energy and Natural Resources and Consumer Protection topic(s)

- with readers working within the Law Firm industries

In a historic development, on 1 July 2021, 130 countries agreed to a broad framework for solutions to address tax challenges arising from digitalisation of the economy. Importantly, the solution envisaged does not restrict itself to the digital economy and could substantially reform the present international tax framework. This article is the first in a new series where we track the latest developments with respect to this historic global tax deal and its implications for businesses.

HISTORIC DEAL ACHIEVES NEAR-GLOBAL CONSENSUS ON INTERNATIONAL TAX REFORM

Introduction

Recently, majority member countries of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS-IF) agreed to the "Statement on a two-pillar solution to address tax challenges arising from the digitalisation of the economy" (Statement). Out of 139 BEPS-IF member countries, 132 countries (which comprise all G20 countries) have agreed to the Statement as of 14 July 2021. This means that India has also joined this important international tax reform.

At a broad level, the Statement reflects a global agreement on significant changes in the existing rules for allocating taxable income of Multinational Enterprise (MNE) groups between countries, and introduction of new rules to ensure that MNE groups pay a minimum level of tax regardless of where they are headquartered or the jurisdictions they operate in. The Statement is substantially based on the two-pillar solution proposed by the OECD Secretariat (OECD Blueprint) in October 2020, albeit with certain changes compared to the OECD Blueprint.

Traditionally, the taxation of business profits has been linked to a physical presence based nexus rule. While this was sufficient in the brick-and-mortar economy, the rapid digitalisation of the economy exposed gaps in such tax rules. Businesses no longer need physical presence to derive economic benefits from a jurisdiction. This has raised concerns for 'market jurisdictions' having the customer / user base, which, in the absence of a taxing right, are not getting their fair share of tax revenues on the income earned by offshore businesses from their territory. While this issue was first identified around two decades ago and being deliberated on since then, this historic deal marks a concrete step in this direction.

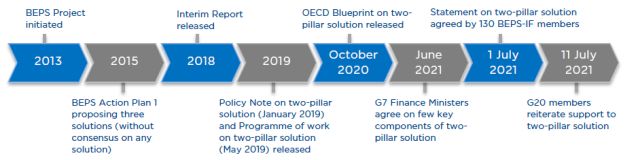

Timeline

Discussions at a global level to address tax challenges arising from the digitalisation of the economy began with the BEPS project in 2013. Until quite recently, reaching global consensus on the OECD's two-pillar approach to international tax reform seemed unlikely and some countries unilaterally started levying Digital Service Taxes to tax foreign businesses operating in the digital economy. Closer home, India implemented equalisation levy (EL) in 2016 and expanded its scope in 2020 to levy tax on non-residents earning income from India through digital means. However, talks gathered pace in recent months with the Biden administration revitalising the negotiations and lending its weight to the two-pillar solution.

Viewed in that context, the Statement is significant as it marks the first agreement among most BEPS-IF members in arriving at a consensus-based solution on taxation of the digital economy.

A timeline of events leading to the Statement is given below.

Main components of the two-pillar solution

The Statement reflects agreement on changes to tax rules that are clubbed into two 'pillars' – Pillar One and Pillar Two.

As regards Amount A, a final agreement is yet to be achieved on the exact percentage of residual profits that would be allocated within the agreed range of 20% - 30%. Allied with Amount A is the 'tax certainty' component, whereby MNEs will benefit from dispute prevention and resolution mechanisms of a mandatory and binding nature on all issues related to Amount A.

As regards Pillar Two, it should be noted that the GloBE Rules are essentially based on traditional controlled foreign company (CFC) principles that have already been enacted by various countries.

Businesses expected to be impacted by the two-pillar solution

Businesses covered by Pillar One

- Amount A will apply to MNE groups with global turnover above € 20 billion (approximately INR 176,000 crores) and profitability above 10% (ie, profit before tax / revenue greater than 10%) (In-scope MNE groups). It remains unclear whether this turnover threshold will be with reference to only a particular year (for instance turnover for the year 2020), or if it will be tested with reference to every year.

- The Statement provides that 7 years after the agreement comes into force, a review of Amount A's implementation will be conducted; if the review concludes that Amount A has been successfully implemented, the turnover threshold will be reduced to € 10 billion (approximately INR 88,000 crores), bringing more MNEs within the scope of these rules.

- Notably, two sectors are excluded from the scope of Amount A - extractives and regulated financial services.

- While the Statement provides that segmentation will be allowed in exceptional circumstances, at an overall level the Statement appears to suggest that Amount A will apply to all segments of an In-scope MNE group and not just those operating in the 'digital economy'.

Businesses covered by Pillar Two

- The GloBE Rules will apply to MNE groups that are required to undertake country-by-country reporting under applicable transfer pricing regulations, which essentially covers MNE groups having annual consolidated turnover above € 750 million (approximately INR 6,600 crores). The Statement adds that countries are free to apply the minimum tax rate principle to MNEs headquartered in their country even if they do not meet the aforesaid threshold.

- GloBE rules will not apply to government entities, international organisations, non-profit organisations, pension funds or investment funds that are Ultimate Parent Entities (UPE) of an MNE Group or any holding vehicles used by such entities, organisations or funds. Further, GloBE rules shall also provide for an exclusion for international shipping income using the definition of such income under the OECD Model Tax Convention.

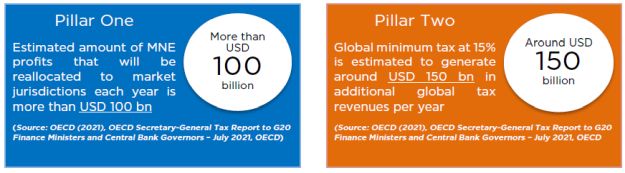

Estimated economic impact of the two-pillar solution

Way ahead and manner of implementation

While the Statement indicates agreement among 132 BEPS-IF members on key aspects of the two-pillar solution, an agreement is yet to be reached on certain important issues. This is recognised in the Statement itself, which states that a detailed implementation plan together with remaining issues will be finalised by October 2021.

Also, seven member countries of the BEPS-IF (Ireland, Estonia, Hungary, Nigeria, Kenya, Sri Lanka and Barbados) have not joined the Statement as of date and whether a consensus can be arrived at among all BEPS-IF members would need to be seen. Further, it will be important to keep an eye on whether the US Administration will get US Congress' approval for the two-pillar solution.

The Statement lays down the following timelines and manner of implementation for the two-pillar solution -

- Amount A will be implemented through a multilateral treaty; the Statement provides that it will be developed and opened for signature in 2022, with Amount A coming into effect in 2023. Work on Amount B is expected to be completed by end of 2022.

- The Statement provides that Pillar Two should be brought into law in 2022 and should be effective in 2023. The Statement provides for implementation of Pillar Two proposals in the following manner –

-

- GloBE Model rules would be implemented by BEPS-IF members through domestic legislation, including the possible development of a multilateral instrument for the purpose of coordinating GloBE Rules implemented by BEPS-IF members. The Statement provides that while BEPS-IF members are not mandatorily required to adopt GloBE Rules in their domestic legislation, BEPS-IF members will be required to accept the application of the GloBE rules applied by other BEPS-IF members.

- For STTR, a model provision together with a multilateral instrument would be developed to facilitate its adoption.

Pillar One – common questions

1. What is the policy rationale behind introducing Amount A?

Under the present international tax treaty framework, cross-border business profits are taxable in the source country provided a taxable presence by way of a Permanent Establishment (PE) exists in the source country. Therefore, income of businesses which operate without any physical presence in market jurisdictions such as technology companies remains largely outside the tax net of such jurisdictions. In response, certain countries have introduced unilateral measures in recent years which bypass the existing tax treaty framework. Such unilateral measures would unlikely be feasible in the long-run due to threats of retaliation by treaty partner countries and dangers of escalation to a trade war, necessitating a consensus-based solution.

Further, developing countries have argued that attribution of profits under the present international tax framework only considers the location of supply factors such as functions, assets and risks. It is contended that the location of demand factors, ie, the consumer, should also be given weightage while attributing profits to a jurisdiction.

To address the above issues, Amount A allocates the taxing rights over certain profits of large MNE groups to market jurisdictions even when there is no physical presence of an MNE group.

2. Will all market jurisdictions be allocated Amount A?

The Statement provides for 'nexus rules' to determine entitlement of a market jurisdiction to an Amount A allocation. The nexus rules essentially provide that –

- Allocation to a market jurisdiction will be permitted when the MNE group derives at least € 1 million (approximately INR 8.8 crores) in revenue from that jurisdiction; and

- For smaller jurisdictions (ie, with GDP lower than € 40 billion (approximately INR 350,000 crores)), the nexus will be set at € 250,000 (approximately INR 2.2 crores).

3. What happens if the residual profits of MNEs are already taxed in a market jurisdiction?

The Statement provides that where the residual profits of an MNE are already taxed in a market jurisdiction on account of marketing and distribution activities in that jurisdiction, the residual profits reallocated to that jurisdiction will be capped by a marketing and distribution profits safe harbour.

4. Will Digital Service Taxes and Amount A co-exist?

The Statement provides that all Digital Service Taxes and other relevant similar measures on all companies will be removed. Therefore, it is possible that India's EL will not be applicable upon implementation of Amount A.

5. How will Amount A work in practice once In-scope MNE groups are identified?

- In respect of In-scope MNE groups, Amount A will be allocated to market jurisdictions in proportion to the revenue derived by the In-scope MNE group from each jurisdiction. It is important to note that profits allocated to market jurisdictions through Amount A will be in addition to existing profits recorded by subsidiaries / PEs located in the market jurisdiction.

- The Statement provides that for determining tax base for allocation of Amount A, profit or loss of the MNE group will be determined by reference to financial accounting income, with a small number of adjustments. Further, losses of the MNE group will be carried forward.

- In order to relieve double taxation burden on MNE groups that may arise on reallocation of profits to market jurisdictions under Amount A, the entity (or entities) that will bear the tax liability will be drawn from those that earn 'residual' profit.

6. Will all constituent entities of an In-scope MNE group be required to undertake filings related to Amount A?

The Statement provides that tax compliance will be streamlined (including filing obligations) and In-scope MNE groups will be allowed to manage the process through a single entity. Further, the 'tax certainty' component of Pillar One is expected to reduce the potential for disputes through setting up of mandatory and binding dispute prevention mechanisms.

Pillar Two – common questions

1. How will the GloBE Rules work in practice?

- The GloBE Rules would comprise of two interlocking domestic rules:

-

- An Income Inclusion Rule (IIR), which would impose top-up tax on a parent entity in respect of low-taxed income of a constituent entity of the MNE group; and

- To the extent the low tax income of a constituent entity is not subject to tax under an IIR, an Undertaxed Payment Rule (UTPR) would apply and would deny deductions to other entities making payments to such low-taxed constituent entity or require an equivalent adjustment.

- The first step in determining application of GloBE rules would be evaluating whether the combined rate of tax (covered within the scope of GloBE Rules) paid by all constituent entities of an MNE group in a particular jurisdiction is lower than the agreed minimum tax rate. The Statement provides that in the aforesaid evaluation, the tax base would be determined by –

-

- reference to financial accounting income (with mechanisms to address timing differences and other agreed adjustments); and

- excluding an amount of income that is at least 5% (in the transition period of 5 years, at least 7.5%) of the carrying value of tangible assets and payroll.

- If it is determined that the taxes paid in a jurisdiction are lower than the agreed minimum tax rate, the IIR will allow eligible parent entity (or entities) to impose a 'top-up tax'. If the eligible parent entity (or entities) does not impose a top-up tax on the low-taxed income of a constituent entity, the UTPR will apply to exclude deductions on intra-group payments or require an equivalent adjustment.

2. What is the scope of STTR and how will it work?

- The Statement provides that STTR will allow source jurisdictions to impose limited source taxation on related party payments being interest, royalties and a defined set of other payments that are subject to tax below a minimum rate in the residence jurisdiction. An agreement on the exact scope of 'defined set of other payments' referred in the Statement is yet to be achieved. In this context, it is important to note that the G24 (Group of 24 developing countries which includes India) as well as the African Tax Administration Forum (ATAF) have favoured the inclusion of payments for services and capital gains within the STTR ambit.

- The taxing right of source jurisdictions will be limited to the difference between the agreed minimum rate and the actual tax rate on the payment. The Statement provides that the minimum rate for STTR will be 7.5% - 9%.

India's position on the two-pillar solution

A day after agreeing to the Statement, India's Ministry of Finance issued a Press Release stating that while India is in favour of a consensus solution, the solution should result in allocation of meaningful and sustainable revenue to market jurisdictions, particularly for developing and emerging economies. This was reiterated by India's Finance Minister in her remarks at the recent G20 Finance Ministers and Central Bank Governors meeting.

Notably, the Press Release mentions that some significant issues that remain open and need to be addressed include the share of profit allocation and scope of STTR. Therefore, one can expect that India would negotiate for a final agreement that allocates residual profits on the higher side within the 20% - 30% range agreed for Amount A, and provide for a wider scope of payments that would be subject to STTR.

Way Forward for Businesses

At the outset, MNE Groups should evaluate if they would meet the threshold requirements outlined for Amount A and the GloBE proposal. While the Amount A proposal on profit reallocation is unlikely to impact many MNE groups considering the high thresholds, Pillar Two proposals will cover various MNE groups if the proposed thresholds are adopted.

In the Indian context, Pillar Two proposals are likely to have a significant influence on outbound investment structuring. Therefore, MNE groups should keep these proposals in mind while setting up outbound investment structures over the coming months. Last but not the least, developments in this area must be closely watched considering their significant impact on the global international tax architecture.

The content of this document do not necessarily reflect the views/position of Khaitan & Co but remain solely those of the author(s). For any further queries or follow up please contact Khaitan & Co at legalalerts@khaitanco.com