The escalation of COVID-19 pandemic is expected to impact the Indian economy severely in the short to medium term. One of the key sectors likely to be affected is infrastructure, given its importance in supporting the overall growth and development of India's economy.

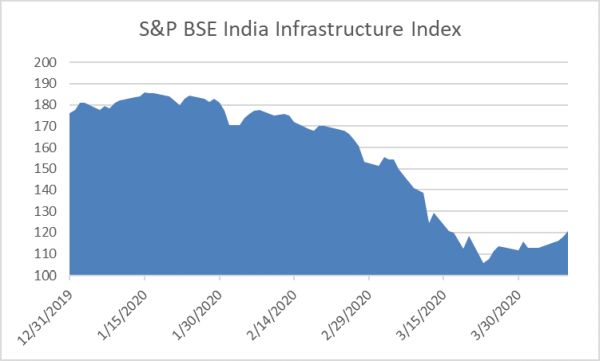

As we speculate on the future, the immediate impact on valuation is observable through the public market benchmark. The S&P BSE India Infrastructure Index has lost nearly 35% value between January end and March end.

Given the above volatility, in this article, we consider some of the key factors that investors should consider for their investing decisions and for fair value reporting purposes.

Macroeconomic Factors to Consider:

The macro challenges are arising from the fact that even though infrastructure assets are considered defensive assets, there will be substantial unsystematic risks originating due to COVID 19 as noted below:

Demand Risk

Early indicators show some sub-sectors linked to transport (air, sea and surface) have seen substantial demand cut.

Per the directions of the Ministry of Road Transport & Highways (MoRTH)/ National Highway Authority of India (NHAI), operations at all toll plaza of the Project SPVs of the Company have been closed. Also, no toll collection is allowed till April 15, 2020.

For power assets, since almost 50% of the demand is from industrial / commercial, sustained lockdown will have adverse impact on revenues, even post lockdown, ramp-up will take some time. Given there is no clarity whether the recovery would be U, V or L shaped, demand risk should be monitored closely.

Supply Side Risk

The impact of recent labor migrations due to COVID 19 will amplify the stress on the infrastructure sector. The availability of human capital is critical for both operational assets and under construction assets and there is no precedence to estimate the economic impact of human crisis. The volatility in pricing could also bring in challenges for this sector. However, at present the key commodities have shown a significant downtick due to lack of demand.

Liquidity Risk

Liquidity will be key to prevent any payment defaults or debt restructurings. Given the assets are significantly leveraged (operational and under-construction), the optimality of capital structures will be reassessed due to the sudden and significant impact on the revenue side.

Counter-party Credit Risk

As Indian infrastructure assets are attracting a lot of foreign funds, stress on the ratings and possible downgrades could test the ability of the domestic institutions to attract new investments in the short and medium term.

We have seen the initial reactions from the service providers, and they are noted below.

- As per exchange announcements by two of the leading service providers Ashoka Buildcon & IRB, the prevailing conditions may be treated as Force Majeure as per their Concession Agreement and therefore the respective Project SPVs are entitled for relief as per the terms of the Concession Agreement.

- They would also seek moratorium on loan repayment to banks and extension of the financial year closure timelines by at least three months to tide over the crisis.

The reactions highlight how the service providers have started calibrating their responses to this unprecedented challenge. The policy related reactions from the government are still awaited.

It should be noted that given the sheer complexity of the COVID 19 impact, scope and scale of the economic support and policy responses will be a major ask for even the most seasoned of policymakers.

However, the Reserve Bank of India provided some general relief to Indian businesses, which include debt moratorium for three months and working capital support through margin reductions and recalibration of working capital cycle.

The valuation challenges for the investors have started to unwind as well. The public market reactions are the first indicators for the same. The factors affecting valuation are arising from macroeconomic challenges, as highlighted before. Also, certain asset specific impacts could arise from COVID-19 disruption, which are highlighted below:

- Management of Liquidity: The priority is to ensure sources of liquidity to cope with any operational, CAPEX and debt related payment;

- Preservation of Yield: The investor group for this sector is mostly yield focused and the challenge arising from maintaining covenant ratios could affect the distributions in the short term.

- Optimization of the Capital Structure: An environment of lower cost of capital and cashflow challenges can lead to a new capital structure optimality for infrastructure assets.

The other valuation challenge would arise from the market observable inputs derived from recent and ongoing transactions, which didn't consider any COVID-19 impact. The valuation assessment would also be impacted by any government policy to support this sector.

For investors in Indian infrastructure assets, though the long-term story remains intact, the valuation assessment in the short term should be calibrated to the short-term challenges.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.