- in European Union

- within Cannabis & Hemp, International Law and Consumer Protection topic(s)

The rapidly growing middle class in Southeast Asia is bringing with it increased household wealth, increased consumption, and increased investment. As a result, the commercial banking sector has seen a boom in the more economically developed countries of the region—especially in Thailand. A select few foreign banks have also been very successful in Cambodia, Laos, Myanmar, and Vietnam for many years, but as other banks seek to replicate their Thai success in these new markets, the field looks likely to become much more crowded in coming years. Six major Thai banks are active in at least one other jurisdiction in mainland Southeast Asia, with some already operating across them all, and many larger international banks also beginning to take note.

Amid that background, this guide examines the legal frameworks for foreign banks seeking to operate in these jurisdictions, and addresses some current and upcoming developments that investors should note.

CAMBODIA

Jay Cohen, Nitikar Nith, Teo Pastor

Cambodia's legal framework is very favorable for foreign investors seeking to invest in the country's banking sector, as there are no restrictions on foreign ownership. Therefore, banks and other financial institutions can be 100% foreign owned.

Foreign investors and banks may structure their banking investments or expansion in Cambodia by way of a subsidiary, a branch, or a representative office. Subsidiaries and branches are both permitted to engage in banking activities in Cambodia, and, for a subsidiary, a foreign investor could incorporate a bank in Cambodia and own 100% of its shares or acquire the shares of an existing bank. Representative offices, however, are only allowed to conduct market research and other activities that do not generate income or profit.

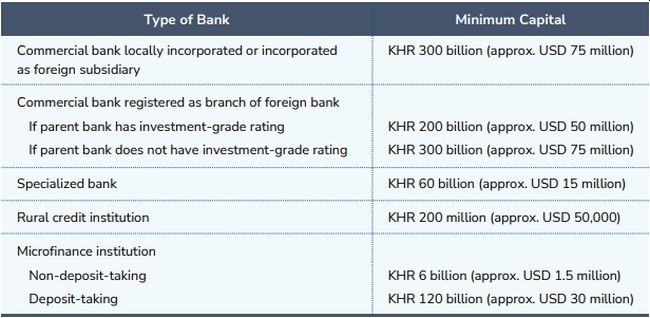

Cambodian law allows for the formation of commercial banks (which may be structured as either subsidiaries, locally incorporated banks, or branches), specialized banks, rural credit institutions, and microfinance institutions. Commercial banks are legal entities licensed to carry out banking operations, including (1) credit operations for valuable consideration, (2) the collection of non-earmarked deposits, (3) the provision of means of payment to customers and the processing of payments in Khmer riel (KHR) or US dollar, and (4) foreign exchange. Specialized banks, on the other hand, are banks that only operate in one of the above activities (typically lending, and without accepting deposits from the public). Rural credit institutions, also called specialized banks for rural credit, provide small loans in the agricultural sector.

Microfinance institutions (MFIs) provide financial services, such as loans and deposits, to poor and lowincome households and to microenterprises. In general, MFIs are not permitted to collect deposits unless they obtain a separate license from the National Bank of Cambodia (NBC).

All banks operating in Cambodia must comply with the minimum capital requirements below.

Establishing a bank and obtaining a banking license is a two-step application process at the NBC— first, an application for in-principle approval from the NBC, and then upon satisfying certain conditions, an application for final approval. Application review and approval takes approximately six months. If the NBC grants the banking license, this will be published in the NBC bulletin and the Official Gazette of the Kingdom of Cambodia.

LAOS

Dino Santaniello

The main relevant legislation is the Law on Commercial Banks No. 56/NA, as amended, dated December 7, 2018. This addresses a number of issues with regard to operation of commercial banks in Laos.

Minimum Registered Capital

The minimum registered capital for local or foreign commercial banks to set up a bank in Laos does not differ and is currently set at LAK 500 billion (approx. USD 30.46 million), while the minimum registered capital for foreign commercial banks seeking to establish only a branch is LAK 300 billion (approx. USD 18.27 million). In-kind value may account for up to 10% of the registered capital. Capital-in-kind can be immovable property or movable property in Laos used in the operation of the business of the commercial bank.

Internal Governance

A board of directors with at least five members must be created. Members serve three-year terms, and can be reelected for up to three consecutive terms. The board must include at least one external member—someone who is not an employee of the commercial bank and who has no family connections or contractual relationship with, or business benefits related to, a shareholder or executive of the commercial bank. This prohibition extends to other business interests unrelated to the bank. For example, an external member cannot be employed, even on a temporary or ad hoc basis, by a bank shareholder's other company.

Internal governance also relies on three required committees—the Governance Committee, the Risk Management Committee, and the Audit Committee—with the option of creating additional committees if desired. Eventually, a directors' council consisting of the director and the deputy director must also be set up. Appointment and dismissal of executives must receive consent from the Bank of Laos (BOL), which is responsible for supervising commercial banks.

Banking Activities

The law permits commercial banking activities, which generally encompass the typical services provided by a commercial bank (including the sale and purchase of foreign currency), as well as an allowance for the BOL to approve specific activities that are not listed in the law.

A commercial bank investing in another company that is not in securities business, insurance business, or financial business as further discussed below can invest only up to 10% of the registered capital of the commercial bank and cannot end up controlling more than 20% of the total shares having voting rights in the target legal entity.

Commercial banks can either set up their own entity or hold shares in other companies conducting securities business, insurance business, financial leasing operations, or other types of financial business upon the BOL's approval.

Foreign Financing of Commercial Banks

On December 10, 2019, the BOL issued Notice No. 684/BOL prohibiting financial institutions from obtaining loans from foreign legal entities or individuals that are not financial institutions or are not approved by the relevant authority of the country of origin for providing loans.

Microfinance Institutions

Deposit-taking and non-deposit-taking microfinance institutions are regulated separately under the Decree on Microfinance Institutions No. 184/G, dated June 20, 2022. To establish a microfinance institution, the decree requires minimum registered capital of LAK 30 billion (approx. USD 1,830,000) for deposit-taking microfinance institutions, and LAK 200 million (approx. USD 12,163) for nondeposit-taking microfinance institutions. For both types of institutions, foreign investors must hold at least 51% of the total shares.

To view the full article click here

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

[View Source]