1. Income Tax

1.1. General Aspects

1.1.1. Income Tax Rate

The general statutory corporate income tax rate for Salvadoran entities including Salvadoran branches of foreign companies is 25% on net income.

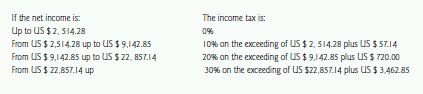

In the case of individuals, the law determines the tax brackets as follows:

The income tax resulting according to the table shown cannot in any case be superior

to 25% of the taxable income obtained by the contributor in each tax year.

1.1.2. Taxable Base

All revenues are subject to income tax unless otherwise excluded by law from the taxable base.

1.1.3. Deductions

As a general rule all costs and expenses are deductible provided that they are related, proportional and necessary to the income producing activity. Any costs or expenses related to Excluded and/or Exempted Items of Income are not deductible, the apportionment must be properly detailed and calculated in order to prevent from having a proportional rejection on overall deductible costs and expenses. Some costs and expenses are limited to quantitative ceilings, e.g. royalties and technical fees between a branch and foreign headquarters.

1.1.4. Depreciation

Tangible fixed assets' depreciation is deductible. Depreciation term varies depending on the nature of the asset. The accepted method of depreciation is straight-line method, any other method must be duly authorised by the proper authorities.

1.1.5. Transfer Pricing

Salvadoran legislation included recently with the 2010 tax reform, general rules for transfer pricing requiring that all transactions among related parties be recorded and effected at market price. The tax authority even has the power to set a price for a transaction for tax purposes, if it thinks the price is not within market terms for similar transactions.

1.1.6. Inflation Adjustments

El Salvador does not have inflation adjustment mechanisms.

1.1.7. Tax Losses Carry-forward / Carry-back

Each financial period is independent of any other; therefore Tax Losses Carry-forward and Carry-back are not applicable in El Salvador, except for capital gain losses against future capital gain earnings.

1.1.8. Financial Leasing Tax Treatment

Income from financial leasing is taxable with income tax, and it can be deducted as a cost for the lessee.

1.2. Payment and Filing.

Income tax must be paid through a Sworn Declaration that must be elaborated on a form legally established by the General Direction of Internal Taxes and which must be filed anytime during the term of four months following the end of the tax year.

1.3. Interest and Penalties on Unpaid Tax or Tax Paid Belatedly.

Not filing a tax return form before the proper authorities, the late filing, incomplete filing and other requirements established by law causes penalties and fines.

Ordinary Tax Year covers a period between January 1st and December 31st. All taxpayers must observe a filing deadline of four months after the closing of the corresponding Tax Year.

Penalties vary according to infraction and are established by the Tax Code ("Código Tributario.)

1.4. Dividends Tax / Branch Profits Tax

No dividend or profit tax is charged if the Corporation producing the profit and paying the dividends has paid the corresponding income tax.

1.5. Cross-Border Payments

There is no specific taxation on cross-border payments, except when it is regarding services provided locally or from abroad and the benefit is for the local company. The charges are 20% withholding on income paid to non domiciled entities, but this is not really a tax on cross-border payments exactly, it is a withholding applicable to income tax.

1.5.1. Withholding Taxes

Generally 20% as Income tax, and 13% as VAT when paid to a non domiciled entity or individual.

Christmas bonuses are to be withheld in the percentage for income tax, only when the amount of Christmas bonuses does not exceed the values set forth in the regulations.

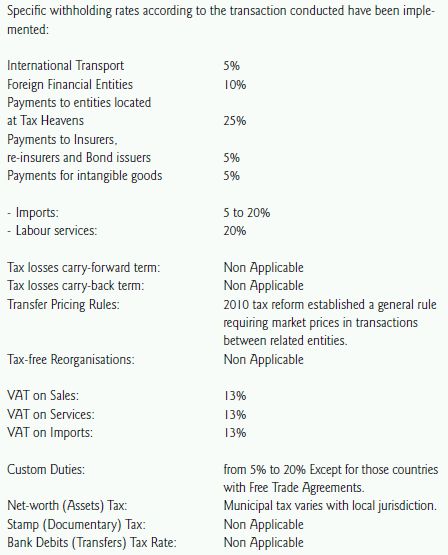

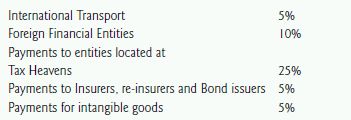

Specific withholding rates according to the transaction conducted have been implemented:

Foreign non-domiciled Banks which had been qualified for year 2009 by the Salvadoran Central Reserve Bank, and which cannot deduct in their homeland countries the amounts that they would pay for tax in El Salvador, and which are not considered by the Central Bank and the Ministry of Treasury as tax heavens can extend their full tax exemption for year 2010 onwards.

If the non-domiciled foreign Bank cannot deduct in its own homeland country taxes which would be paid in El Salvador, or are considered to reside in countries that qualify as tax heavens, a 10% withholding on interest earned applies.

1.5.1.1. Dividends

No withholding applicable.

1.5.1.2. Royalties

20 % withholding as income tax advancement payment, 25% if paid to a tax heaven country.

1.5.1.3. Technical, Administrative or other Advisory Services.

If rendered in El Salvador by a domiciled individual 10% withholding as income tax applies. If rendered by non-domiciled entities 20% income tax and 13% VAT, applies. Withholding applies for services rendered abroad and used in El Salvador.

1.5.1.4. Interest and Leasing Payments

Interest payments are subject to a 20 % withholding tax rate, unless located at a tax heaven country in which case withholding is 25%; for non-domiciled entities unless some exemptions apply, such as loans with a non-domiciled financial entity Registered before the Central Bank, which is withheld only 10%,. Leasing payments are subject to a 20% withholding tax rate, and 13% VAT.

1.5.1.5. Equity Reimbursements

Equity reimbursements are considered taxable income.

1.5.1.6. Tax Havens

Payments to entities or individuals located in countries considered as Tax havens are to be withheld 25% as income tax from the 2010 tax reforms.

1.5.2. Tax Treaties

Only general tax treaty in effect is with Spain, other tax treaties with Mexico and USA refer only to income earned by Airlines.

2. Value Added Tax (VAT)

2.1. General Aspects

2.1.1. Tax Rates

VAT's general rate is 13%, a zero tax rate is applicable for exports of goods and services. There is also some VAT exemptions for specific foreign entities and certain citizens under reciprocity treatment agreements.

2.1.2. Taxable Transactions

Any transfer of goods or services rendered are taxable, also real estate transactions only with regards to payment of rent.

2.1.3. Taxable Base

As a general rule, the taxable base is the price or value of the consideration paid for the goods or services, the tax rate is of 13%.

2.1.4. Creditable VAT

As a general rule the VAT taxpayer has a right to credit against payable VAT all VAT paid to her providers for tangible movable property bought or imported and for services hired, provided that they constitute a cost or expense of the taxpayer's income producing activity.

2.2. Selected VAT Incentives.

The VAT law does not include selective Incentives.

2.3. Payment and Filing

VAT has a 1-month taxable period. Therefore, the tax must be paid and a VAT return filed monthly. The VAT return must be filed and paid in full on the filing date, 10 working days after the closing of the monthly period.

3. Other Taxes

3.1. Property Taxes

Non applicable.

3.2. Industry

No industry tax

Commerce and Service Tax

No commerce and service tax other than 13% VAT at the national level. Municipalities have various commerce and service taxes. There is a scale according to the amount of assets.

3.3. Stamp Tax

Non applicable.

3.4. Registration Tax

The registration of acts and documents with the National Registrar Office is subject to registration taxes that vary according to a scheduler classification. The taxable base is the amount of the price or consideration shown in the document.

4. Customs Regime

General Aspects

4.1. Custom Duties.

Most Customs Duties go from 0% to 20%, with exemptions for countries with which El Salvador has Free trade agreements such as USA, All of Central America, México, Dominican Republic and Chile.

4.2. Taxable Base

Value of the merchandise.

4.3. Filing and Payment

A form to be filled when importing goods and paid before customs releases the goods. Imports to Free Zones are customs tax-free.

4.4. Selected Custom Duties Regimes Available

Free Zones and Service Parks do not pay custom duties, but all their production has to be exported to enjoy the tax exemption.

4.4.1 Ordinary Importation Regime

Regulated by Central American Customs Union and CAUCA treaty.

4.4.2 Temporary Importation Regime

Applies for some types of machinery such as construction machinery.

4.4.3 Active Improvement Regime

Non applicable.

4.4.4 Passive Improvement Regime

Non applicable.

4.4.5 Duty Drawback Regime

6% devolution applies on the value of exports of non-traditional goods out of the Central American Region.

4.4.6 Free Trade Zone Regime

Exemption of All taxes for Free Zone and Services Park. It includes Income Tax, VAT, customs, real state transference and municipal taxes.

5. Payroll Taxes/ Welfare Contributions

5.1. Social Security System

The Instituto Salvadoreño del Seguro Social manages and operates the Social Security System and the National Health System. These systems provide services and benefits related to illness treatment (Health Care), disability, maternity, and death insurance. Social Security taxes are applicable to employer and employees. The taxes are based on the monthly salaries with a 7.5 % rate for the employer and 3 % for the employee, with a maximum payment of USD 20.57.

5.2. Retirement Contributions

In Salvadoran law the contributions on this matter are divided as follows: 6.75% for the Employer (the ceiling is established on a salary of US $ 5274.52) and 6.25% for the employee (in which case there is no ceiling established or a temporal limit) this applies for the whole employment term. Contributions are deposited in a Labor Capitalization Account under employee's name to form the individual's Mandatory Complementary Retirement and savings fund.

5.3. Labour Risks Insurance

This mandatory insurance is covered by health services provided by the Instituto Salvadoreño del Seguro Social and covers all the labour force in the nation. The employer has to pay the insurance according to a schedule of payments updated by the Insurance National Institute.

5.4 Incidence on Wages Deductibility

For purposes of the Corporate Income Tax deductible expenses, the deduction of wages is conditioned to the accurate application of Income Tax on Salaries, Social Security and Pension Fund contributions

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.